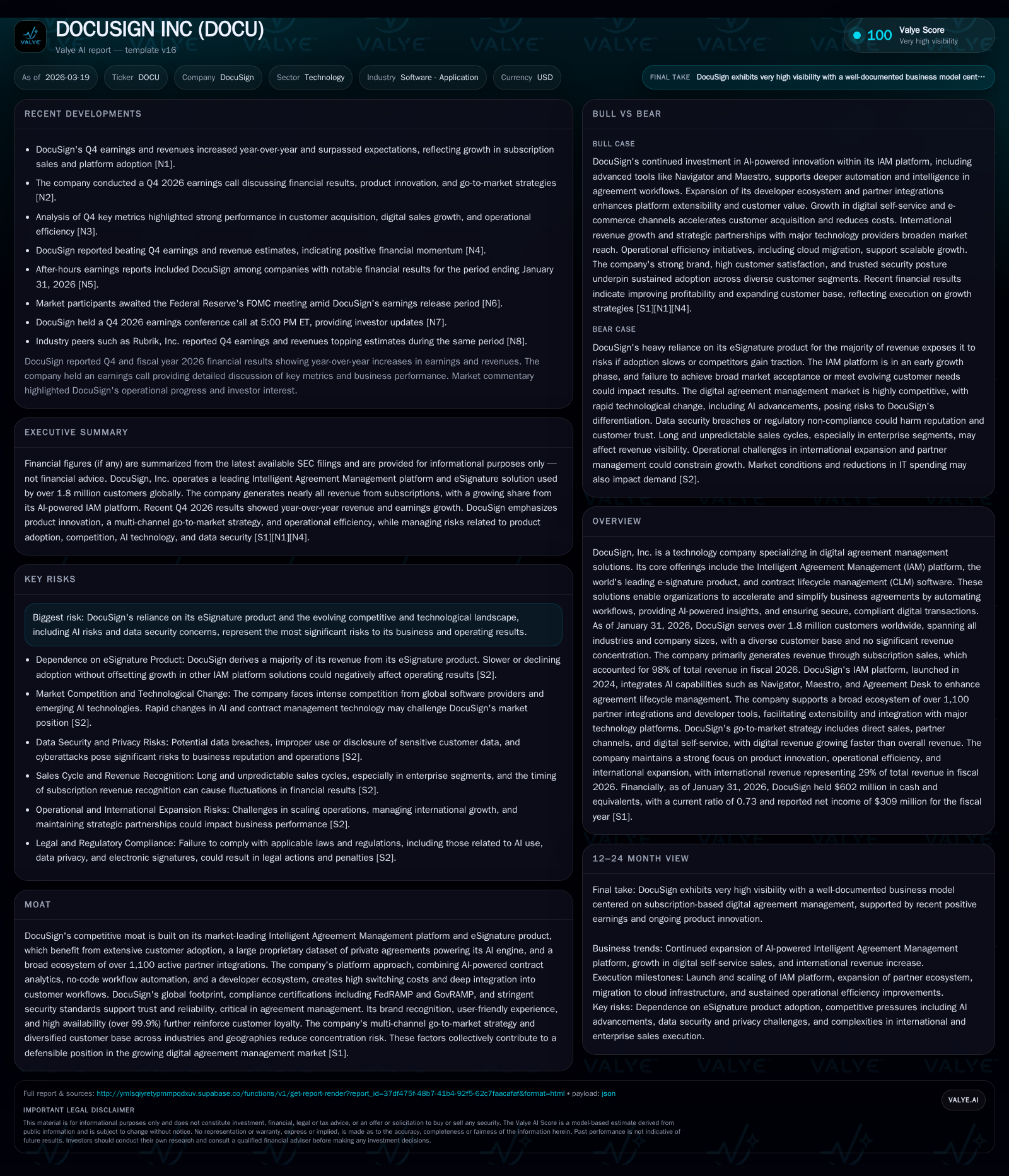

DocuSign’s Fiscal 2026 Growth Rebound Powered by IAM Platform Expansion

DocuSign’s strategic shift from eSignature to the Intelligent Agreement Management platform fueled a substantial profitability upswing in fiscal 2026.

After several years of uneven financial results, DocuSign posted a nearly 50% year-over-year increase in operating income in fiscal 2026, driven by adoption gains of its expanded Intelligent Agreement Management (IAM) platform. Subscription revenue grew as IAM broadened the company’s addressable market beyond legacy eSignature products, supported by a diversified customer base exceeding 1.8 million. Strong free cash flow generation enabled significant share repurchases as DocuSign balanced investments in innovation with capital returns, while cybersecurity and AI-related risks warrant close monitoring. Absent explicit forward guidance, investors should watch expansion of IAM deployments and partner ecosystem performance for clues on sustaining momentum.

From Headwinds to Tailwinds: The Turnaround in Profitability

DocuSign’s fiscal trajectory illustrates a pronounced shift from earlier volatility toward robust profitability in FY2026. Operating income swelled by approximately 49.3% year-over-year, climbing to $298.6 million while net income paradoxically declined from the previous fiscal year’s exceptionally high $1.07 billion—reflecting possibly one-off items or tax benefits not repeating this cycle [F1]. Operating cash flow maintained solid momentum at $1.165 billion (up from $1.017 billion), with capital expenditures increasing moderately by nearly 10% to $106 million [F1]. The resulting free cash flow approximated $1.06 billion underpinning significant shareholder returns via a substantial $869 million share repurchase program that more than doubled the prior year’s buyback activity [F1]. Equity stood at about $1.92 billion yielding an approximate return on equity of 16%, indicative of enhanced capital efficiency entering the current period.

This turnaround is anchored fundamentally in the success of DocuSign's Intelligent Agreement Management platform expansion and highlights a transition away from reliance on legacy eSignature revenues toward broader AI-powered solutions with deeper enterprise integration.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2026 | 309 | 1165 | 299 | 106 | -71.1% |

| 2025 | 1068 | 1017 | 200 | 97 | +1343.5% |

| 2024 | 74 | 980 | 32 | 92 | +175.9% |

| 2023 | -97 | 507 | -88 | 78 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2026 | 869 | 1059 | 16.1 |

| 2025 | 684 | 920 | 53.3 |

| 2024 | 146 | 887 | 6.5 |

| 2023 | 63 | 429 | -15.8 |

Source: SEC companyfacts cache [F1].

The Pivotal Role of IAM Platform in Driving Subscription Growth

The Intelligent Agreement Management (IAM) platform launched in April 2024 represents a transformative step beyond DocuSign’s foundational eSignature product by anchoring itself as the central system of record for comprehensive agreement workflows. IAM bundles AI-driven tools like Navigator — a sophisticated repository for millions of agreements offering actionable contract insights — Maestro for no-code workflow automation and Agreement Desk which streamlines collaboration across all agreement requests [S12], [S13].

IAM subscriptions now represent approximately 10.8% of annual recurring revenue during FY26 after becoming available globally in major geographies across all customer segments through direct sales and partner channels [S15]. Transitioning the IAM offering to user-based subscription pricing allows addressing nuanced departmental usage patterns while maintaining legacy envelope counting methods mainly used for standalone eSignature revenues which remain dominant currently [S15].

This platform strategy enables scalable ‘land-and-expand’ customer growth through digital self-service captures initially small or department-level users (accounting for about 15% of FY26 digital revenue) before expanding footprint via high-touch commercial sales teams targeting broader enterprise use cases—a model known to yield improved customer lifetime value in SaaS markets where initial trial friction is minimized yet deep integration creates switching costs over time [S4], [S5].

Expanding Customer Base and Market Penetration Dynamics

DocuSign serves over 1.8 million customers worldwide spanning industries and sizes with balanced revenue contribution without material concentration risk; the largest customer accounted for less than 10% of revenue at fiscal year end [S4], [S6], [S9]. Among those customers are roughly 280,000 direct enterprise and commercial accounts managed via field sales or partners—an increase versus prior periods indicating successful penetration into higher-value segments with extended contract values exceeding $300k growing modestly to over 1200 accounts at fiscal year end FY26 [S4], [S9].

Geographically international revenue contributed nearly 29%, growing faster than domestic sales consistent with product availability expansions including feature compliance such as EU eIDAS standards through Signature Based Solutions ("SBS") technology adoption facilitating addressable market growth outside common law jurisdictions—efforts supported by compliance credentials like FedRAMP Moderate and GovRAMP authorization further underpinning government sector trustworthiness [S7], [S11], [S13].

Strategic partnerships play a fundamental role as well: ties with Microsoft Azure underpin migration efforts alongside co-selling relationships with Salesforce and SAP leverage joint marketing initiatives; broad ecosystems encompass more than a thousand active integrations facilitating embedding Docusign into everyday enterprise workflows along with concerted channel partner reinvestment focusing on ISVs and systems integrators expand reach efficiently across verticals including finance and healthcare niches experiencing increased digital transformation demand patterns [S6], [S8], [S13], [S20].

Balancing Platform Innovation With Competition and Risk

Innovation centered around AI capabilities embedded within IAM offers competitive differentiation by leveraging extensive proprietary contract datasets for model training differentiating precision levels versus generic LLMs or public datasets—enabling highly specialized contract analysis essential for mission-critical applications where accuracy correlates directly to risk mitigation or opportunity discovery potential; nonetheless it ushers considerable operational tradeoffs regarding handling sensitive data within regulatory boundaries exacerbate legal and reputational concerns highlighted repeatedly in risk disclosures emphasizing product acceptance hazards within evolving compliance landscapes plus emerging cybersecurity threat surfaces endemic to SaaS cloud platforms hosting sensitive information internationally [S16], [S19], [S25].

Cybersecurity governance is detailed thoroughly within filings describing multi-tier oversight shared among board audit committees alongside active management-led programs implementing intelligence collaborations with law enforcement; a dedicated Security Governance Council headed by an experienced CISO manages continuous proactive risk detection and incident response readiness bolstered by insurance coverage protecting against material cyber incidents [S1], [S27]. This strategic approach reflects industry best practices critical given the increasing attractiveness of software supply chains as attack vectors.

Meanwhile competitive dynamics intensify chiefly from Adobe Acrobat Sign supplemented by emerging contract workflow vendors integrating AI features internally or offered via public cloud providers; accelerations in foundational LLM capabilities reduce entry barriers potentially eroding differentiation absent rapid innovation cycles requiring sustained R&D investment alongside vigilance on evolving regulatory prescriptions governing AI usage beyond technology feasibility into governance ethics domains [S10], [N12].

Capital Deployment: Buybacks and Cash Flow Trends in FY2026

DocuSign’s disciplined capital allocation balances reinvestments supporting its long-term strategic pillars against significant shareholder returns enabled by sustained cash flow strength. Fiscal year operating cash flow grew by approximately 14.5% to around $1.17 billion supported by an expanding subscription base driving recurring billing stability complemented by improved operating margins reflecting scale benefits [F1]. Capital expenditures rose moderately near $106 million focusing on infrastructure enhancement including cloud migration efforts designed to optimize scalability elasticity responding to global usage patterns [F1], [S18].

The company employed over $869 million in share repurchases during FY26—a marked escalation that signals confidence in capital efficiency improvements and aims to offset dilution effects inherent in tech sector stock compensation while enhancing earnings per share impact [F1]. Dividend issuance appears minimal or absent suggesting focus rests primarily on buybacks and growth investments aligning well with SaaS-stage technology companies prioritizing innovation cycles.

Approximate return on equity calculated using net income dividing equity stands near a healthy ~16%, underscoring effective employment of equity capital despite moderate leverage implied by sub-1 current ratio liquidity metrics reflecting working capital structure nuances noted [F1]. Overall financial flexibility appears robust backed by strong free cash generation capacity.

What To Watch: Upcoming Milestones and Sector Challenges

No explicit numeric guidance was provided for upcoming quarters or years but pertinent milestones are scattered across recent commentary advocating continued ramp of platform adoption especially expanding usage breadth among current enterprise accounts while augmenting partner network vitality through co-development efforts linked to developer ecosystem events showcased since late calendar year 2024 [N2], [N3], [N4], [S20]. Watch closely initiatives tying IAM tightly into leading LLM platforms per beta release announcements integrating ChatGPT and others via Model Context Protocol server pointing toward embedding contextual AI agents assisting complex agreements processing at scale [S13].

Regulatory developments relating to data privacy regimes globally plus evolving scrutiny over AI deployment may influence pace at which certain new features roll out or necessitate additional compliance investments increasing operational cost pressures [S25], while macro considerations center on corporate IT spending trends influenced by Federal Reserve policy shifts affecting renewal timing or deal sizes notably under rising interest rate conditions described broadly across tech sector earnings commentary [N10]. Competitive moves from key rivals Adobe plus emergent niche software players exploiting modular contract management could challenge premium pricing unless differentiated value delivered with visibility expands compellingly.

Potential litigation risks relating to intellectual property remain perennial issues documented involving claims that could divert management focus or impose unforeseen expenses albeit presently not materially impacting results or guidance [S16]. Ongoing cybersecurity vigilance remains paramount given elevated threat environments compromising critical SaaS infrastructures can lead to reputational damage rapidly cascading through client ecosystems relying heavily on uninterrupted access.

This analysis synthesizes publicly available financial reporting extracted from SEC filings including DocuSign's FY2026 Form 10-K together with relevant earnings commentary sourced primarily from Nasdaq-hosted transcripts and articles through March 2026 without conjecture outside verified evidence presented herein. It is intended solely for informational purposes without any recommendation related to investment decisions.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments