Ducommun Inc. Earnings Slide Reflects Aerospace Cyclicality and Supply Chain Pressures

Sharp earnings declines in 2025 underscore industry cyclicality and supply chain challenges impacting Ducommun’s aerospace-focused manufacturing.

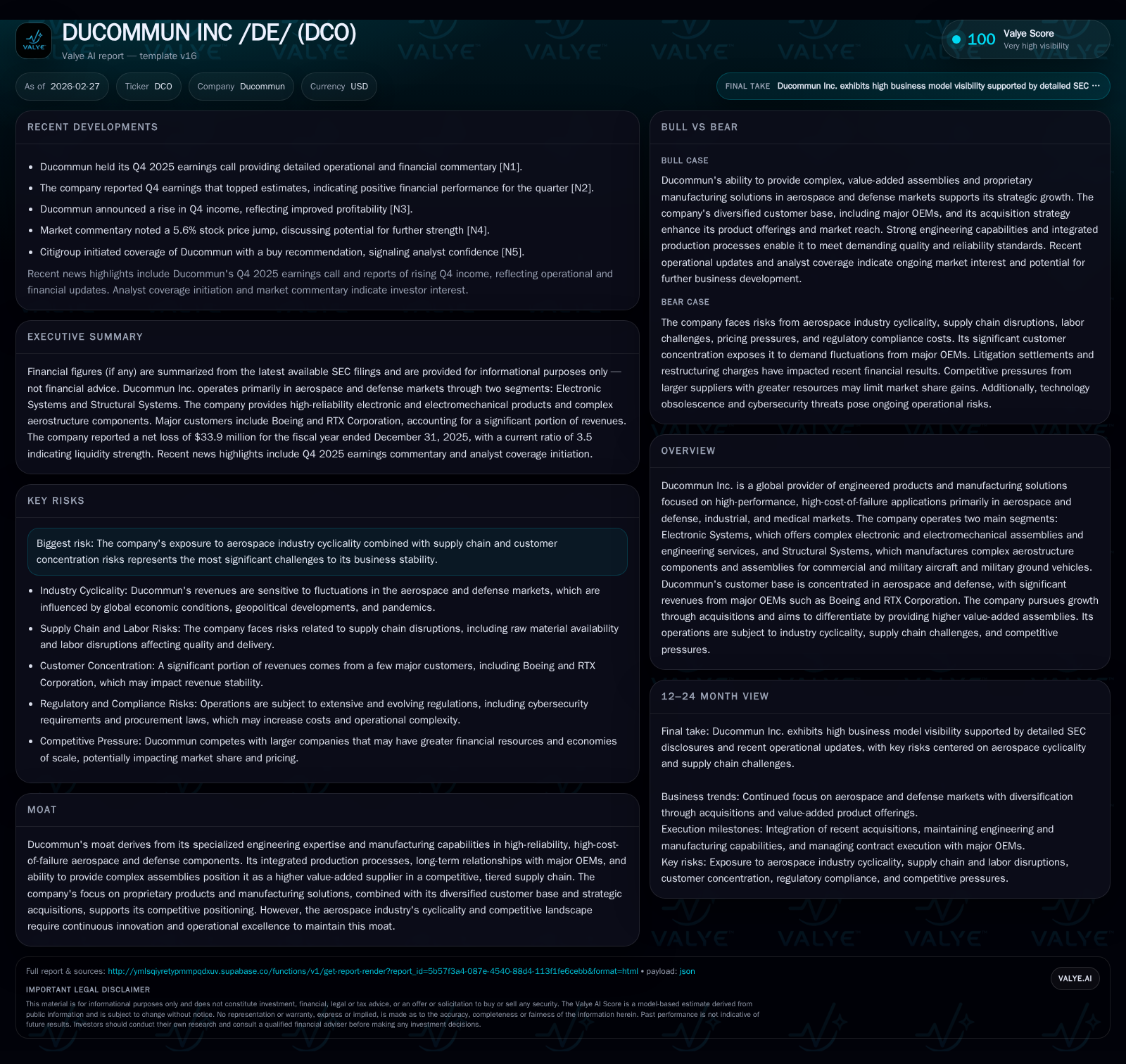

Ducommun Inc. experienced a marked reversal in profitability during fiscal 2025, seeing operating income swing significantly negative despite largely stable revenues. This downturn follows several years of solid growth supported by acquisitions and robust aerospace demand. The company’s reliance on major OEMs such as Boeing and RTX intensifies exposure to sector cyclicality and supply chain disruptions impacting margin profiles. Liquidity remains adequate post-refinancing, but negative operating cash flow and free cash flow along with margin pressures highlight ongoing operational challenges. Near-term prospects hinge on backlog conversion and successful execution of strategic growth initiatives.

From Expansion to Earnings Contraction: Reviewing Ducommun’s Historical Growth

Ducommun Inc.’s financial trajectory through recent years showcases a notable inflection point in fiscal year 2025. The company’s revenue base has remained broadly stable after recovering from mid-decade volatility, settling near $142 million in both 2016 and 2017 as per historical records ([F1]). However, the sharp contrast emerges when examining the span from 2022 through 2025.

Between 2022 and 2024, Ducommun sustained meaningful operating income growth — from roughly $39.8 million in 2022 to $52.2 million in 2024 — emblematic of expanding operational scale largely fueled by acquisitions and strong aerospace demand conditions. Net income followed a similar upward path ascending to nearly $31.5 million by the end of 2024 ([F1]). Operating cash flows during this period reinforced the earnings strength with consistent generation around $31–34 million annually while capital expenditures fluctuated but remained substantial due to investments supporting engineered product capabilities.

Yet in fiscal 2025, this momentum was abruptly halted as operating income swung to a significant loss of $32.3 million (a nearly -162% YoY change) alongside a net loss of $33.9 million ([F1]). Operating cash flow deteriorated into negative territory totaling -$33.4 million—a reversal that signals acute working capital or operational disruption coupled with rising costs ([F1]). Incremental capex spending rose modestly by close to eight percent highlighting continued deployment against legacy investments even as profitability contracted.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -34 | -33 | -32 | 15 | -207.8% |

| 2024 | 31 | 34 | 52 | 14 | +97.7% |

| 2023 | 16 | 31 | 29 | 20 | -44.7% |

| 2022 | 29 | 33 | 40 | 20 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -49 | -5.1 |

| 2024 | 20 | 4.6 |

| 2023 | 12 | 2.5 |

| 2022 | 13 | 5.5 |

Source: SEC companyfacts cache [F1].

Note: Revenue figures shown only where available; historical trends primarily illustrate earnings volatility tied to operational dynamics ([F1]).

How Aerospace Cyclicality and Customer Concentration Shape Current Challenges

Ducommun's fortunes remain intimately tied to the broader aerospace and defense industry's cyclical nature which is influenced by global economic conditions, geopolitical uncertainties, and airline demand cycles ([S22]). Approximately 96% of net revenues originate from aerospace and defense end-use markets demonstrating critical dependency on aircraft OEMs such as Boeing and RTX Corporation ([S4], [S6]). Specifically, Boeing accounted for about 13% of Ducommun’s revenues while RTX contributed roughly an additional 18%, cumulatively forming over one-third of total revenue exposure ([S4], [S6]).

Such customer concentration exposes Ducommun acutely to any shifts in OEM production rates or order deferrals common during cyclical downturns or supply chain disturbances ([N1], [S9]). These OEMs’ supply disruptions cascaded downstream affecting Ducommun’s ability to meet delivery deadlines precisely during periods when raw material lead times also inflated costs ([S23], [N1]). Contract structures often emphasize firm fixed price arrangements with rights allowing customers termination for convenience which further encumbers revenue predictability during volatile demand environments ([S20], [S26]).

Engineering Differentiation Versus Margin Compression: Analyzing Profitability Trends

Central to Ducommun’s competitive position is its capability in engineering highly complex electronic systems and aerostructural assemblies designed for high-cost-of-failure aerospace applications—where reliability cannot be compromised ([S10], [S21]). This specialization is reflected in their dual-segment focus: Electronic Systems delivering advanced electromechanical assemblies including circuit card assemblies; Structural Systems providing complex aero components for military and commercial platforms ([S10]).

However, delivering added engineering value has coincided with persistent margin compression throughout late-cycle aerospace expansion phases principally due to inflationary pressures on critical raw materials like aluminum and titanium alongside episodic supply chain bottlenecks ([N1], [S23]). Operating income margins drastically deteriorated from prior positive returns down into significant losses signaling that increased input costs were not fully recoverable via pricing adjustments given intense competition at various supply chain tiers ([N1], [S23]). The transition toward more customized higher value-added assemblies infers elevated labor content and manufacturing complexity intensifying cost absorption risks particularly when customer pricing power wanes.

Debt, Liquidity, and Capital Structure: Cushioning Against Industry Volatility

Despite operational challenges, Ducommun maintains substantial liquidity buffers following its refinancing activities completed late in fiscal year 2025 ([S11], [S16]). The company replaced its prior credit facilities with the '2025 Credit Facilities' incorporating a $200 million senior secured term loan maturing in November 2030 alongside an expanded revolving credit facility up to $450 million also maturing in November 2030 ([S11], [S16]).

As of December 31, 2025, outstanding long-term debt stood at approximately $305 million bearing an average variable interest rate near six percent ([S11]). The revolving credit portion offers around $200 million remaining unused borrowing capacity after factoring standby letter commitments providing ample breathing room amid short-term liquidity demands ([S5], [S25]). Compliance with all financial covenants was maintained at year-end including leverage ratios calibrated against EBITDA adjusted for non-cash items indicating prudent balance sheet management given cyclical exposures ([S7], [S13]).

Nevertheless, variable rate debt exposes Ducommun to rising interest cost risk while covenant constraints may limit financial flexibility on future strategic moves or acquisitions unless offset by strong cash flows or deleveraging efforts ([S13]). Interest rate swaps covering $150 million of notional amount reduce immediate exposure somewhat but residual variability persists over the life span.

What Lies Ahead? Backlog, Market Dynamics, and Strategic Growth Opportunities

Looking forward, Ducommun reported backlog growth reaching approximately $1.20 billion as of December-end 2025 representing firm fixed price orders expected within the next two years ([S17], [N1]). Approximately seventy percent of this backlog is anticipated to translate into revenue during calendar year 2026 providing relative visibility into near-term business volume amidst uncertain macroeconomic conditions.

Demand signals from major OEMs remain cautiously optimistic with Boeing projecting sustained fleet growth over decades balanced against ongoing challenges like elevated fuel prices and geopolitical tensions that could affect new orders globally ([S17]). Airbus forecasts similarly align citing Asia-Pacific as a key region driving aerospace service demand expansion despite prevailing headwinds.

Strategically, Ducommun continues pursuing growth through targeted acquisitions aligned with broadening product scope in aerodynamic systems or integrated electronics aiming to entrench itself further up the value chain beyond mere component supplier status ([S10], [N1]). However, given current margin stresses plus cyclic risk factors cited repeatedly by management calls or filings, execution risk remains significant.

Capital Allocation Review: Cash Flows, Returns, and Shareholder Distributions

A thorough examination reveals cash flow generation turning sharply negative in fiscal year end-2025 contrasted with prior robust positive free cash flow performance exceeding $20 million annually from preceding years ([F1]). The net operating cash outflow totaling over $33 million indicates potential working capital build or delayed receivables collections coupled possibly with inventory accumulation amid production delays or retooling efforts—all inflaming liquidity usage despite solid revenue volume.

Consequently free cash flow (operating cash flow less capex) declined by approximately $48.6 million placing pressure on discretionary capital allocation priorities such as shareholder returns currently absent given no recent dividend payouts or share repurchase initiatives documented since before FY2013/14 periods ([F1], [N3]).

The return on equity approximates negative five percent (-5.1%), underscoring deteriorated profitability juxtaposed against an equity base expanded through retained earnings addition over prior profitable cycles indicative of transitional stress rather than structural impairment at this stage ([F1]). Management appears focused presently on preserving balance sheet strength rather than extracted shareholder returns amidst ongoing recovery efforts.

Valye Analyst Take: Key Milestones and Risks to Monitor for Ducommun

As Ducommun navigates through what can be best described as a cycle-induced earnings trough exacerbated by persistent supply chain issues impacting cost structures and delivery schedules, key milestones will include observing margin stabilization developments through succeeding quarterly reports alongside backlog conversion success rates.

Liquidity maintenance within covenant thresholds combined with measured deleveraging—should market conditions permit—will also constitute important markers toward restoring investor confidence that current setbacks are transitory rather than systemic failures.[N4],[S19]

Critical risks remain tightly linked to aerospace industry cyclicality compounded by concentrated dependency on few major OEMs subject again to pandemic hangovers or geopolitical shocks reducing aircraft build rates or shifting program priorities unexpectedly.[S19] Further customer pricing pressure introduces uncertainty regarding sustainable margin recapture even as raw material cost inflation normalizes over time.

Investors should watch upcoming contract awards announcements—especially those involving more integrated manufacturing solutions—and monitor incremental steps toward innovation-led differentiation as bellwethers validating longer-term competitive positioning despite prevailing turbulence.

This report synthesizes publicly available regulatory filings and news sources up to February 27, 2026 without offering investment advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments