Dow Inc.: Navigating Commoditization, Macroeconomic Headwinds, and Strategic Transformation in Chemicals

Dow Inc. confronts a challenging global chemical industry landscape with strategic cost cuts, innovation delays, and a pivot toward operational simplification to sustain its competitive edge.

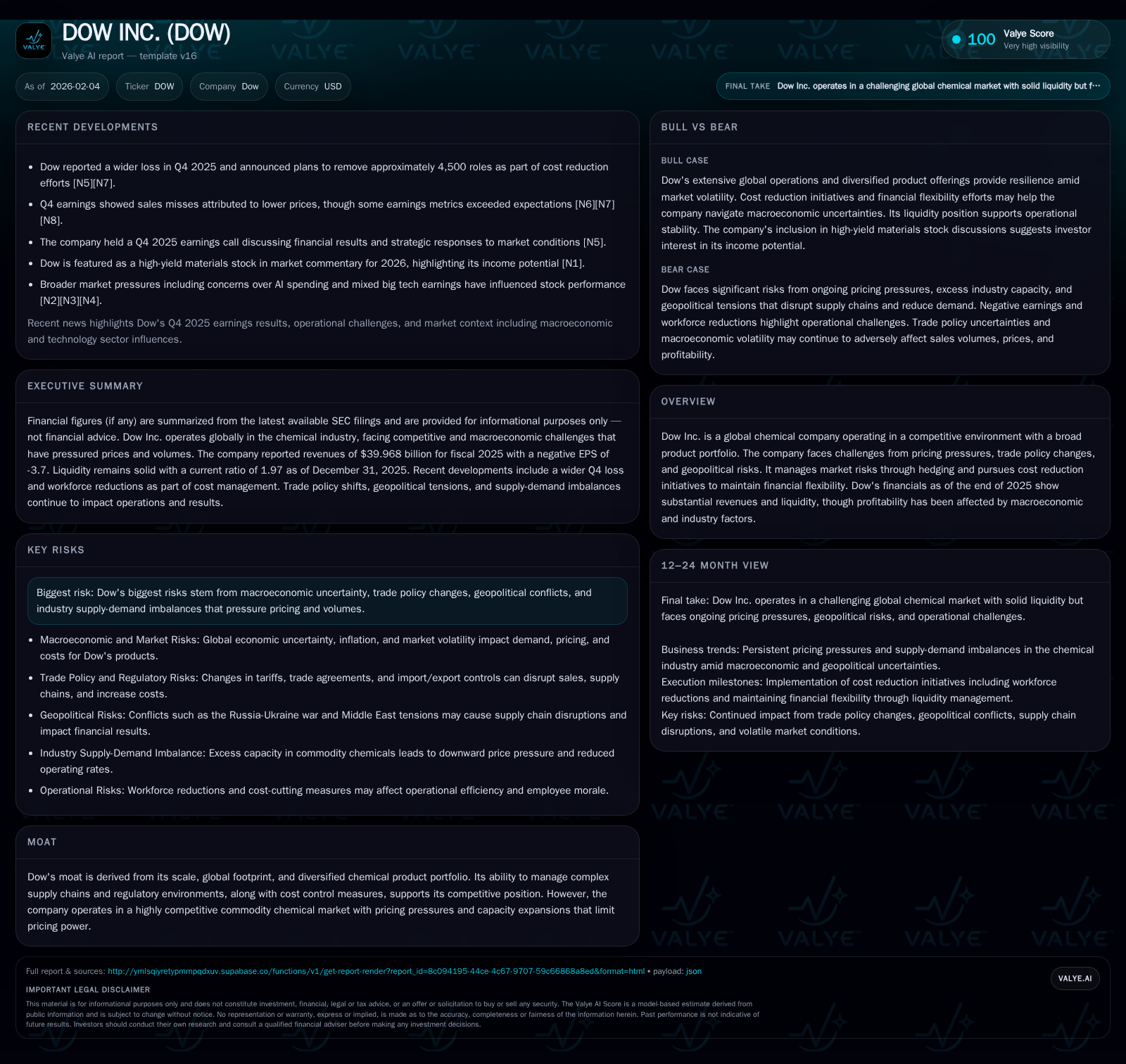

As one of the largest global chemical producers, Dow Inc. operates within a fiercely competitive and commoditized market amidst persistent macroeconomic uncertainties including geopolitical tensions and trade policy shifts. Despite strong revenues and liquidity, profitability is squeezed by pricing pressures exacerbated by overcapacity and economic sluggishness. In response, Dow has launched an ambitious transformation program focused on structural cost reductions, workforce realignment, and streamlining operations, while balancing ongoing investment in sustainability initiatives like its delayed Path2Zero project. These maneuvers aim to bolster near-term earnings prospects and position Dow for resilience amid enduring sector cyclicality.

A Global Giant Challenged: Understanding Dow's Market Landscape

Dow Inc. stands among the titans of the global chemical industry, boasting an extensive portfolio that spans across packaging, specialty plastics, industrial intermediates, infrastructure materials, performance coatings, and more [S1][F1]. This breadth grants Dow significant scale advantages, enabling complex supply chain management across numerous jurisdictions while navigating intricate regulatory frameworks worldwide. Yet scale alone does not insulate Dow from the fundamental challenges facing commodity chemicals.

The company operates in highly competitive arenas characterized by aggressive pricing pressures intensified by capacity expansions from existing rivals and new entrants exporting at anti-competitive economics [S1]. This restricts Dow's ability to command premium pricing despite product quality or service levels—a persistent constraint that keeps margins under tight compression. With such dynamics entrenched industry-wide, sustaining profitability demands continuous operational efficiency improvements and responsive market strategies.

Monetary Weather: Macroeconomics, Trade Policies, and Geopolitical Pressures

2025 was marked by turbulent external conditions undermining Dow’s operational environment [S1][S2]. Global GDP growth slowed significantly against a backdrop of inflationary pressures that squeezed customers’ purchasing power. Against this economic drag lay an evolving trade policy landscape—particularly heightened U.S. tariffs excluding those goods compliant under USMCA—provoking retaliatory tariffs from key trading partners that disrupted material sourcing and increased logistical complexity.

Supplementing these strains are ongoing geopolitical tensions: notably the protracted Russia-Ukraine conflict with resultant sanctions limiting Dow’s investments in affected regions alongside operational restrictions [S2]. Additional volatility derives from Middle East conflicts and regional instability further injecting uncertainty into energy costs and supply pathways crucial for chemical manufacturing. These layered risks collectively dampen demand volume while suppressing selling prices due to oversupplied markets—a harsh climate that materially pressured revenues and cash flows throughout the year.

Financial Health Snapshot: Liquidity Amid Losses

Unfortunately for Dow stakeholders, top-line robustness did not translate into stable bottom-line performance in 2025 [F1][N4][N6]. The company recorded revenues nearing $40 billion yet faced widening quarterly losses—including a marked shortfall in Q4 earnings driven largely by lower average selling prices amid oversupply conditions [N6]. Nonetheless, Dow maintained financial resilience: end-of-year cash reserves approached $3.8 billion complemented by current assets nearly double current liabilities (a 1.97 current ratio) signaling ample liquidity buffers [F1].

This juxtaposition of strong liquidity against loss-making operations reveals an organization wrestling with macroeconomic headwinds while preserving enough runway to implement strategic initiatives without immediate solvency threats.

Transform to Outperform: A Strategic Pivot for Near-Term Stability

In response to persistent margin pressure, January 2026 saw Dow unveil ‘Transform to Outperform,’ an ambitious program designed to yield at least $2 billion in near-term Operating EBITDA improvements principally through simplification of its operating model coupled with accelerated growth agendas [S1][N12]. This transformational blueprint extends beyond earlier cost-saving efforts announced mid-2025.

However promising the potential upside, transformational progress carries short-term costs evidenced by expected restructuring charges between $1.1 billion to $1.5 billion over two years—including severance expenses associated with roughly 4,500 layoffs [N12]. This reflects a dual-edged scenario where disruption may unsettle near-term performance even as it prepares the company for leaner operations aligned with prevailing market realities.

Cost Cuts, Workforce Reduction, and Asset Rationalization: Balancing Act or Shortcut?

The Transform initiative builds on groundwork laid since early 2025 when Dow targeted $1 billion in structural cost reductions including workforce cuts (~1,500 roles) alongside cutting capital expenditure plans from $3.5 billion down to $2.5 billion [S1]. This coincided with strategic rationalization of European asset footprints: closures scheduled through 2027 encompass an ethylene facility in Böhlen (Germany), vinyl assets in Schkopau (Germany), a siloxanes plant in Barry (UK), plus write-offs on non-core corporate assets [S1].

While these moves aim to rightsize capacity in line with profitable demand amid industry cyclicality, they also risk stripping essential capabilities if overly aggressive—underscoring a precarious balance between prudent downsizing versus compromising long-term competitiveness.

Innovation and Sustainability: The Delayed Path2Zero Endeavor

Sustainability remains a pillar of Dow’s corporate identity—embodied most prominently by the Path2Zero project designed as the world’s first integrated ethylene complex achieving net zero Scope 1 & 2 emissions [S1]. Yet macroeconomic uncertainty led to its delay announced twice during 2025 and again early 2026 pushing completion phases into late decade (end of 2029/early 2030) horizons [S1].

Although painful because it defers anticipated ESG-aligned growth drivers particularly in downstream applications like pressure pipe or wire & cable markets where low-carbon credentials increasingly matter—the delay arguably conveys financial discipline amid uncertain demand environments rather than abandonment. It also reinforces the incremental nature of transformational change within legacy-heavy commodity industries.

Governance in Risk-heavy Times: Cybersecurity & Oversight

Beyond external pressures lies another dimension of risk carefully managed within Dow’s governance framework: cybersecurity [S1]. Led by a Chief Information & Digital Officer reporting directly to COO—and supported by specialized teams including a Cyber Security Operations Center—the firm adopts multi-layered incident detection and response protocols ensuring swift containment and escalation channels involving senior executives.

Notably, oversight responsibility rests centrally with the Audit Committee of the Board which receives quarterly reports encompassing threat assessments, mitigation plans, audit findings and training compliance metrics [S1]. Given growing cyber threat sophistication impacting industrial enterprises globally this structured vigilance represents vital safeguarding of operational continuity alongside reputational protection.

Investor Lens: Dividends, Valuation, and Market Sentiment

Dow’s protracted profitability squeeze prompted its Board to halve dividends starting Q3 2025—from previous levels down to $0.35 per share—as part of conserving capital flexibility amidst uncertainty [S1]. This dividend recalibration aligns with prudent capital allocation balancing shareholder returns against funding strategic transformation under earnings pressure.

Market reception has been cautious; mixed earnings reports weighed on share price despite some investor attraction toward yields nonetheless considered elevated within the materials sector [N14][N10]. The narrative highlights tradeoffs inherent between income-seeking objectives and appreciating underlying operational recovery prospects.

Where Next? Outlook Amid Persistent Industry Cyclicality

Looking ahead Dow faces no simple path out of entrenched cyclical industry headwinds magnified by global economic fragility [S1][F1][N8]. Supply-demand imbalances driven by capacity expansions globally will likely keep pricing subdued near term even if eventual demand normalization provides relief later in the decade.

Execution of ‘Transform to Outperform’ thus represents both necessary recalibration under duress—and foundational positioning—in anticipation that operational agility combined with sustainability investments can restore competitive differentiation over time. How effectively Dow navigates continued geopolitical uncertainties, trade friction evolutions, inflationary pressures alongside technological disruptions will shape whether it emerges more resilient or remains mired within commoditized constraints.

This analysis synthesizes available regulatory filings and recent disclosures related to Dow Inc.'s operations through early 2026 without issuing investment recommendations or price forecasts. It aims instead to provide a measured assessment grounded in publicly reported facts enriched with context from sector dynamics known broadly at this time.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments