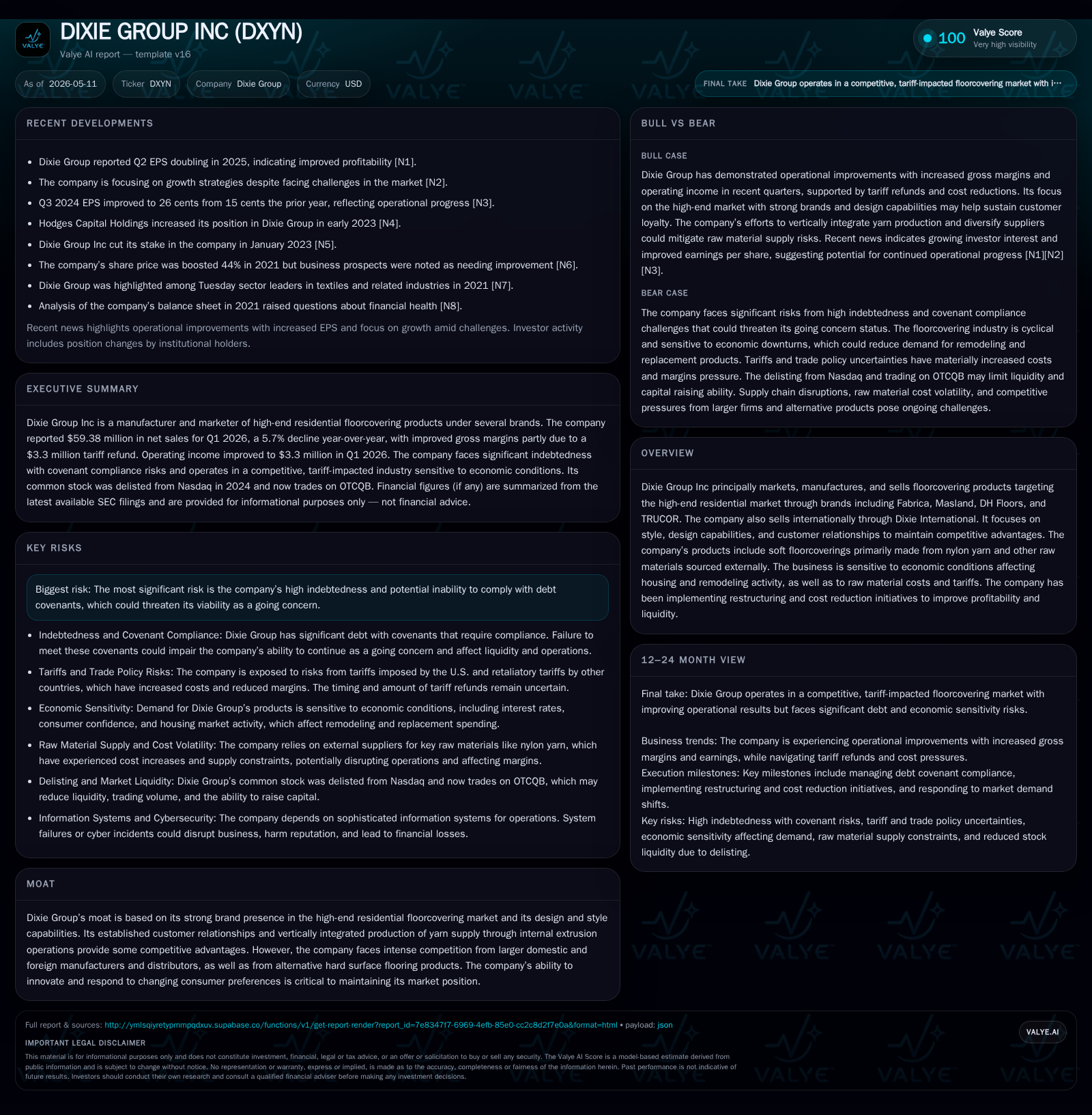

Dixie Group Grapples with Tariff Uncertainties and High Debt Amid Soft Housing Demand

Dixie Group’s Q1 2026 reveals tariff refund windfalls and operating challenges in a subdued floorcovering market pressured by inflation and liquidity constraints.

In Q1 2026, Dixie Group reported a 5.7% decline in net sales driven by weak consumer demand from elevated interest rates and inflationary pressures impacting housing remodel activity. The quarter’s operating income benefitted from a $3.3 million tariff refund linked to a Supreme Court ruling, yet the company continues to face liquidity headwinds with cash usage in operations and significant debt maturities classified as current liabilities. Dixie Group’s high-end flooring business relies on design-led differentiation but remains vulnerable to cyclical residential remodeling trends and exposure to US tariffs. Management’s ongoing restructuring and cost control efforts aim to mitigate margin pressure, but the company’s financial covenant risks and dependence on favorable trade policy outcomes remain key watch points.

Recent Operating Update

Dixie Group Inc's first quarter of fiscal year 2026 demonstrated mixed signals during a challenging macroeconomic backdrop [S2]. Net sales from continuing operations declined 5.7% year-over-year to about $59.4 million, primarily impacted by soft consumer demand influenced by persistent inflationary pressures and elevated interest rates that continue to suppress residential construction and remodeling activity [S2]. The company noted that housing turnover remains subdued due to high mortgage rates, resulting in postponement of durable goods purchases such as flooring.

Within this difficult revenue environment, Dixie Group recorded an operating income of $3.3 million in Q1 2026 compared with nearly breakeven results a year earlier [S8]. This improvement largely stemmed from recognition of a $3.3 million recovery related to IEEPA tariff refunds following a U.S. Supreme Court decision invalidating the government's tariff authority under this act [S2], [S8], [S14]. However, excluding this one-time tariff refund benefit, operating profitability remains constrained during ongoing volume pressure.

Liquidity dynamics highlight ongoing stress: cash used in operations totaled approximately $2.6 million for the quarter [S2]. Increases in accounts receivable—primarily driven by receivables for tariffs—used an additional $7 million of cash in working capital during the period [S2]. Inventory levels rose by about $1.7 million while increases in accounts payable provided some offsetting cash generation (+$4.3 million) [S2]. Capital expenditures remained minimal at $59 thousand [S2]. At quarter-end March 28, 2026, the company held around $2.35 million in cash against total debt approximating $24.6 million [F1]. The company acknowledges liquidity risks but believes in its operational plans and available credit capacity sufficient to meet near-term requirements under existing conditions [S15].

Business Model

Dixie Group operates principally in the design, manufacture, and marketing of soft floorcovering products targeting the premium segment of the residential flooring market [S1], [S2]. Its product offering is primarily nylon-based carpet manufactured using externally sourced raw materials alongside some internally produced yarn via extrusion facilities that provide partial vertical integration benefits [S1]. The company's portfolio comprises well-recognized brands such as Fabrica, Masland, DH Floors, and TRUCOR which cater mainly to high-end residential consumers through specialized sales channels [S1]. Outside North America, Dixie International distributes these brands internationally.

Revenue derives from unit sales of carpet products where price realization depends on product design appeal, fiber quality (nylon being a preferred durable fiber), mix shifting toward higher margin styles, and geographic distribution effectiveness. Customers largely include floor covering retailers servicing renovation markets where homeowners replace or upgrade flooring mostly tied to real estate transactions or remodeling projects.

Margins are sensitive to raw materials — petrochemical derivatives — whose pricing is influenced by oil prices along with tariffs levied on imports affecting cost structure unpredictably [S1], [S24]. Management pursues cost reduction strategies including facility consolidation (notably on the east coast) and productivity enhancement initiatives aimed at maintaining competitiveness despite scale disadvantages relative to larger peers within the industry [S8], [S18].

Industry Structure and Competitive Position

The U.S. residential floorcovering industry is fragmented yet dominated by several large manufacturers offering an array of carpet types alongside hard surface flooring alternatives like laminate or luxury vinyl tile which encroach upon carpet usage especially in mid-tier segments (analysis). Dixie Group's focus on the upper-end segment differentiates it through style leadership, design collaboration capabilities, and brand prestige which act as competitive moats. Furthermore, internal yarn extrusion confers some cost advantages although it does not entirely insulate raw material exposure.

Competition arises from large domestic firms with scale advantages enabling more efficient purchasing power on inputs and broader distribution reach plus foreign manufacturers leveraging lower labor costs (analysis). Additionally, alternative hard surface products growing in consumer popularity pose substitution risks combined with macroeconomic sensitivities linked closely to housing activity cycles.

Growth Drivers

Growth prospects for Dixie hinge structurally upon housing market dynamics—specifically new home construction rates plus turnover-driven remodeling activity that fuels demand replacement cycles for premium carpeting [S2]. The aging housing stock coupled with slower inventory turnover creates latent demand which could accelerate if mortgage rates moderate leading consumers back into remodeling projects (analysis).

Design innovation remains critical; differentiation through updated patterns, textures, sustainable fiber content responsiveness elevates product appeal versus commoditized carpet options (analysis). Geographic expansion internationally via Dixie International offers incremental opportunity leveraging brand recognition outside core domestic markets but scale remains modest.

Operationally, continued execution of restructuring measures aims at improving margins by consolidating manufacturing overheads plus optimizing sourcing models amid ongoing tariff instability which management actively monitors seeking mitigation strategies such as supplier renegotiations or potential price adjustments [S2], [S24].

Risks and Watchpoints

A paramount risk entails Dixie’s elevated indebtedness posing constraints on liquidity with significant portions of debt currently classified as short-term due to restrictive covenants including subjective acceleration clauses that could be triggered if business deteriorates further or financial ratios weaken [F1], [S24]. Non-compliance could precipitate acceleration events threatening survival.

Macroeconomic headwinds linked to inflationary pressures elevate input costs especially energy-related raw materials limiting margin expansion potential alongside cautious consumer discretionary spending depressing volumes nationally across housing-related sectors including flooring.

Tariff exposure creates both direct cost volatility risks due to unpredictable tax implementations plus indirect adverse impacts from retaliatory trade actions abroad potentially complicating Dixie’s international distribution or supplier relationships [S24]. While recent IEEPA tariff refunds provide some relief temporarily there is no certainty future tariffs may not be reintroduced or replaced increasing operational complexity.

Legal contingencies regarding environmental regulations and product liability are perennial risks given industry exposure though covered by insurance policies whose sufficiency cannot always be assured per regulatory scrutiny reports cited previously (analysis).

Market competition from larger peers possessing scale advantages combined with alternate flooring gaining market share introduces continual pricing and volume pressure requiring sustained innovation investment.

What To Watch Next

Key near-term execution markers include monitoring quarterly sales trends correlated against macroeconomic shifts particularly mortgage rate movements signaling potential pickup in remodeling spend driving core demand.

Development around U.S. trade policies concerning tariffs claims processes remain highly relevant given their outsized impact on profit margins; timing and amounts realized will materially influence future earnings visibility.

Operational efficiencies from completed east coast manufacturing consolidation phases along with any further restructuring announcements will offer insight into management’s ability to sustainably reduce fixed costs thus preserving cash flows.

Management issued no formal guidance updates but regularly revises forecasts underlying their going concern assessments meaning any changes therein warrant close attention [S15].

Financial Profile Summary

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Cash & equivalents | $2.35mm | |

| 2026-03-28 | ||

| Total debt | $24.6mm | |

| 2026-03-28 | ||

| Net debt | $22.3mm | |

| 2026-03-28 | ||

| Current assets | $106.5mm | |

| 2026-03-28 | ||

| Current liabilities | $108.3mm | |

| 2026-03-28 | ||

| Current ratio | 0.98x | |

| 2026-03-28 |

Source: SEC companyfacts cache [F1].

While the company holds sizable current assets primarily reflecting receivables (including tariff-related), these are nearly matched by current liabilities indicating tight liquidity buffers and reliance on working capital management efficiency going forward [F1]. Interest expense increased due to floating rate debt amidst rising U.S. rates compounding financial expenses constraining net income generation capacity despite operational improvements reported for early 2026 quarters compared vs prior year periods.[S8]

This analysis synthesizes the most recent SEC filings up through May 11th 2026 combined with established industry context for Dixie Group Inc without providing investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments