Cash Flow Struggles and Strategic Constraints Cloud Camping World’s 2025 Outlook

Camping World contends with softer consumer demand, rising costs, and restrictive debt covenants following a decade of growth tied to RV market surges.

Camping World Holdings, Inc. saw its top-line rebound modestly in 2025 after the initial COVID-driven boom dissipated, challenged by shifting product mixes towards lower-priced travel trailers and greater promotional activity. Operating income rose 21.3% year-over-year, yet net losses deepened due to inventory management pressures and elevated SG&A expenses amid a competitive and seasonally volatile environment. The company’s liquidity remains adequate with a current ratio near 1.2, but restrictive senior secured credit facility covenants limit capital deployment options including dividends and acquisitions. Investors should watch for shifts in same-store sales, supplier agreements, and cash flow trends to gauge operational resilience.

Revenue Growth and Evolving Product Mix: Tracking a Decade of Change

Camping World’s revenue trajectory over recent years reflects a period of rapid expansion followed by more recent headwinds tied closely to evolving consumer preferences within the RV space. From approximately $670 million in 2016, the company expanded its top line to nearly $982 million by the end of 2018 [F1]. Growth accelerated further through the pandemic era when consumers sought socially distant travel options, propelling demand for new RV units.

However, as of 2025, revenue increased moderately by about 10.5% over the prior year [F1]. A key dynamic shaping this trend has been the product mix shift toward travel trailers—less costly units compared to motorhomes or fifth wheels—that grew from roughly 62% of new unit sales in 2015 to approximately 79% by 2025 [S1]. Despite inflationary pressures pushing nominal prices upward, this mix shift contributed to an overall decrease of around 8% in average selling price per new vehicle over this period—down to roughly $37,083 per unit [S1], [F1].

Dealer agreements with manufacturers include obligations such as stocking requirements and minimum advertised price floors that influence strategic inventory decisions [S19]. The increased reliance on travel trailers necessitated deeper attention to pricing tactics as volume alone could not sustain previous per-unit revenue gains.

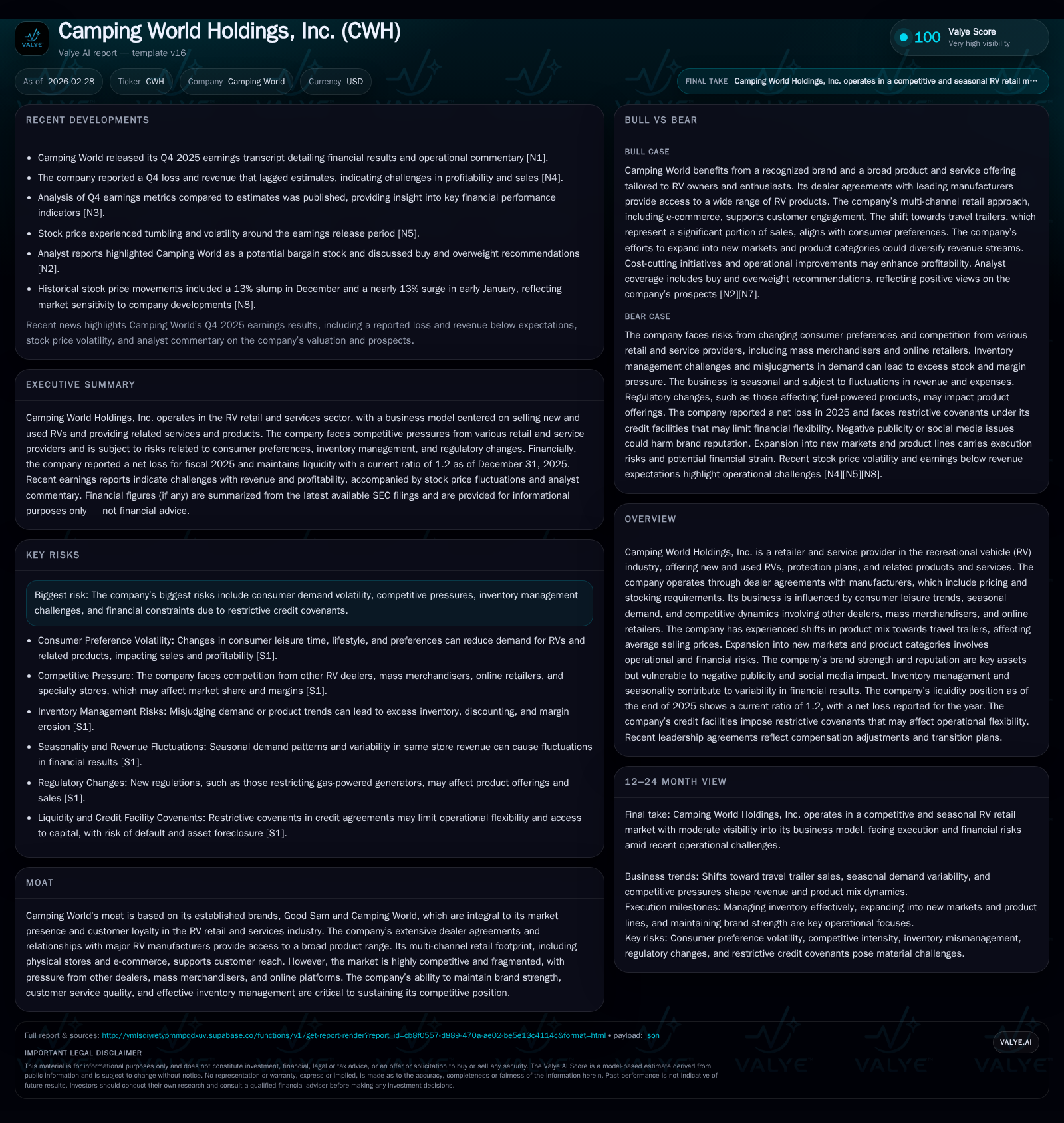

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Net YoY |

|---|---|---|---|---|

| 2025 | -90 | -132 | 180 | -132.4% |

| 2024 | -39 | 245 | 149 | -224.5% |

| 2023 | 31 | 311 | 267 | -77.3% |

| 2022 | 137 | 190 | 569 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | ROE% |

|---|---|---|---|

| 2025 | 31 | -39.3 | |

| 2024 | 25 | 0 | -11.8 |

| 2023 | 67 | 0 | 24.9 |

| 2022 | 105 | 80 | 92.6 |

Source: SEC companyfacts cache [F1].

Table notes: Revenues before FY2019 unavailable; YoY calculations only where appropriate data exist.

Consumer Trends in Recreation Vehicles: From Boom to Normalization

The COVID-19 pandemic catalyzed an unprecedented wave of consumer engagement with RV ownership as travelers sought socially distanced ways to explore [S1], [N1]. This phenomenon markedly boosted foot traffic across Camping World’s multi-channel retail footprint comprising physical stores and e-commerce platforms.

As these exceptional conditions abate, the company faces erosion in active customer levels—a key metric driven partly by reduced discretionary spending propensity and intensified leisure competition [S1], [N3]. Promotional activities have proliferated as Camping World attempts to mitigate impact from diminished foot traffic amid rising inventory carrying costs.

Discretionary spending volatility pervades outdoor lifestyle sectors; consumer willingness to invest in big-ticket recreational assets fluctuates with employment confidence, fuel prices, and competing vacation alternatives like air travel or experiential tourism [S1]. Maintaining robust customer acquisition and retention is pivotal for stemming margin erosion.

Profitability Pressures: Operating Income vs. Net Loss Dynamics in 2025

Despite achieving an operating income increase of over $30 million or nearly +21% year-over-year in fiscal 2025 [F1], Camping World’s net income reflected sharply widening losses at -$89.8 million compared to -$38.6 million the prior year [F1]. This contrast highlights financial pressures below operating line primarily attributed to elevated interest expense linked with substantial debt loads compounded by inventory markdowns amidst softened unit pricing.

Rising SG&A expenses further pressured profitability as staffing costs surged seasonally while marketing spend intensified to counter declining same-store sales productivity particularly during peak quarters [S1], [N3]. Additionally, product mix dilution owing to higher travel trailer proportions limited gross margin expansion despite cost containment efforts.

Liquidity, Debt Covenants, and Capital Allocation Constraints

Camping World maintains cautious liquidity management with current assets near $2.62 billion outpacing current liabilities around $2.18 billion for a current ratio of approximately ~1.2x [F1]. While this supports short-term solvency comfort, underlying debt arrangements impose substantial operational restrictions.

Senior secured credit facilities—including a revolving credit line plus approximately $1.4 billion term loan—and extensive floor plan financing contain covenants that restrict incurrence of additional debt, asset sales, dividend payments beyond modest levels, share repurchases (suspended since FY2023), acquisitions, and certain investment activities [S4], [S5].

Capital allocation thus prioritizes servicing existing obligations over growth investments or enhanced returns which may constrain strategic flexibility during periods demanding rapid adaptation or opportunistic M&A pursuits.

Seasonality, Inventory Cycles, and Their Impact on Financial Outcomes

Sales are concentrated with roughly sixty percent occurring during spring/summer quarters aligned with vacation patterns for RV users [S6], [S7]. This seasonality introduces cyclicality affecting revenue recognition and margin volatility through fluctuating labor utilization rates and variable promotional activity.

Inventory management complexity is heightened; floor plan financing supports stocking large volumes ahead of peak seasons but misalignment risks excess aging stock requiring discounting that exacerbates margin pressure [S28]. Demand forecasting inaccuracies around evolving consumer tastes add obsolescence risk especially when coupled with disruptions such as atypical weather patterns.

Effective coordination across procurement planning, retail execution, and pricing strategies remains an ongoing operational challenge underscoring recent cash flow stress.

Future Business Prospects Amid Competitive Pressures and Market Risks

Camping World faces intensifying competition spanning traditional dealership rivals to mass merchandisers like Walmart or Target expanding outdoor recreational categories alongside growing digital-first e-commerce platforms [S27]. Manufacturer concentration—with Thor Industries and Forest River representing over ninety percent combined supplier share—raises supply chain dependency risk [S29].

Regulatory uncertainty looms over emissions standards particularly California Air Resources Board regulations impacting diesel-powered motorhome availability post-2024 model year; federal rollbacks add ambiguity complicating fleet alignment with customer expectations [S26].

Brand equity anchored via Good Sam memberships requires active stewardship amid evolving member demographics reflecting broader leisure interests realignment [S16].

Expansion into new products or geographies carries execution risks including site selection difficulties plus skilled personnel recruitment challenges prolonging ramp-up timelines potentially depressing near-term returns [S11], [S14].

What Analysts Watch Next: Milestones, Risks, and Operational Indicators

Key metrics include monitoring quarterly same-store sales during critical second-third quarter windows given their disproportionate contribution to yearly revenues alongside tracking operating cash flow trajectories for signs of recovery or continued strain indicating liquidity pressures [N1], [N2].

Supplier renewal negotiations—particularly with major OEMs like Thor Industries—will materially influence product assortment breadth and pricing power directly affecting margins amid shifting industry fundamentals [N7].

Investors will assess effectiveness of cost reduction programs aimed at organizational streamlining balanced against potential talent attrition or morale impacts that could erode service quality reported during prior initiatives [S17]. Meanwhile digital channel leverage may partially offset physical footprint limitations warranting incremental resource reallocation considerations.

This analysis is based solely on disclosed financial data and filings up to early 2026 without speculative forward-looking valuation or investment recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments