Direct Digital Struggles with Liquidity and Revenue Collapse While Launching Growth Initiatives

The company reports severe financial distress amid ongoing operational setbacks, but introduces a new digital marketing product to regain traction.

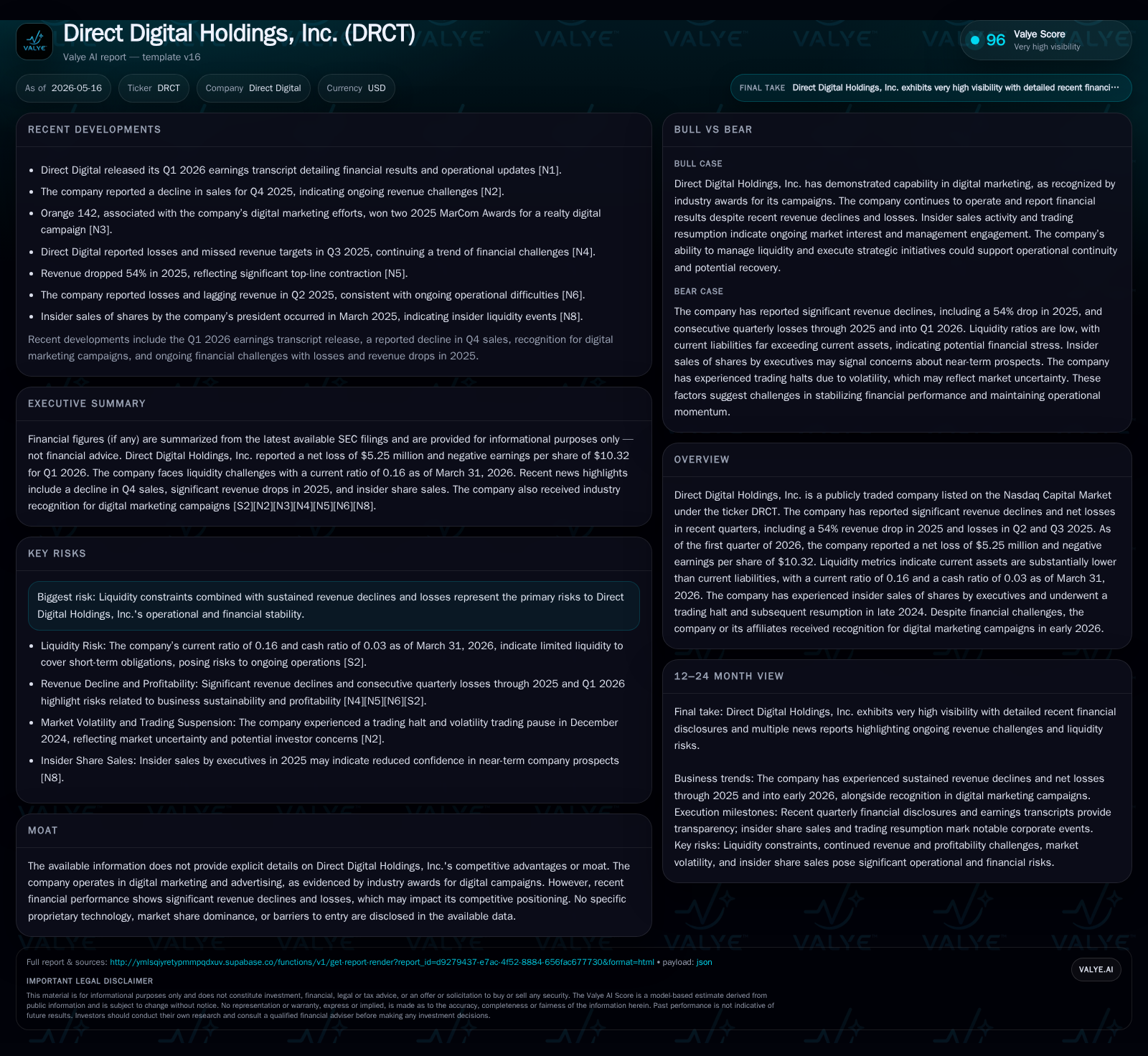

Direct Digital Holdings, Inc. reported a net loss of $5.25 million for Q1 2026, continuing a trend of significant revenue decline and liquidity constraints that have raised going concern doubts. Despite these financial challenges, the company launched Ignition+, a new digital marketing platform targeting enterprise clients to drive future growth. The firm is also negotiating credit facility amendments and pursuing equity raises to address near-term liquidity pressures. While industry recognition for marketing campaigns highlights operational capability, sustained revenue declines and high leverage pose meaningful risks to stability.

Recent Operating Update

Direct Digital Holdings filed its latest quarterly report (10-Q) on May 15, 2026, revealing persistent operational challenges marked by continued losses and cash flow difficulties [S2]. For the quarter ending March 31, 2026, the company posted a net loss of approximately $5.25 million and negative earnings per share of $10.32 [F1][N1]. This follows a broader pattern in 2025 where revenues fell by over half (54%), severely squeezing top-line growth and profitability.

Liquidity remains under acute pressure: current assets stood at just $4.4 million against current liabilities exceeding $28 million, resulting in a razor-thin current ratio of 0.16 as of Q1-end [F1][S2]. The firm's capital structure shows total debt around $17 million with a comparable net debt burden due to low cash balances (~$0.8 million) [F1]. The company has breached certain covenants related to minimum cash balances and EBITDA thresholds but has obtained lender waivers to avoid immediate default action while it negotiates amendments to extend flexibility [S6][S28].

Despite these stresses, management announced efforts to pivot growth via a new product launch—Ignition+—which targets driving increased digital marketing spend from existing customers while attempting to attract new enterprise clients entering digital advertising markets [S19][N1]. Coupled with recognized success in recent digital marketing campaigns (awards reported early 2026), this indicates operational strength in service delivery even amid financial headwinds.

Business Model Overview

Direct Digital operates primarily as a digital marketing services provider with specialization in campaign management leveraging data-driven technologies targeted at destination marketing organizations (DMOs) and other enterprise buyers seeking measurable advertising ROI [S1]. Revenue is generated largely through fees charged for online advertising placements, campaign execution, and data analytics services that optimize ad spend efficiency.

Customers typically engage under contractual arrangements tied to campaign volumes and performance metrics. Revenue fluctuations hinge on client budget allocations driven by travel demand cycles and broader economic conditions affecting destination marketing budgets. The firm's ability to scale depends on both customer retention and onboarding demand driven by marketing innovation and demonstrated effectiveness.

Margins are sensitive to variable costs associated with ad inventory purchases and platform maintenance, while fixed overheads entail technology development investments and personnel expenses [S1]. Recent cost reductions attempted during the downturn aim to improve margin sustainability but have not yet offset the volume-induced revenue declines decisively.

Industry Structure and Competitive Position

The digital marketing industry is highly competitive with numerous established players offering specialized programmatic advertising solutions characterized by rapid technological evolution and constant pressure to innovate around data privacy regulations (e.g., cookie restrictions).

Direct Digital's competitive position appears challenged due to its shrinking revenue base amid increasing competition from better-capitalized firms with proprietary advertising algorithms or deeper client relationships in more diversified end-markets [S1]. There is no indication in SEC filings of differentiated proprietary technology or significant barriers to entry supporting a durable moat.

Customer concentration poses risk; reliance on destination marketing organizations – frequently public-private partnerships with cyclical budgets – accentuates earnings variability linked to tourism demand cycles and public funding availability.

Growth Drivers

Product Innovation: Ignition+

The launch of Ignition+ marks Direct Digital's main growth initiative. This platform seeks to enable clients' enterprise-scale access to intentional digital marketing spends through improved targeting capabilities designed for highly measurable outcomes [S19][N1]. Success will depend on client adoption rates, retention improvement among existing customers, and expansion into larger or new market segments.

Equity Fundraising & Refinancing Efforts

Efforts underway include utilizing newly established equity reserve facilities offering up to $11.6 million capital infusion potential as of Q1 2026 along with negotiating credit facility amendments aimed at easing near-term repayment burdens while maintaining operations continuity [S19][S28].

Leveraging Market Recognition

Receiving accolades for campaign effectiveness early in the year enhances credibility with prospective clients amid marketplace skepticism generated by prior trading halts and insider sales events that eroded investor confidence previously.

Risks and Watchpoints

- Liquidity Constraints: Significant working capital deficit ($23.9 million) threatens ability to meet short-term obligations absent successful refinancing or equity raises; going concern doubts remain pronounced [F1][S19].[

- Covenant Compliance Risk: Ongoing breaches create dependency on lender goodwill; failure to secure further waivers could trigger defaults imminently as term loans mature by December 2026 [S6][S28].

- Revenue Recovery Uncertainty: Lack of clarity whether Ignition+ can reverse multi-year revenue declines particularly given competitive intensity and cyclical demand factors affecting core DMO clients.

- Market Perception: Prior insider stock sales combined with past NASDAQ trading halt episodes may deter new investors despite recent operational achievements.[

- Regulatory/Technological Disruption: Potential impacts from evolving privacy rules limiting tracking capabilities or advertising fraud could impair product efficacy.

- Customer Concentration Risk: Revenue reliance on few large DMO customers exposes vulnerability if budgets tighten further or priorities shift abruptly.

What to Watch Next

Key milestones signaling execution progress include:

- Quarterly bookings growth or retention improvement tied directly to Ignition+ adoption rates documented in forthcoming earnings releases.[

- Updates on equity facility drawdowns or successful completion of registered/private offerings enhancing liquidity profile.[

- Lender covenant negotiation outcomes ahead of December loan maturities reflecting financial stability outlook.[

- Any changes in insider ownership patterns or remedial governance measures addressing market confidence concerns.[

- Evidence from client case studies or win announcements leveraging awards received validating solution quality versus peers.

Financial Profile Snapshot (As of March 31, 2026)

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Cash & equivalents | $796000 | |

| 2026-03-31 | ||

| Total debt | $17mm | |

| 2026-03-31 | ||

| Net debt | $16mm | |

| 2026-03-31 | ||

| Current assets | $4mm | |

| 2026-03-31 | ||

| Current liabilities | $28mm | |

| 2026-03-31 | ||

| Current ratio | 0.16x | |

| 2026-03-31 |

Source: SEC companyfacts cache [F1].

[F1]

The capital structure shows elevated leverage relative to liquid assets creating potent refinancing risk ahead of the maturity timeline in late 2026.[S2] Quarterly installment payments have increased since January 2024 reflecting intensifying cash obligations under the term loans[S6], which exacerbate liquidity strain amid weak operating cash flows.

This analysis synthesizes information strictly based on publicly available SEC filings as of mid-May 2026 alongside recent transcript insights without providing investment recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments