Ellington Financial's Diversified Mortgage Strategy and Cash Flow Volatility Challenge Return Stability

Ellington Financial leverages broad credit expertise in mortgage assets while contending with fluctuating cash flows and external management dependencies.

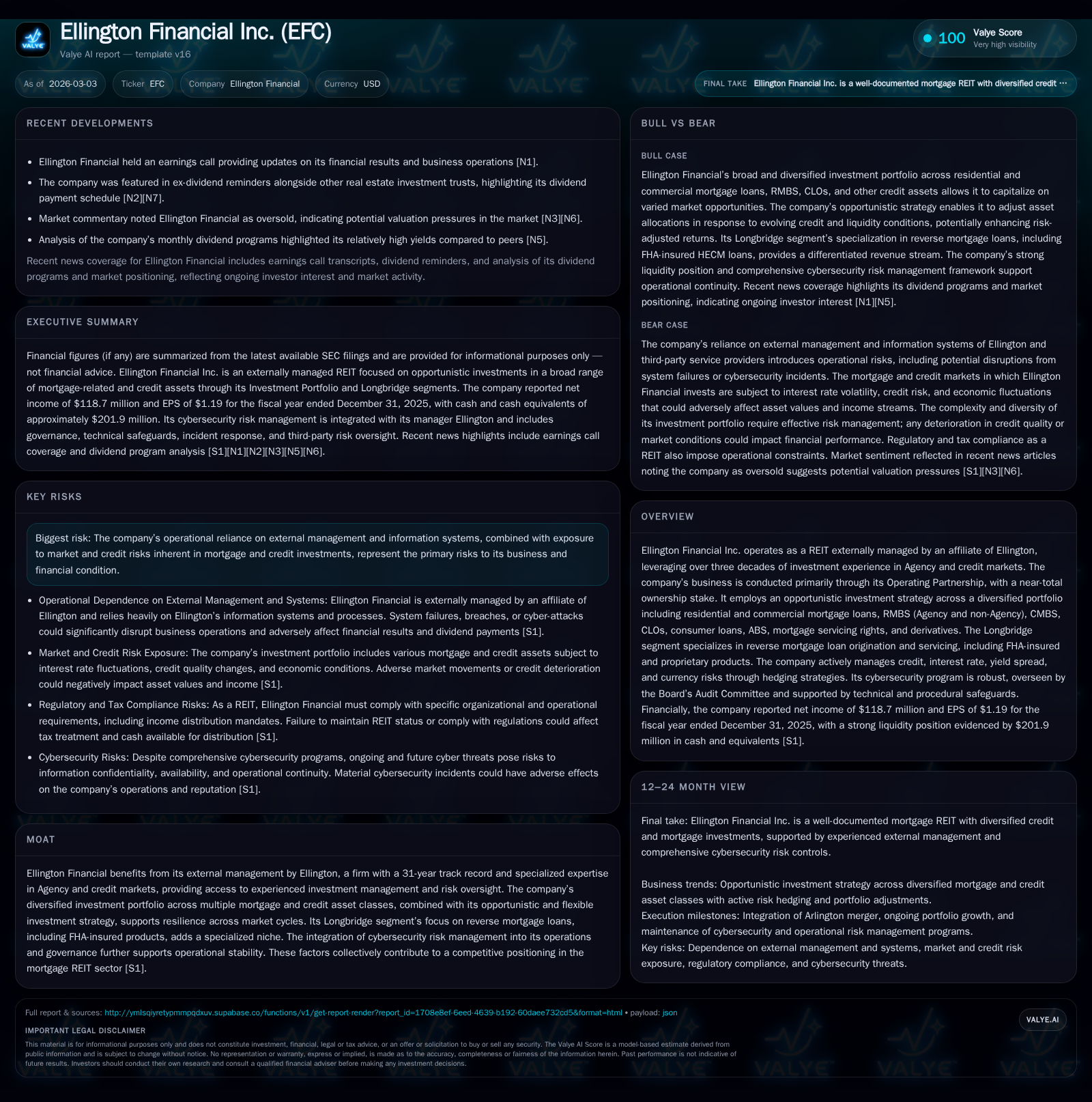

Ellington Financial Inc. (EFC) operates as an externally managed REIT with a history of opportunistic investments across diversified residential and commercial mortgage-related assets, including Agency and non-Agency RMBS, CLOs, consumer loans, and reverse mortgages. Its past growth reflects strong net income gains and equity expansion, albeit with significant operating cash flow swings recently. Future growth hinges on dynamic asset allocation, credit market conditions, and successful integration of Longbridge’s reverse mortgage niche. Watching operating cash flow trends and capital returns will be critical to assess sustainability given a consistent dividend policy amid no recent buybacks.

Company Overview

Ellington Financial Inc., traded under ticker EFC, is an externally managed real estate investment trust (REIT) specializing in mortgage-related assets across residential and commercial sectors. The company employs an opportunistic investment approach without restrictions related to ratings or position within capital structures. Managed by an affiliate of Ellington — a firm with over three decades of experience in Agency and credit markets — Ellington Financial leverages this expertise through its Operating Partnership structure where it holds a roughly 99.1% ownership stake [S1].

Its portfolio spans multiple asset classes: Agency RMBS (including specified pools), non-Agency RMBS including prime jumbo and non-QM loans, commercial mortgage-backed securities (CMBS), collateralized loan obligations (CLOs), consumer whole loans and ABS, mortgage servicing rights (MSRs), derivatives including To-Be-Announced (TBA) securities and credit default swaps (CDS), as well as strategic equity investments in loan originators [S1][S6][S9][S12]. The firm's Longbridge segment specializes in reverse mortgages—originating FHA-insured Home Equity Conversion Mortgages (HECMs) and proprietary reverse products—with servicing operations encompassing approximately 500 employees [S1][S18].

Historical Performance & Growth Drivers

From a financial perspective, Ellington Financial has exhibited notable income growth alongside increased balance sheet size over the recent years tracked from SEC filings through end-2025 [F1]. Net income nearly doubled between 2023 ($60.9 million) and 2025 ($118.7 million), boosted by higher yields on credit assets amid tightening spreads and stronger credit performance [F1][S4]. Equity also rose consistently from $1.2 billion in 2022 to $1.83 billion at the end of 2025.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | Net YoY |

|---|---|---|---|

| 2025 | 119 | -925 | +0.8% |

| 2024 | 118 | -431 | +93.5% |

| 2023 | 61 | -242 | +171.4% |

| 2022 | -85 | 43 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | ROE% |

|---|---|---|---|

| 2025 | 184 | 0 | 6.5 |

| 2024 | 164 | 1 | 7.5 |

| 2023 | 149 | 12 | 4.0 |

| 2022 | 123 | 2 | -7.1 |

Source: SEC companyfacts cache [F1].

Table: Key financial metrics for Ellington Financial Inc., fiscal years ended December [F1]

Operating cash flow has been negative for three years running through fiscal year-end 2025, plunging further in the latest year to nearly -$925 million from roughly -$430 million in the prior year [F1]. This points to volatility typical of leveraged mortgage investment platforms where mark-to-market impacts on asset valuations, securitization activity, or working capital timing can significantly influence cash flows.

Dividend payments have grown steadily despite challenging cash flow dynamics—$183 million paid out in dividends during fiscal year-end 2025 vs $123 million in 2022—with no share repurchases since minimal buys in preceding years [F1][S10]. This implies a prioritization of stable distributions aligned with REIT qualification requirements over capital return via buybacks.

Portfolio Composition & Investment Focus

The company's targeted lending asset classes span:

- Agency RMBS: Whole pools and specified pools guaranteed by federal agencies or GSEs such as Fannie Mae and Freddie Mac; includes fixed- and adjustable-rate mortgages plus reverse mortgages securitized into HECM-backed MBS.

- Non-Agency Credit Portfolio: Includes non-QM residential loans which encompass borrowers outside Qualified Mortgage standards but not necessarily subprime; fix-and-flip loans; residential NPLs/RPLs; HELOCs; consumer unsecured loans; ABS backed by consumer loans or SBA loans.

- Commercial Real Estate Debt: First-lien seasoned bridge loans on transitional properties with maturities generally under two years [S6][S14][S15].

- CLOs & Corporate Debt: Positions in CRE CLO notes along with corporate loan tranches.

- Mortgage Servicing Rights: Investments related to forward MSRs following the December 2023 merger with Arlington Asset Investment Corp., allowing access to servicing revenue streams [S1][S25].

- Derivatives: Mortgage-related derivatives used for hedging interest rate risk or yield spread risk include TBA contracts, CDS referencing MBS or CMBX indexes.

This multi-faceted portfolio approach enables pivoting among various risk-return profiles depending upon market pricing of credit risk or liquidity conditions [S1][S6]. For example, Non-QM loans typically offer higher yields relative to Agency RMBS but require more active credit monitoring.

Recent Trends & Market Environment Considerations

Market data as of early 2026 indicate Federal Reserve interest rate shifts—with Fed easing beginning late 2024 followed by slower rate cuts projected for all of 2026—which are key drivers influencing mortgage loan yields versus funding costs impacting net interest margins for Ellington's portfolios [S17]. Concurrently, geopolitical trade uncertainties including tariff policies contributed to volatility impacting capital markets during parts of the trailing period [S17].

Delinquencies in both residential and commercial lending saw uptick year-over-year but improved slightly by Q4 2025; however realized losses remained contained so far suggesting resilient borrower performance [S4]. Ongoing focus remains on working down non-performing assets within legacy loan positions particularly within residential NPL/RPL pools sourced from motivated sellers at attractive prices [S14][S15].

Ellington's extensive use of derivative instruments for interest rate swaps mitigates repo borrowing cost fluctuations—a vital aspect given funding is largely secured through repurchase agreements at variable market rates [S21]. The firm's hedging strategies also address credit spread risk exposures via CDS on corporate bonds or collateralized securities alongside selective foreign currency hedging for Euro-denominated holdings.[S16]

Capital Allocation & Returns

The company did not execute any share repurchases in fiscal year 2025 after relatively modest buybacks totaling $685 thousand the prior year and $12 million in FY23 [F1]. Dividend distributions have increased steadily from approximately $123 million paid in FY22 to $183 million paid in FY25 reflecting commitment to steady investor payouts consistent with REIT tax regulations requiring distribution of at least 90% taxable earnings annually [F1][S10].

Return on equity is presently moderate at about 6.5% demonstrating that net income growth has broadly tracked equity expansion resulting from earnings retention primarily reinvested into the asset base rather than elevated leverage growth given overall balance sheet size near $1.83 billion equity at end-2025 [F1]. This ROE level is acceptable within structured credit investing where incremental gains arise from specialized underwriting rather than high operating leverage.

Operational Risk & Cybersecurity Governance

A salient non-financial factor is Ellington Financial’s dependence on their external manager Ellington’s information technology systems as well as those of third-party vendors such as mortgage servicers within their portfolio firms [S24][S18]. These dependencies underscore risks related to potential system failures or cyber-attacks which could materially disrupt operations impacting results or dividend capacity.

To mitigate these risks, Ellington implements rigorous cybersecurity governance overseen by its Board Audit Committee receiving comprehensive updates regularly covering threat environments, vulnerability assessments, incident responses, technological upgrades, employee training programs, disaster recovery plans together with specialized teams led by experienced CTO and infrastructure leaders focused solely on security measures across enterprise operations [S24]. Moreover Longbridge segment applies additional bespoke operational risk oversight tailored for the mortgage banking sector [S18].

Forward-Looking Considerations & Milestones to Watch

Ellington does not provide explicit public guidance for revenue or earnings forecasts but signals intent to continuously adjust asset allocations responsive to shifting market conditions while maintaining REIT status compliance [N1][S1][S12]. Key performance indicators will involve tracking:

- Growth or contraction trajectory of adjusted long credit portfolio beyond the reported roughly +24% increase into subsequent periods,

- Trends in delinquency rates balanced against credit loss reserves,

- Interest rate environment evolution affecting net interest margin especially relating to repo cost variations versus asset yields,

- Integration success of anticipated acquisitions like residential mortgage servicers improving operational capabilities,

- Regulatory developments that might impact servicing practices or capital treatment,

- Dividend payout sustainability vis-à-vis volatile operating cash flow patterns,

- Any material shifts or expansions within the Longbridge reverse mortgage segment that may alter risk/return profile.

Summary & Conclusion

Ellington Financial Inc.’s business model emphasizes a broad-based yet selective exposure across diverse mortgage-related assets leveraging deep external management expertise rooted in agency-backed securities alongside higher margin non-QM loans and commercial real estate debt.

Historical performance evidences strong net income growth supported by increasing equity base although overshadowed recently by negative operating cash flows revealing underlying earnings quality concerns typical within complex structured finance entities reliant on mark-to-market fluctuations.

Capital allocation favors dividends over share repurchases consistent with REIT norms while sophisticated risk management including derivatives hedging buttress returns against volatile markets.

Operational risks center primarily around external management reliance especially IT/cybersecurity vulnerabilities but these are addressed proactively through formal governance frameworks supported by veteran technical staff expertise.

Investor focus should be directed towards monitoring evolving portfolio mix adjustments amid uncertain interest rate trends plus ongoing credit quality metrics alongside any regulatory headwinds impacting structured product markets where Ellington competes.

Disclaimer: This document is an analysis based on publicly available company filings and news sources as cited; it does not constitute investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments