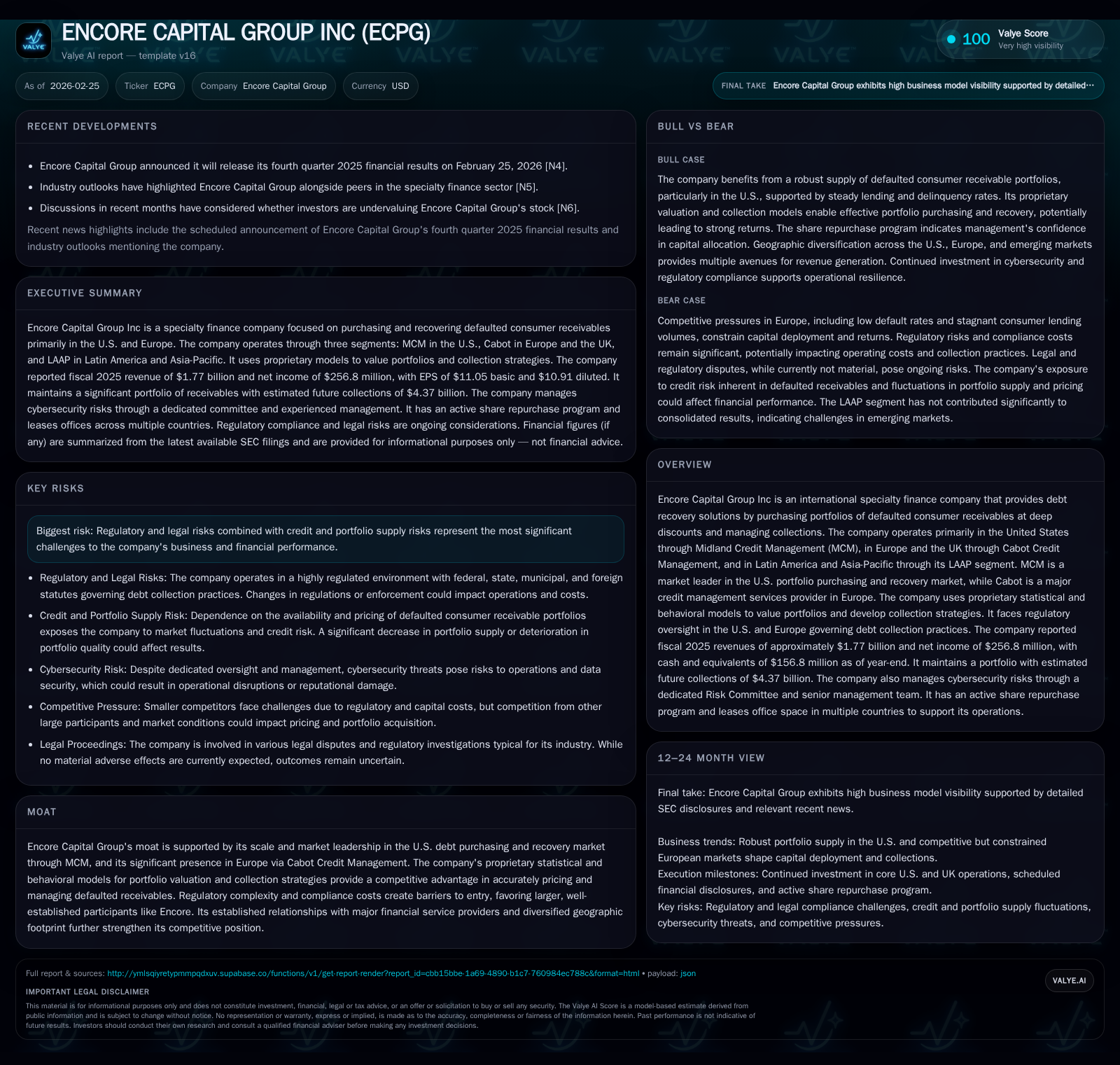

Encore Capital Group’s Turnaround: Accelerated Growth and Strengthened Market Foothold

Encore Capital reversed prior losses in fiscal 2025 through robust portfolio acquisition, operational improvements, and disciplined capital deployment.

After consecutive years of net losses, Encore Capital Group Inc achieved significant financial recovery in fiscal 2025, posting a 34.4% revenue increase to $1.77 billion and a nearly threefold surge in operating income to $627 million [F1]. This turnaround was driven chiefly by expanded portfolio purchases—especially via its Midland Credit Management (MCM) segment in the U.S.—and improved collections efficacy leveraging proprietary valuation models [S11][N4]. Despite regulatory complexities and legal contingencies, Encore bolstered financial flexibility through capital market issuances and accelerated share repurchases totaling $89.5 million in 2025 [S6][F1]. Continued oversight of portfolio supply dynamics, regulatory compliance, and litigation risks will be critical to sustaining growth momentum.

Rebounding from Volatility: Fiscal 2025 Financial Performance Overview

Encore Capital Group demonstrated a decisive recovery in fiscal year 2025 after two years marked by weak profitability and losses. The company’s total revenues jumped by approximately 34.4% from about $1.32 billion in 2024 to nearly $1.77 billion in 2025 [F1], signaling a robust expansion in debt portfolio purchasing and servicing activity.

Operating income surged by an outstanding 298.3%, climbing from roughly $157 million to $627 million over the same period [F1]. This remarkable rebound reflects not only volume growth but enhanced operational leverage as collection efficiencies improved under the stewardship of their Midland Credit Management (MCM) unit.

Net income swung dramatically from a negative $139 million to a positive $257 million, representing a near-tripling effect that confirms stabilization and improved earnings quality [F1]. Meanwhile, operating cash flow remained relatively steady at around $153 million despite the volatility in earnings, reflecting consistent underlying cash generation capacity necessary to fund aggressive portfolio acquisition [F1]. Capital expenditures declined modestly by roughly 9.4% year-over-year to $26.3 million, indicating controlled investment into property and systems aligned with business needs [F1].

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 1769 | 257 | 153 | 627 | +34.4% | +284.4% |

| 2024 | 1316 | -139 | 156 | 157 | +7.7% | +32.6% |

| 2023 | 1223 | -206 | 153 | 17 | -12.6% | -206.1% |

| 2022 | 1398 | 195 | 211 | 462 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | FCF ($mm) |

|---|---|---|

| 2025 | 90 | 127 |

| 2024 | 0 | 127 |

| 2023 | 0 | 128 |

| 2022 | 87 | 173 |

Source: SEC companyfacts cache [F1].

The quantitative improvement encapsulates the company's successful turnaround strategy centered on expanding purchasing scale while controlling collection costs.

What Fueled Encore’s Surging Revenue and Operating Income?

The engine behind Encore's resurgence lies primarily in its enhanced portfolio purchasing approach combined with sophisticated collections analytics. The company leverages proprietary statistical and behavioral models that provide superior predictive insight into the valuation of defaulted consumer debt portfolios, enabling more accurate pricing as well as optimized collection strategies [N4][S11].

Midland Credit Management (MCM), Encore’s flagship U.S.-based segment, increased purchasing activity substantially during fiscal 2025 through forward flow purchase agreements—multi-year commitments to acquire specified volumes of defaulted receivables at pre-negotiated prices that enable operational predictability and scale efficiencies [S11][S13]. These agreements minimize uncertainty around originations pacing, directly boosting revenue visibility.

Enhanced collection performance also contributed materially to operating margin expansion; improvements stem from process automation combined with data-driven segmentation of delinquent consumers that reduces cost to collect while boosting gross cash flows recovered from accounts [N4][S11]. These advantages exemplify how Encore solidifies its moat utilizing data science capabilities which smaller competitors may struggle to replicate.

Geographic and Segment Contributions to Growth

Encore operates through one reportable segment focused on debt purchasing and recovery but geographically spans multiple regions including the United States (via MCM), Europe/United Kingdom (via Cabot Credit Management), and other international markets [S11][S12]. Despite steady activity across all regions, the bulk of revenue growth is attributable to the U.S., where MCM maintains market leadership.

In fiscal 2025, the U.S. segment generated approximately $1.27 billion in revenues versus about $992 million in the prior year, representing robust growth driven by expanded portfolio purchases backed by securitized financing vehicles supporting MCM's asset base on balance sheet [$770 million book value as collateral under the U.S. facility] [S7][S11].

European operations under Cabot generated revenues near $495 million—a meaningful contribution albeit reflecting constrained growth amid price competition and regulatory headwinds especially across UK, France, and Spain markets where default rates remain lower than historical averages [S12][S13]. Across Europe, forward flow arrangements have gained traction but consumer lending volume stagnation has capped expansion prospects.

Other international markets remain smaller but represent strategic areas for growth.

Key native terms relevant here include 'securitized financing vehicle' for debt facilities backing receivables portfolios, 'book value of receivables' representing loan asset carrying amounts underpinning borrowings, and 'forward flow purchase agreements' denoting committed receivable acquisitions which jointly influence capital deployment velocity.

Regulatory Landscape: Compliance as Both Headwind and Moat

Encore faces significant regulatory scrutiny stemming from its collection practices governed by a complex web of federal, state, municipal statutes within the United States as well as analogous foreign regulations impacting Cabot operations [S5][S27]. Ongoing investigations led by certain U.S. state Attorneys General relating to historic practices impose both direct compliance costs—including potential penalties—and reputational risks that can affect business dynamics.

However, this intricate regulatory environment also erects barriers deterring entry by smaller or less compliant competitors who face disproportionate expense burdens managing evolving statutes —thus reinforcing Encore's position as an incumbent large-scale operator able to invest significantly into governance infrastructure such as cybersecurity oversight managed through the Risk Committee reporting directly to the Board according to disclosures [S1]. Such risk management sophistication enhances durability amidst regulatory complexity.

Furthermore, litigation contingencies exist but reported reserves are not material currently owing to conservative accounting principles that require recognition only upon probable loss estimations supported by measurable data—underscoring prudent risk conservatism embraced by management [S5][S27].

Capital Structure Evolution and Its Impact on Financial Flexibility

Throughout fiscal year 2025, Encore actively optimized its capital framework by amending existing credit arrangements for greater capacity and extending maturities matching business needs amid varying interest rate environments.

Notably, the company increased its Global Senior Secured Revolving Credit Facility by $190 million bringing total commitments up to approximately $1.485 billion with maturity pushed back from September 2028 to September 2029—with certain tranches retaining earlier maturities—providing expanded liquidity for portfolio acquisitions [S4][S7]. The facility bears floating interest tied primarily to Term SOFR plus margins near ~2.25%, inclusive of credit adjustment spreads reflecting creditworthiness.

Alongside revolving credit enhancements, Encore issued new senior secured notes totaling $500 million due April 2031 at coupon of approximately 6.625%, using proceeds partly to repay revolving credit draws enhancing financial flexibility while locking long-term fixed rate funding at favorable levels compared with prior debt tranches maturing sooner or at higher coupons [S15][S18].

Restrictions embedded within facilities incorporate leverage thresholds such as Loan-To-Value (LTV) limits—the Global Senior Facility restricts LTV ratio below .75 if utilization exceeds 20%, alongside Fixed Charge Coverage Ratio covenant set at minimum of twice annual fixed charges—measures intended to maintain prudent leverage controls consistent with rating agency expectations for specialty finance operators investing heavily in nonperforming consumer loans [S4].

These structures collectively support ongoing forward flow agreement commitments critical for sustained portfolio acquisitions while preserving covenant headroom under prevailing market conditions.

Capital Allocation Priorities: From Share Repurchases to Debt Management

Capital allocation reflects balanced emphasis on returning value while maintaining investment capacity for growth initiatives.

After authorization expansions increasing share repurchase program size cumulatively up to $600 million since May 2021 augmentation actions, Encore recommenced buybacks aggressively starting late calendar year 2025 accelerating repurchase volumes notably absent during previous years when losses constrained distributions [S6][F1]. In FY25 alone approximately $89.5 million was utilized acquiring over two million shares at average prices rising throughout quarters consistent with stock price recovery trends recorded during that time frame; this reflects management's confidence supported by positive free cash flow generation after capex deductions amounting roughly $127 million annually (operating cash flow minus capex) illustrating prudent liquidity management alongside shareholder returns ambitions.

Conversely, Encore has historically not declared dividends on common stock citing board discretion in light of debt covenants limiting dividend capacity plus strategic reinvestment priorities tied tightly to capital-intensive receivables purchasing business model requirements restricting distributable free cash beyond share retirements presently stated in filings [S6][F1].

Debt management saw convertible note extinguishments—a key milestone included settlement of their maturing $100 million convertible notes in October “cash conversion” funded from revolver borrowings with minimal earnings impact apart from conversion cost amortizations demonstrating proactive liability maturation planning enhancing balance sheet clarity ahead of longer-dated senior notes issuance [S9][S15].

Looking Ahead: Indicators to Monitor for Enduring Growth Momentum

While explicit forward guidance is absent from public disclosures, several indicators warrant close monitoring going forward:

- The cadence and volume embedded within forward flow purchase agreements serves as a near-term barometer of portfolio origination pipeline strength influencing revenue trajectories given sizable portion of buying committed under multi-month contracts constraining volatility risk exposure [N4][S13].

- Collection cost efficiency ratios improve margins directly; advancements via automation or model refinements could uplift yields on acquired assets amid competitive pricing pressure particularly outside U.S. markets where lower default levels limit upside capital deployment opportunity notably across Europe [N4][S13].

- Evolving regulatory regimes or settlements pertaining to existing investigations remain variable affecting expense profiles or operating constraints especially at MCM level since legislative bodies continue revising debt collection practice frameworks dynamically requiring agile adaptations maintaining compliance without eroding economics excessively [S5][N4].

- Geographical expansion aspirations primarily involve deepening presence within established European jurisdictions like France or Spain where sales volumes show resilience supported occasionally by macroeconomic factors influencing non-performing loan industry cycle timing though overall consumer lending stagnation tempers upside visibility sufficiently cautioning prudent capital commitment pacing [N4][S27].

Risks Remain: Litigation Exposure and Portfolio Supply Dynamics

Despite encouraging recent financial improvement trends considerable risks persist impacting future performance consistency:

- Outstanding litigations including state Attorney General inquiries related historically embedded collection tactics expose Encore potentially costly settlements or injunctive mandates altering operational flexibility; however current provisions remain immaterial reflecting conservative accounting treatment aligned with GAAP loss contingency standards whereby only probable and estimable losses are accrued limiting unexpected earnings shocks but warrant vigilance on case developments given duration unpredictability typical within this sector's regulatory environment [S5][F1][S27].

- Portfolio supply concentration represents another risk vector given that despite sizeable available opportunities particularly domestically enabled via forward flow constructs actual volumes fluctuate with credit originators’ willingness influenced by economic cycles or underwriting shifts; thus any abrupt contraction or repricing spikes could challenge growth continuity although Encore’s diverse geographic footprint mitigates region-specific downturn risks somewhat offering structural resilience relative to pure-play single market counterparts[S13][N4].

- Operational risks such as cybersecurity threats managed under Board Risk Committee oversight add further layers needing continuous focus emphasizing integrated enterprise risk governance mechanisms requisite for trust retention among clients sensitive about data stewardship within financial services delivered extensively via digital channels today [S1].

In summary, Encore Capital Group’s turning point captured by restored profitability stems from disciplined expansion backed by proprietary analytics bolstered collections efficiencies plus savvy capital structure enhancements fueling acquisition expansion financed prudently against a backdrop of complex regulatory environments shaping competitive moats favoring scale incumbents yet necessitating ongoing vigilance against legal risks inherent in specialty finance portfolios.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments