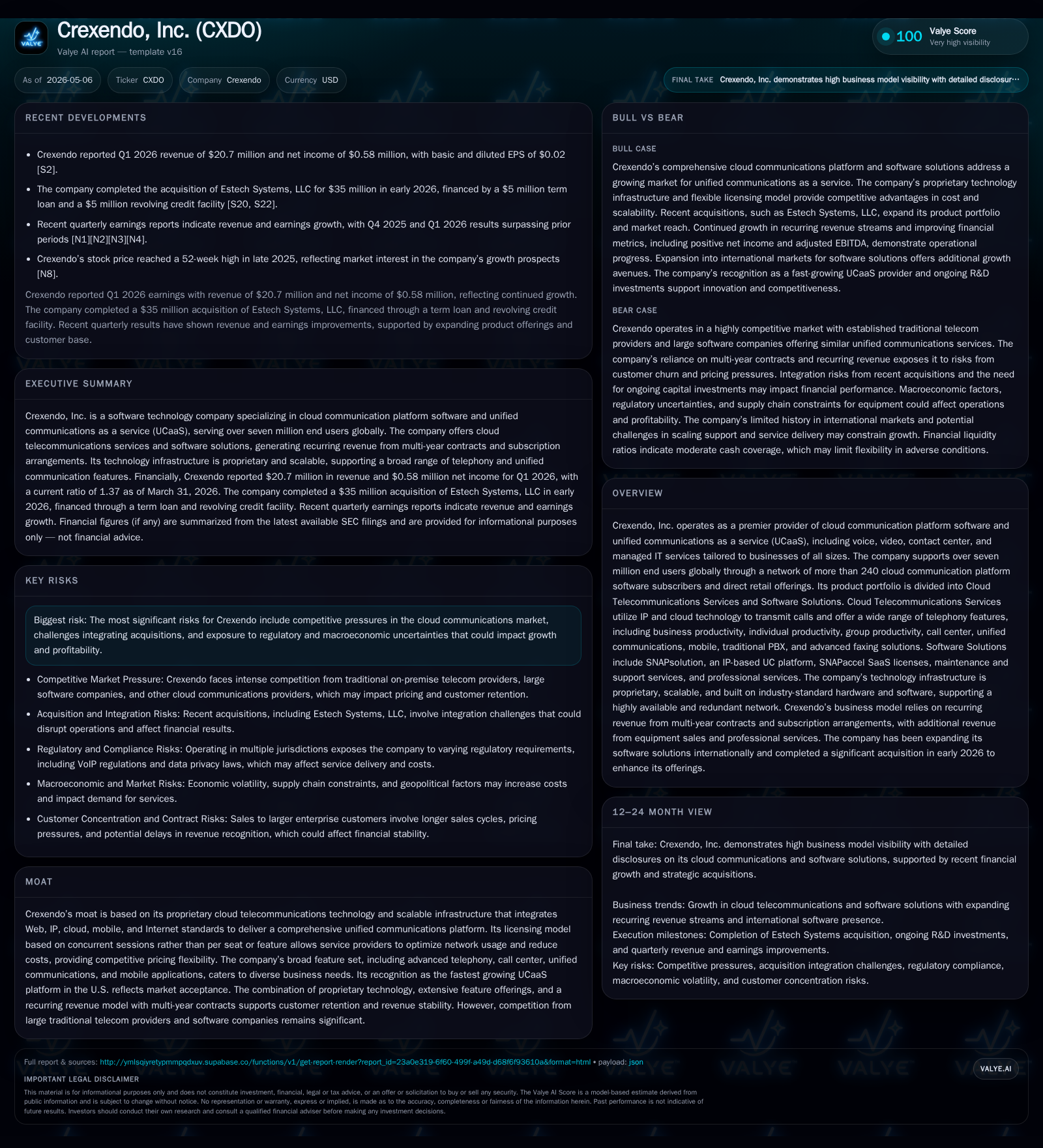

Crexendo's Strategic Credit Move and Growing UCaaS Footprint

Crexendo leverages new credit facilities to fuel acquisition-led growth while expanding its cloud communication service platform.

In Q1 2026, Crexendo finalized a $5 million term loan and a $5 million revolving credit line with Wells Fargo to partly fund its $35 million acquisition of Estech Systems, signaling a strategic expansion of its UCaaS offerings. The company continues to generate subscription-based recurring revenue from its proprietary cloud telecommunications platform, which licenses concurrent sessions to optimize network costs for providers. Despite competitive pressures and regulatory risks, Crexendo’s broad feature set, scalability, and growing customer base position it well in the evolving unified communications market. Investor focus will center on integration execution, subscription growth metrics, and financial covenant compliance in the near term.

Latest Operating Update: Acquisition and Financing Catalysts

Crexendo’s latest quarterly filing on May 5, 2026 marked a pivotal update with the announcement of a new Credit Agreement executed on May 1 with Wells Fargo Bank providing two distinct facilities: a revolving line of credit up to $5 million and a $5 million term loan [S2][S3]. This financing package primarily funded the recent acquisition of Estech Systems, LLC for approximately $35 million—a transaction combining cash ($27.3 million) and stock issuance valued at $7.7 million [S3][S18]. Estech contributes cloud-based as well as on-premises phone systems products that can broaden Crexendo’s UCaaS solution mix.

Q1 operational results also reflected underlying positive momentum with the company beating both earnings and revenue estimates according to Nasdaq coverage on May 5 [N1][N2]. This combination of capital raise-backed inorganic expansion alongside organic performance improvement provides a near-term catalyst in Crexendo’s growth narrative.

Business Model and Product Overview: Architecting Scalable UCaaS Solutions

Crexendo generates its revenues primarily through multi-year subscription contracts tied to its cloud telecommunications services alongside broadband Internet services, managed IT solutions, software license sales, and device-as-a-service offerings [S1]. A notable aspect is their proprietary licensing model based on concurrent sessions rather than traditional per-seat or per-feature billing [S1][S12], enabling telecom service providers to oversubscribe networks efficiently—driving volume growth and lowering the cost per user.

The core product portfolio divides into two main categories:

- Cloud Telecommunications Services: Deliver call transmission over IP/cloud technology featuring extensive telephony functionalities such as unified communications (voice/video), call center capabilities, mobile integrations, traditional PBX replacements, advanced faxing, and productivity suites accessible via a single identity regardless of device [S1].

- Software Solutions: Including SNAPsolution (IP-based unified communications platform), SNAPaccel SaaS licenses sold as subscriptions with maintenance/support contracts, plus professional services like consultation and installation bundled variably [S1][S12].

The business retains strong recurrence given contractual terms typically spanning 36 to 60 months combined with activation fees recognized over contract tenure or at device installation [S1]. This structure supports predictability and stable cash flow generation integral for scaling investments like acquisitions.

Competitive Positioning within the Cloud Communications Ecosystem

In an increasingly crowded UCaaS market dominated by large incumbents and agile cloud-native entrants alike, Crexendo distinguishes itself via its technology-driven moat formed around proprietary integrated infrastructure combining Web, IP, cloud networking protocols alongside mobile standards [S1]. The licensing model based on concurrent session thresholds rather than fixed per-user seats lends pricing flexibility to service partners enabling optimized network utilization.

The extensive feature set addressing SMBs through larger enterprises—including voice/video communications, contact centers, mobility applications, and device offerings—broadens appeal across customer segments while fostering switching cost advantages due to customization potential. However, competition remains intense from Tier 1 carriers offering bundled services and from emerging smaller platforms pushing aggressive pricing or innovative workflows.

Customer retention is bolstered through recurring contract models lasting multiple years coupled with ongoing software maintenance agreements. Yet sustaining differentiation will require continuous investment in platform enhancements given the relentless pace of innovation in unified communications technologies.

Growth Drivers: Market Penetration, Channel Expansion, and Technology Integration

Several structural factors underpin Crexendo’s growth prospects:

- Post-Pandemic UC Adoption: Continuing demand from organizations embracing hybrid work models fuels uptake of unified communication platforms integrating voice/video/contact center functions.[N2]

- Inorganic Expansion: The Estech acquisition enhances product breadth particularly into hybrid cloud/on-premises phone systems positioning for customers preferring mixed deployment topologies [S18][S3].

- Managed IT Services Growth: Augmenting core telecom offerings with managed IT solutions increases wallet share per client while catering to increasing outsourcing trends among SMBs.

- Bundled Licensing & Hardware Sales: Combining software licenses with hardware device-as-a-service models unlocks steady equipment financing revenue streams complementing subscription cash flows.

Key performance indicators such as Annualized Exit Monthly Recurring Subscriptions (AERR) serve as forward-looking signals of subscription revenue trajectory allowing internal strategy calibration [S12][S13]. Management’s ability to scale distribution channels and retain existing customers while expanding user footprints drives sustainable top-line growth potential.

Risks & Constraints: Competitive Pressures, Regulatory Hurdles, and Integration Challenges

Despite promising fundamentals Crexendo faces tangible headwinds:

- Intense Competition: Market saturation from major telecom incumbents combined with aggressive cloud-based UCSP startups may suppress pricing power limiting margin expansion or necessitate additional marketing spend [S20].

- Regulatory Complexity: As a VoIP provider operating numerous states as a CLEC and handling cross-jurisdictional service delivery subject to varying FCC/state commission regulations plus data privacy laws presents ongoing compliance burden potentially limiting geographic expansion or adding operational costs [S24][S25].

- Acquisition Integration Risks: The sizable Estech purchase poses execution risks including cultural mismatch, technology unification challenges, customer attrition risk during transition phases or increased operational expenses diluting near-term earnings [S21][S26].

- Legacy Legal/Regulatory Inquiries: Historical investigations related to discontinued seminar operations remain open-ended potentially imposing contingent liabilities or reputational effects if escalated formally impacting business continuity or stock volatility [S4][S5].

- Macroeconomic Sensitivities: Fixed pricing multi-year contracts limit pricing agility amid inflationary pressures; economic slowdowns may reduce enterprise budgeting cycles affecting renewal rates or new wins,[S20].

Near-Term Watchpoints: Operational Milestones and Financial Guidance

Investor focus should prioritize:

- Tracking quarterly AERR developments as leading indicators of subscription revenue sustainability originating organically or via newly acquired customer bases [S12][N1].

- Progress updates on Estech Systems integration encompassing technology consolidation timelines plus retention benchmarks critical to justifying acquisition valuation multiples [S18][N2].

- Adherence to financial covenants embedded within the new Credit Agreement chiefly total net leverage ratio limits plus fixed charge coverage ratios that govern future borrowing capacity and refinancing flexibility [S3][S8].

- Pricing/mix shifts in subscription plans reflecting competitive adjustments or upsell initiatives influencing average revenue per user metrics.

- Any announced guidance revisions transparently communicating management’s operating outlook amidst competitive/regulatory backdrop [N2][N3].

Financial Snapshot: Balance Sheet Strength and Capital Structure

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Current assets | $23mm | |

| 2026-03-31 | ||

| Current liabilities | $17mm | |

| 2026-03-31 | ||

| Current ratio | 1.37x | |

| 2026-03-31 |

Source: SEC companyfacts cache [F1].

Crexendo exhibits a solid liquidity profile entering mid-2026 anchored by current assets of approximately $23 million against current liabilities near $16.8 million producing a current ratio of about 1.37 indicating reasonable short-term coverage capacity [F1][S2]. Cash & equivalents stood near $3.7 million at quarter end consistent with healthy working capital availability [F1].

The recent capital structure change introduces roughly $5 million in term debt bearing interest rates tied to total net leverage ratio plus term SOFR between 2.25%–2.75% alongside an equally sized revolving facility both maturing May 2029—a moderate increase reflecting targeted acquisition funding rather than leveraging for operational shortfalls [S3][S8].

| Metric | Value | As of |

|---|---|---|

| Cash & Equivalents | $3.7M | |

| 2026-03-31 (Q1) | ||

| Current Ratio | 1.37 | |

| 2026-03-31 | ||

| Total Debt | Approx. $5M* | |

| 2026-05-01 |

*Includes new Term Loan from Credit Agreement filed May 1, 2026 (S3).

The capital injection through indebtedness reflects management’s commitment toward disciplined financing aligned with strategic growth rather than aggressive balance sheet risk taking.

Disclaimer: This analysis is based solely on publicly available information including SEC filings [F1], recent press releases and industry news as referenced. It does not constitute investment advice or recommendations. Readers should perform their own due diligence before making any investment decisions.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments