Datasea Inc.’s Intersection of Explosive Revenue Growth and Lingering Financial Fragility

Datasea’s steep 2024-25 revenue surge contrasts starkly with persistent net losses and critical liquidity warnings.

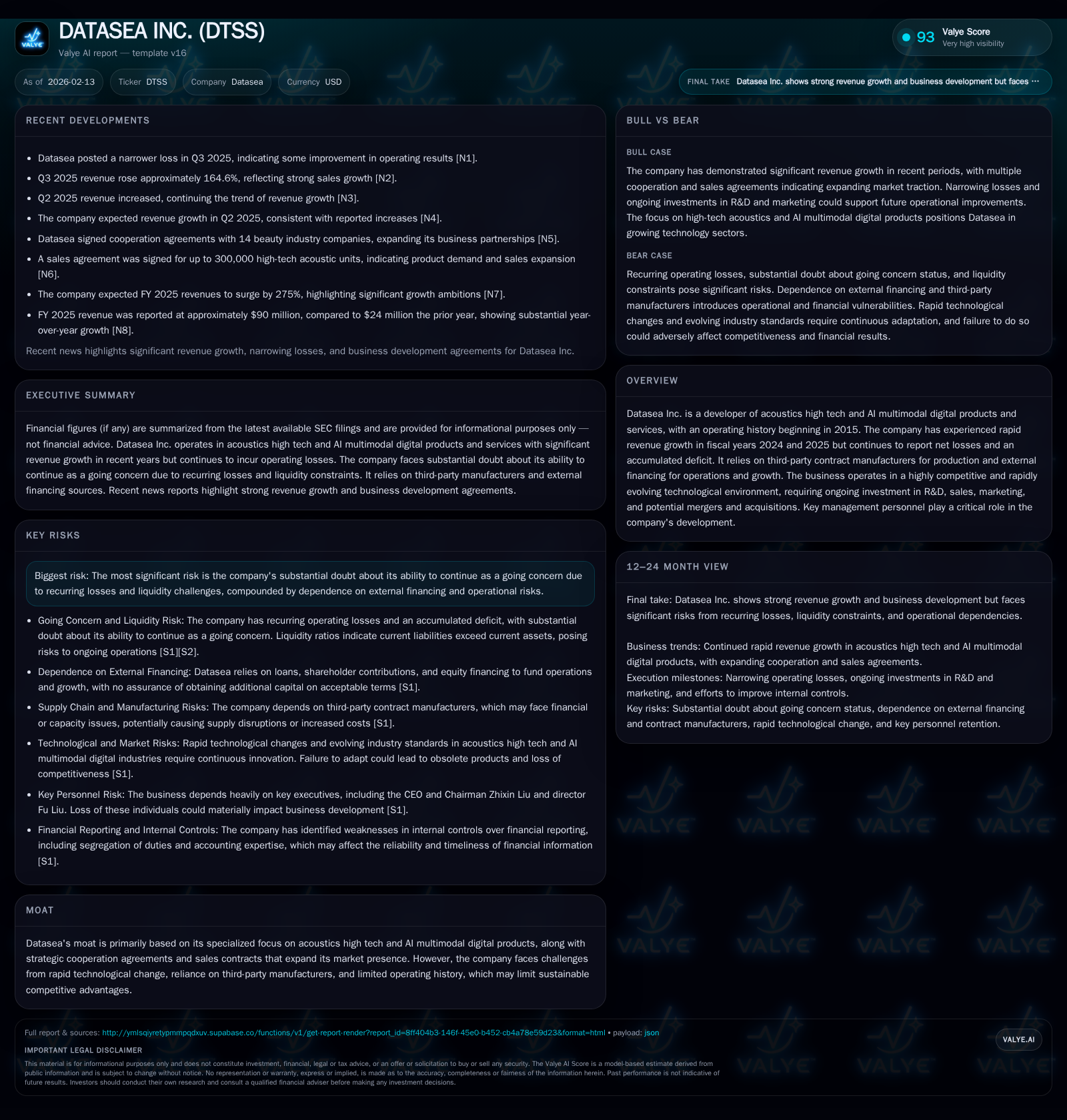

Datasea Inc., specializing in acoustics high-tech and AI multimodal digital products, has recorded nearly 200% revenue growth between fiscal years 2024 and 2025. Despite this rapid expansion, the company continues to operate at a loss, raising auditors’ substantial doubt about its ability to continue as a going concern. Reliance on third-party manufacturing and external financing compounds operational risks in a fiercely competitive and fast-evolving technological landscape. Management faces the dual challenge of driving innovation while navigating acute financial constraints.

Navigating the Acoustic AI Frontier: Datasea’s Core Competency

Datasea Inc. was founded in 2015 with a targeted focus on developing acoustics high technology integrated with AI-driven multimodal digital products. This specialization situates Datasea within a demanding space where hardware precision, software intelligence, and user-interface fluidity must harmonize to produce competitive offerings. The Valye report emphasizes this realm as both an opportunity and challenge since rapidly evolving industry standards compel continuous innovation to remain relevant [valye_report_excerpt]. Operating within this sophisticated intersection demands technical prowess that few enterprises can replicate quickly, providing Datasea with a differentiated product profile. Yet, the company’s limited track record tempers expectations; being a relative newcomer constrains historical performance insights investors might typically rely upon.

Revenue Boom vs. Profitability Gap: Dissecting Recent Financials

Datasea’s revenue trajectory from fiscal year 2024 to 2025 was extraordinary—posting $71.6 million in revenue for 2025, an increase of approximately 199% compared to the prior year [S1]. This escalation reflects successful commercial deployments or expanding client adoption of its acoustic AI solutions. Gross profit increased over fourfold during the same period, signaling improving operational leverage. However, despite these encouraging topline dynamics, the company recorded a net loss of roughly $5 million in fiscal 2025, albeit reduced versus the prior year’s $11.38 million loss [S1]. The latest quarterly figures (FY Q2 2026) show a continued struggle with profitability manifesting as roughly half a million dollars net loss while revenue markedly declined to about $13 million during that interval [F1]. This contraction signals challenges sustaining growth momentum or seasonal fluctuations impacting sales volumes.

The disparity between robust revenue gains and persistent net losses underscores underlying cost structures—principally investment-heavy R&D efforts and sales/marketing outlays required to sustain competitiveness in AI-acoustic technologies. It also reveals margin pressures possibly amplified by outsourced manufacturing costs, described later. This dichotomy paints Datasea as a classic growth-stage tech vendor balancing aggressive expansion with cash burn dynamics typical for such profiles.

The Shadow of Doubt: Going Concern and Liquidity Warnings Explored

A prominent theme running through Datasea's SEC filings is an auditor-issued ‘going concern’ explanatory paragraph reflecting substantial doubt about the company’s ability to continue operations absent profitable turnarounds or fresh capital injections [S1]. The firm concluded fiscal 2025 with an accumulated deficit nearing $44.53 million against negative operating cash flows ($2.37 million for FY 2025), down from even larger deficits in prior years [S1]. Moreover, current liabilities exceed current assets (current ratio ~0.6), highlighting short-term liquidity constraints [F1].

These financial stress indicators suggest that without access to new funding sources—including debt or equity—the company's operational viability could be severely impaired. While management expresses confidence about future financing opportunities, these remain contingent on external market conditions beyond firm control including investor appetite for Chinese-operated tech companies like Datasea [S1]. Thus, despite impressive growth signals, the liquidity fundamentals remain precarious requiring close scrutiny by stakeholders.

Dependency Dilemma: The Risks of External Manufacturing and Financing

Datasea outsources its product manufacturing to third-party contract manufacturers rather than maintaining vertically integrated production capabilities [valye_report_excerpt]. This model reduces direct capital expenditures on plant & equipment but brings dependencies on supplier reliability, quality assurance standards, inventory logistics, and cost fluctuations. Any disruption or contractual failure here could delay product availability or increase expenses.

Compounding operational exposures is Datasea's heavy reliance on external financing channels to fund ongoing R&D activities vital in its quickly shifting tech space [S1]. Shareholder loans, capital contributions, and public equity rounds currently provide the lifeblood for continued development and marketing efforts but create dilution risk or debt service burdens if projections slow down or capital markets tighten unexpectedly.

Strategic Moves in a Rapidly Evolving Tech Landscape

The fast pace of technology evolution within acoustics and AI modalities demands continual reinvestment into research platforms alongside proactive marketing initiatives aimed at customer acquisition and retention [valye_report_excerpt]. To survive competitive pressures from better-capitalized incumbents or emerging startups requires nimble strategy adjustments possibly including mergers and acquisitions to fill capability gaps or access new distribution channels [S1]. Frequent technological pivots imply that yesterday’s innovations quickly become tomorrow’s baselines—raising both opportunity ceilings and risk floors.

Such dynamics justify Datasea’s substantial R&D spend despite current unprofitability but depend heavily on management's ability to allocate resources effectively amidst budget constraints.

Management’s Role Amid Fast-Paced Innovation and Financial Pressure

Key personnel are tasked with navigating Datasea through an intricate matrix balancing accelerated product development cycles against meaningful cost control amidst liquidity threats [valye_report_excerpt]. Their stewardship affects everything from securing capital resources through investor relations to operational decision-making that impacts product timelines and quality. The disclosures emphasize leadership's critical function without detailing individual backgrounds or strategic philosophies. Clearly evident is the weight placed on management acumen given the stakes involved.

Effective leadership will be instrumental not only in managing present challenges but in scaling operations sustainably should breakthrough successes materialize.

Moat Realities: Strategic Cooperations Amid Fierce Competition

Datasea's moat principally arises from its specialized domain expertise blending acoustic technologies with AI multimodal digital innovations—a relatively narrow field limiting direct peer competition based purely on technological focus [valye_report_excerpt]. Complementing this are strategic cooperation agreements which help extend market reach beyond organic growth alone.

However, this moat is qualified; rapid tech changes challenge maintaining unique advantages long-term especially given limited IP disclosure or scale economics compared to larger competitors documented. Reliance on collaborations instead of fully proprietary platforms may further inhibit defensibility depending how contractual terms evolve.

Overall, while differentiation exists materially today it carries notable vulnerability embedded within fast-changing industry conditions.

Investor Takeaway: Balancing Growth Potential with Speculative Risks

Datasea presents an intriguing study in contrasts: its nearly tripled revenues between fiscal years signal real product-market acceptance yet sit side-by-side with sustained net losses exceeding $5 million annually and deteriorated liquidity ratios [S1][F1][valye_report_excerpt]. Auditor warnings regarding going concern reflect significant financial fragility requiring serious consideration.

The company operates within a challenging operational model reliant on third-party manufacturing plus cyclical external financing—both introducing uncertainties into stability forecasts. While management endeavors persistently to align innovation investment with growth opportunity horizons, outcomes remain uncertain given nascent operating history.

For investors evaluating Datasea purely through disclosed facts without extrapolation: optimism about potential technological gains must be carefully juxtaposed against clear indicators of financial stress and speculative upside scenarios articulated directly by company risk factors.

Disclaimer: This analysis is for informational purposes only, reflecting data as reported up to early 2026 without providing investment advice or buy/sell recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments