Clearthink 1 Acquisition Corp.: Poised to Tap Financial Services Opportunities with Experienced Management

A blank check company leveraging a strong trust account and leadership expertise to secure its inaugural business combination in financial services.

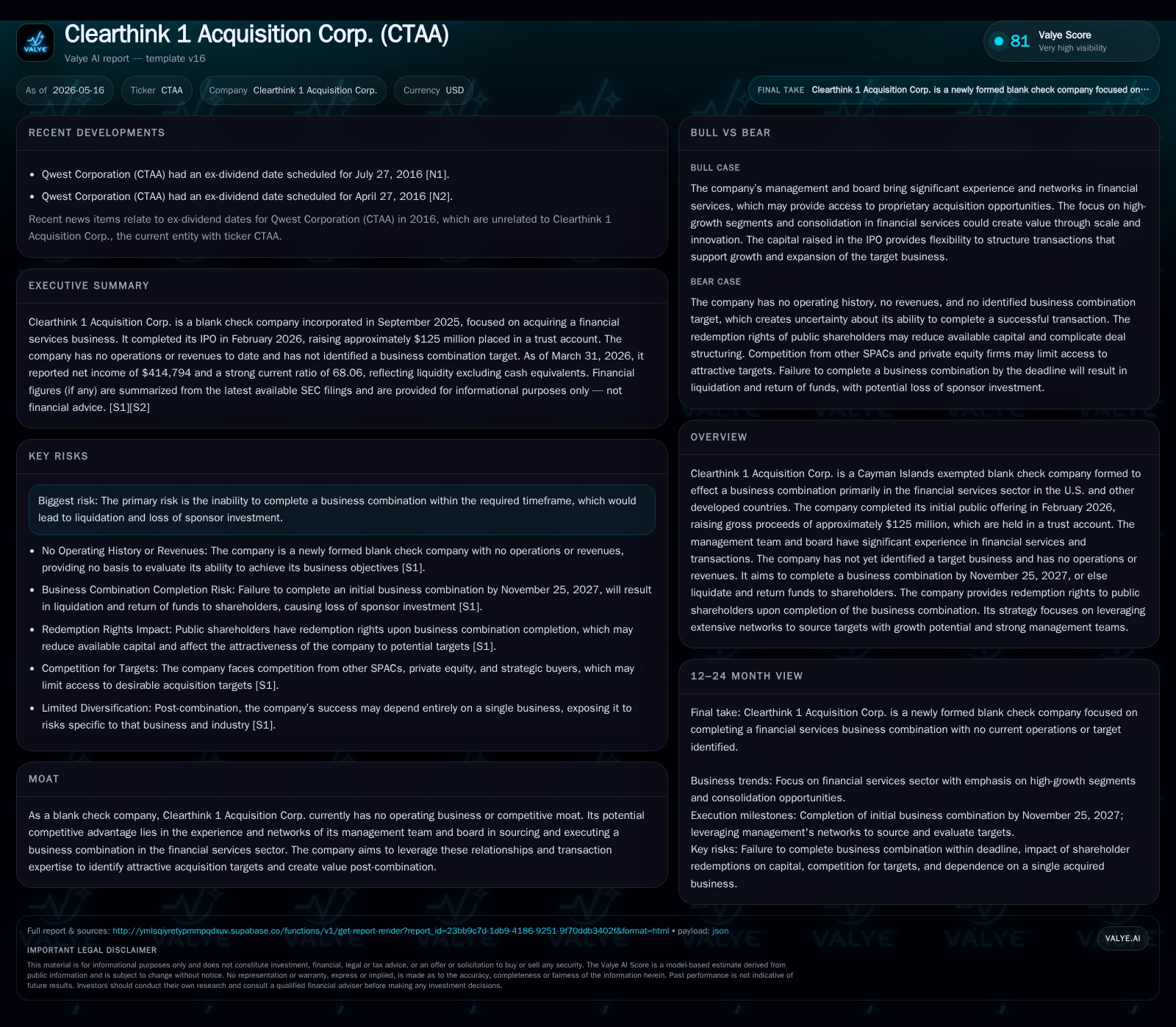

Clearthink 1 Acquisition Corp. remains on track with its strategic mission as reflected in the latest quarterly filing, maintaining a pristine trust account of approximately $125 million and advancing corporate governance by enabling separate trading of its Class A shares and rights. The SPAC is specifically focused on acquiring a financial services company in the U.S. or other developed markets, capitalizing on an experienced management team with robust networks for proprietary deal sourcing. The critical challenge ahead lies in consummating a suitable business combination by the November 2027 deadline while navigating shareholder redemption rights and potential sponsor interest shifts.

Quarterly Update Signals Progress Toward Business Combination

Clearthink 1 Acquisition Corp.'s latest quarterly filing (10-Q dated May 15, 2026) confirms that it remains strictly a blank check entity without operating revenues or active business operations but fully retains the cash proceeds from its IPO deposited into the trust account [S2][F1]. The trust account balance reflects approximately $125 million held via Equiniti Trust Company LLC, acting as trustee. Current liabilities are contained ($25,681), resulting in an extraordinary current ratio of roughly 68x — emblematic of exceptional liquidity positioned to fund an initial business combination when identified [F1].

Additionally, per the April 13, 2026 8-K event filing, holders of Clearthink’s public units (CTAAU) gained the option to separate their units into Class A ordinary shares (CTAA) and rights (CTAAR) that trade independently on Nasdaq starting April 16th [S3]. This structural change introduces greater flexibility in trading instruments representing claims on the eventual combined entity plus accretive shares. Such separation can enhance market dynamics for shareholders by providing granular exposure to share price moves versus merger-related dilution or redemption risks.

Business Model: Blank Check Structure and Target Sector Focus

As detailed in the March 31, 2026 annual report (10-K), Clearthink is established as a Cayman Islands exempted blank check company specifically created to effectuate a merger or similar business combination primarily targeting the financial services sector in developed economies including the United States [S1][S5]. It raised gross proceeds of ~$125 million through an initial public offering completed in February 2026 [S6].

The company generates no revenue until such time as it consummates an acquisition. Its economic model centers entirely on deploying capital raised within approximately a two-year window to transact with a privately-held target exhibiting growth characteristics aligned with financial services industry dynamics. These include businesses with recurring revenue streams, robust cash flow conversion profiles, high barriers to entry driven by regulation or technology moats, and strong existing management teams capable of scaling post-combination [S1][S5].

This focus leverages Clearthink’s management team's operating and investing background in financial services — enabling thematic deal sourcing linked to sector consolidation trends such as fintech innovation disrupting legacy banking models or asset managers consolidating portfolios [S13][S6].

Competitive Positioning Anchored in Management Experience and Networks

Unlike many SPACs with broadly diversified or generalist mandates, Clearthink positions itself through concentrated expertise within financial services complemented by deep and proprietary network relationships across venture capital firms, private equity funds, investment banks, family offices, industry executives and corporate boards globally [S13][S28].

Moreover, board members contribute complementary sector insights that enrich target screening processes — increasing likelihood of identifying underexploited or undervalued assets amenable to value creation through operational improvements post-merger [S13][S28]. The convergence of sponsors’ transaction know-how and network reach forms Clearthink’s core competitive advantage entering this crowded acquisition race.

Key Growth Drivers: Deal Sourcing and Transaction Timing

Clearthink's growth is inherently binary at this stage — predicated wholly on consummation of an initial business combination rather than organic expansion. Success metrics revolve around identifying a target company meeting stringent investment criteria by November 25, 2027 — approximately an eighteen-month window from the latest quarter date before mandatory liquidation triggers.

Target companies will be evaluated partly on potential for accelerating organic growth via innovative business models disrupting traditional services (e.g., embedded finance platforms), scale efficiencies from consolidating fragmented sub-sectors like wealth management boutiques or specialty insurers, recurring top-line stability fostering predictable cash flows, and scalability into public capital markets for long-term growth financing [S1][S6][S14].

Macro M&A environment conditions also influence prospects: favorable credit markets support debt financing opportunities augmenting offer flexibility; fintech sector momentum attracts interest in carve-outs; regulatory clarity impacts valuation premiums—all factors shaping acquisition timing and terms. Rapid execution constrained by fixed deadline induces urgency which can be both an impetus for deal closure or source of negotiation pressure from sellers aware of timeline leverage.

Risks and Constraints: Timebound Business Combination Deadline and Sponsor Dynamics

The overarching risk facing Clearthink is failure to complete an initial business combination prior to November 25, 2027 — after which it must liquidate trust assets returning funds pro rata to shareholders thereby resulting in loss of sponsor equity stakes and forfeiture of any upside participation [S29]. This temporal limitation imposes significant pressure on source diligence and negotiating pace.

Investor protections include redemption rights allowing public shareholders upon transaction announcement either at shareholder vote or via tender offer to exit at IPO price plus accrued interest regardless of vote outcome. While these rights safeguard investor returns should they disapprove of deal terms, excessive redemptions may erode transaction economics limiting attractiveness or ability to close with preferred targets [S27][S23].

Sponsor-related risks include potential dilution or control shifts if founder shares are transferred or forfeited prematurely before consummation. Such changes could reshape strategy focus or derail execution continuity without direct shareholder consent given sponsor control provisions embedded within governance documents [S18]. Also notable is the possibility that despite negative shareholder sentiment toward a proposed deal, sponsor entities hold sufficient class shares (approximately 25%) combined with founder shares voting power to approve transactions unilaterally — reflecting potential conflict between public investor interests versus management agenda [S23].

Lastly, single-asset risk post-combination means Clearthink’s future success hinges entirely on one acquired company's performance subjecting sponsors/investors to higher volatility than diversified entities.

Catalysts Ahead: Upcoming Milestones and Market Signals

Investors should closely track several key developments indicating progress along the acquisition pathway:

- Official announcement of identification or signing of a Letter of Intent (LOI) with proposed target.

- Details regarding intentions for seeking shareholder approval including proxy disclosures if required.

- Public shareholder redemption statistics ahead of vote providing insight into deal reception.

- Market reception toward newly separated Class A ordinary shares (CTAA) and rights (CTAAR) trading patterns reflecting liquidity perceptions.

- Regulatory guidance impacting financial service M&A activity which might influence valuation attractiveness.

- Publishing any forward-looking statements updating timelines or strategic adjustments post-quarterly filing [S2][S3].

These milestones will directly inform assessment of execution feasibility within tight timelines as well as underlying demand signals among retail investors participating currently only via unit ownership.

Financial Snapshot: Strong Liquidity Supports Strategic Flexibility

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Current assets | $1747943 | |

| 2026-03-31 | ||

| Current liabilities | $25681 | |

| 2026-03-31 | ||

| Current ratio | 68.06x | |

| 2026-03-31 |

Source: SEC companyfacts cache [F1].

| Metric | Value (USD) | Period Ended |

|---|---|---|

| Current Assets | 1,747,943 | |

| 2026-03-31 | ||

| Current Liabilities | 25,681 | |

| 2026-03-31 | ||

| Current Ratio | 68.06 | |

| 2026-03-31 |

As demonstrated above using companyfacts sourced from the most recent quarter ending March 31st, Clearthink exhibits outstanding liquidity characteristics largely driven by IPO proceeds securely held within its trust account collateralized for future acquisition use without impairment risk from liabilities exceeding nominal operational expenses [F1][S2]. No revenue streams exist yet; operating losses reflect standard organizational costs consistent with early-stage SPAC structures highlighting that current focus remains firmly on transaction readiness rather than commercial activity.

This fortress-like balance sheet provides strategic optionality allowing incumbent leadership adequate runway for deal scouting while eliminating near-term refinancing urgency often faced by entities reliant on ongoing cash flows.

This analysis is based strictly on information disclosed up to May 15th, 2026 filings without conjecture beyond cited sources. It does not constitute investment advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments