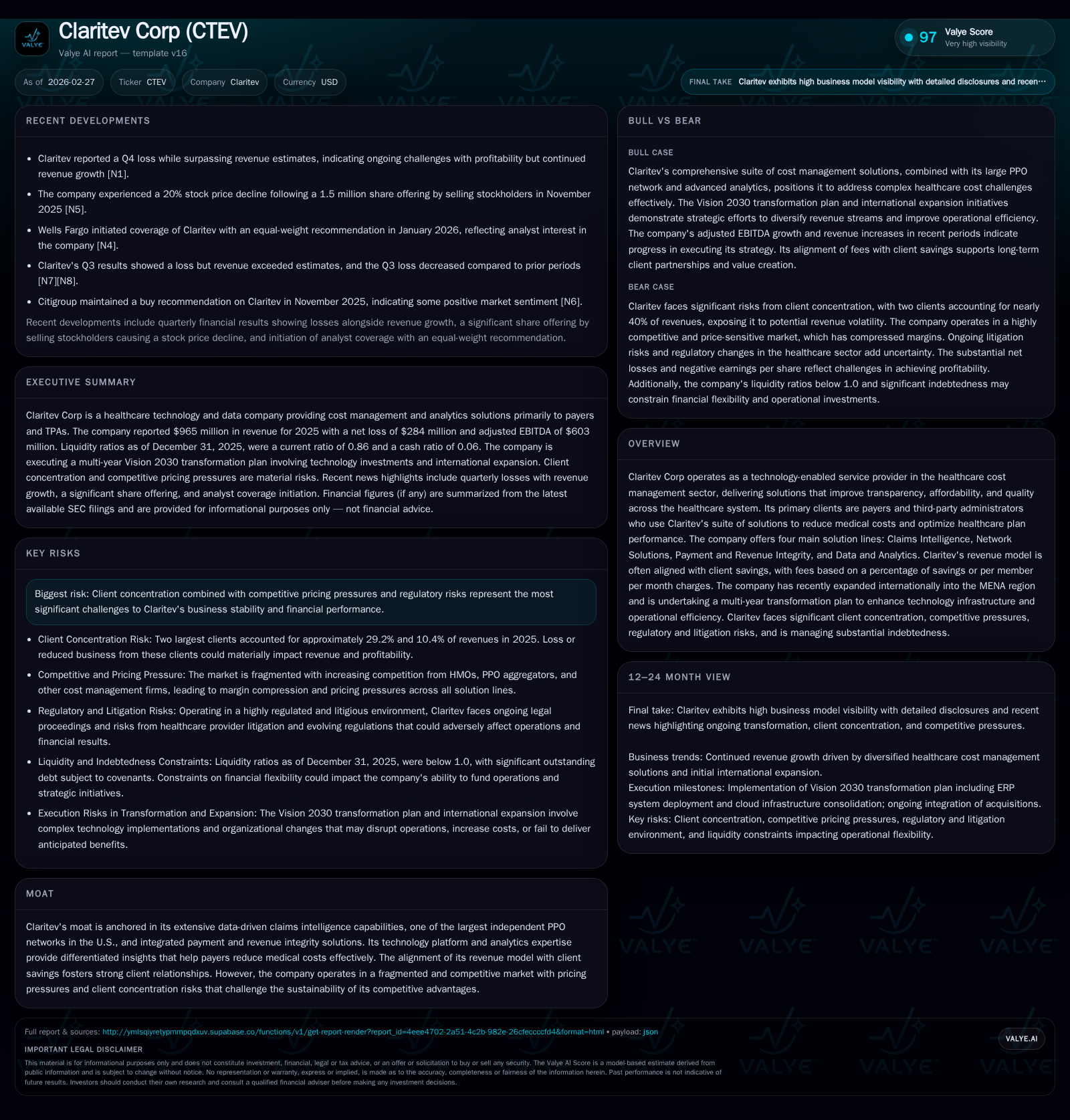

Claritev's Recovery and Challenges: Managing Client Concentration and Regulatory Risks with Modest Revenue Growth

Claritev Corp returned to operating profitability in 2025, but client concentration and regulatory headwinds continue to shape its financial and strategic outlook.

Claritev Corp, a healthcare cost management technology provider, reported a positive turnaround in operating income for fiscal year 2025 after steep losses in 2024. The company’s revenue grew modestly by 3.7%, driven by its claims intelligence, network solutions, and new international partnerships in the MENA region. However, net income remains deeply negative due to substantial interest expenses and prior goodwill impairments. Liquidity is supported by conservative borrowing under a revolving credit facility and cash from operations, but Claritev faces ongoing risks from high client concentration, competitive pricing pressures, complex litigation exposure, and evolving regulatory frameworks. Its multi-year technology transformation initiatives increase operating leverage and costs short term but may underpin future scalability.

Company Overview

Claritev Corp operates as a technology-enabled service provider within the healthcare cost management space. It offers solutions aimed at improving transparency, affordability, and quality across the healthcare ecosystem primarily serving payers and third-party administrators (TPAs). The company delivers four main solution categories: Claims Intelligence, Network Solutions, Payment and Revenue Integrity, and Data & Analytics. Claritev's revenue model largely ties fees to realized savings or usage-based metrics such as per employee/per member per month (PEPM) charges [S1][S26].

The company’s moat depends heavily on its data-driven capabilities for claims evaluation, one of the largest independent preferred provider organization (PPO) networks in the U.S., integrated payments integrity platforms, and an aligned fee model that links success with client cost reductions [S1]. However, Claritev operates in a fragmented market marked by competitive pricing pressures and faces material client concentration risks with its two largest customers accounting for roughly 40% of revenues in 2025 [S1][S29].

In pursuit of growth beyond the core U.S. market, Claritev launched its first international expansion in 2025 targeting the Middle East & North Africa (MENA) region through partnerships with established local healthcare organizations [S1].

Historical Performance & Financial Results

The following table summarizes Claritev's key annual financial metrics for fiscal years 2022 through 2025 [F1]:

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -284 | 117 | 29 | 130 | +82.7% |

| 2024 | -1646 | 108 | -1390 | 118 | -1694.9% |

| 2023 | -92 | 172 | 162 | 109 | +84.0% |

| 2022 | -573 | 372 | -363 | 90 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 0 | -12 | 163.5 |

| 2024 | 10 | -11 | -1958.8 |

| 2023 | 15 | 63 | -5.4 |

| 2022 | 0 | 283 | -32.0 |

Source: SEC companyfacts cache [F1].

Operating Income turned positive in the most recent fiscal year following a severe $1.39 billion loss driven primarily by goodwill impairment charges recorded in FY2024.

Revenue recovered modestly with a low single-digit increase reflecting stable demand combined with emerging international sales.

Net losses narrowed sharply but remain substantial due to interest expense burdening earnings.

Operational cash flow improved by approximately $9.7 million year-over-year while capital expenditure rose by near ten percent supporting ongoing system upgrades including SAP ERP implementation [S23][S6].

Share repurchases were paused during the latest period despite prior activity in earlier years when conditions permitted [F1][S16].

Growth Drivers & Strategic Initiatives

Claritev's growth hinges on several levers grounded in both product innovation and geographic expansion:

- Solution Expansion: Increasing penetration within existing accounts by cross-selling data analytics alongside core claims intelligence solutions could boost recurring revenues as these newer offerings mature [S1].

- International Markets: Building out presence in MENA presents an opportunity to replicate successful U.S.-based cost-management models tailored to regional payer systems [S1].

- Technology Transformation: The ongoing multi-year effort to upgrade core IT infrastructure aims to enhance operational efficiency and scalability which may translate into margin improvement [S23].

- Client Retention & Pricing: Maintaining business levels with large clients who account for a disproportionate share of revenues is vital; however this exposes Claritev to renegotiations under pricing duress or utilization drops influenced by employment trends affecting health plan enrollment [S1][S7].

- Regulatory Adaptation: Navigating an evolving healthcare regulatory landscape including compliance with anti-kickback statutes, surprise billing laws, data privacy rules like HIPAA, as well as increasing scrutiny on cost management practices is both a challenge and potential barrier to new business development [S7][S15][S21].

Key impediments or capping factors include legal risks arising from lawsuits brought by providers resisting cost controls, potential loss or contraction of large payer contracts if consolidation trends reduce supplier diversity or bargaining leverage shifts unfavorably against Claritev [S7][S13]. Additionally, growing competition from boutique integrators or internal solutions developed by payers could limit market share gains.

Forecasts & Benchmarks to Watch (Analysis)

While no explicit company guidance was disclosed recently beyond annual results announcements [N1][S3], external observers should monitor:

- Continued revenue growth momentum particularly from international ventures.

- Margins progression amid investment costs associated with transformation.

- Client renewal rates and any changes in contract terms reflective of negotiating power balance.

- Legal outcomes or regulatory developments impacting operational model tolerances.

- Liquidity status including revolver borrowings relative to capex needs.

Capital Structure & Returns Analysis

Claritev carries substantial indebtedness stemming from multiple tranches of first lien term loans totaling over $1.45 billion combined outstanding at end-2025 bearing blended interest rates around ~8.9% after interest rate swaps reduce floating risk partially [S11][S16][F1]. Interest expense increased further in FY2025 compared to FY2024 ($392 million vs $326 million) exacerbating net losses despite improved operating results [F1]

Liquidity remains adequate supported by cash balance ($28 million including restricted cash), positive operating cash flow ($117 million), and an undrawn revolving credit facility with ~$324 million remaining capacity [F1][S16]. Nevertheless stringent debt covenants restrict flexibility including limits on dividends or repurchases while repayments pose refinancing risks should capital markets tighten unexpectedly [S24][S6].

No share repurchases took place in FY2025 though the board authorized a five-year buyback program up to $75 million starting January 2026 capped annually at $20 million that has yet to be deployed indicating cautious capital allocation priorities amid balance sheet repair efforts [S16][F1].

Return metrics are currently depressed given heavy non-cash goodwill impairments past years and high leverage — approximate ROE calculated via latest net income over equity sits abnormally high negative (negative equity base), underscoring unresolved balance-sheet weakness while operating profits have stabilized recently which may bode better prospectively [F1].

Industry Context & Competitive Positioning (Analysis)

The healthcare cost management sector navigates complex payer-provider dynamics exacerbated by regulatory flux around reimbursement models such as surprise billing reforms under the No Surprises Act, continued consolidation among insurers leading to concentrated purchasing power, and technology innovation pressures incorporating AI-driven analytics tools.

Claritev maintains one of the largest independent PPO networks—a strategic moat conferring bargaining leverage—but it still contends with competitors offering vertically integrated platforms that bundle claims adjudication or care management services which they do not provide directly themselves.

Its alignment of fees based on savings delivery fosters client trust yet also imposes revenue variability tied closely to claims volume fluctuations which can be impacted by employer hiring trends or plan design changes reducing covered populations.

Legal challenges especially those brought by provider groups contesting utilization review or network adequacy add costly uncertainty requiring investment in compliance infrastructure.

Conclusion

Claritev has successfully reversed negative operational momentum experienced through fiscal year 2024 demonstrating resilience through incremental revenue growth supported by expanding solution scope and international partnerships. However, this improvement masks significant underlying challenges—most notably elevated client concentration risk exposing revenues to fierce pricing negotiations amidst insurer consolidation trends; compounded substantial debt load carrying substantial interest burdens; ongoing exposure to complex litigation environments resisting cost containment strategies; plus evolving regulatory demands requiring continuous adaptation.

Capital allocation remains prudently conservative following prior balance sheet distress; cash flows are positive but future free cash generation is currently constrained due to elevated capex needs supporting critical ERP upgrades crucial for future operational scalability.

To realize sustainable growth trajectories while preserving profitability gains, Claritev will need careful navigation of contractual relationships with its largest clients alongside vigilant legal risk management complemented by smart deployment of its technology modernization efforts.

This analysis does not constitute investment advice or solicit investment actions pertaining to Claritev Corporation securities.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments