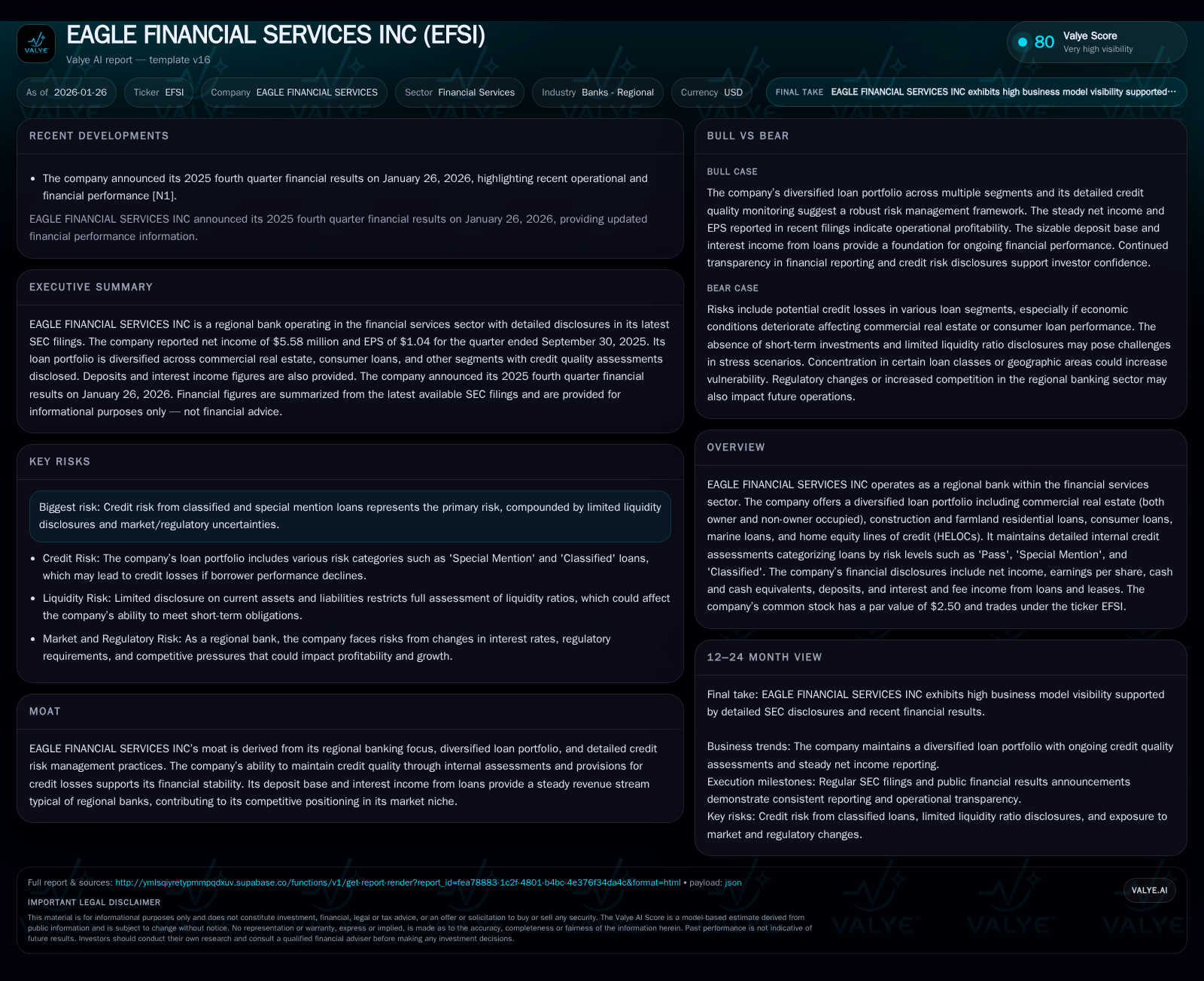

Eagle Financial Services Releases Q4 2025 Results, Confirming Steady Regional Bank Performance

Eagle Financial Services reported its fourth quarter 2025 financial results with detailed disclosures reinforcing its credit risk monitoring and stable net income.

Eagle Financial Services reported Q4 2025 results highlighting steady net income and ongoing credit risk assessments; the release signals continued transparency but offers limited new guidance, with credit risk and liquidity remaining key areas to monitor.

Eagle Financial Services reported its fourth quarter 2025 financial results with detailed disclosures reinforcing its credit risk monitoring and stable net income.

Valye News Insights

Eagle Financial Services disclosed its fourth quarter 2025 financial performance, reinforcing operational transparency for stakeholders. This quarterly update offers visibility into the company’s ongoing credit quality management amidst a diversified loan portfolio, though it lacks specifics on changes in guidance or liquidity metrics, which remain potential gating factors for deeper analysis.

From a Valye AI perspective, the industry-wide challenge remains balancing credit risk with regional economic conditions, especially in commercial real estate and consumer lending.

One plausible scenario is continued steady income if credit quality holds, but material credit deterioration could recalibrate risk profiles.

The materiality gate centers on upcoming quarterly metrics detailing loan performance changes, provision adjustments, and deposit trends. In practical terms, that usually means milestones like Roadmap Proof Points and What Changes Minds.

Key numbers

- January 26, 2026 – Date of Q4 2025 financial results announcement

- Q3 2025 net income reported as $5.58 million

- Q3 2025 earnings per share of $1.04

- $1.58 billion in deposits reported in latest filings

- $81.8 million in interest and fee income from loans and leases

What changed

- Announced fourth quarter 2025 financial results

Bottom line: The quarterly report confirms Eagle Financial Services’ steady financial performance and transparency but leaves liquidity and credit risk evolution as pivotal factors for future operational stability.

Key points

- Eagle Financial Services announced its Q4 2025 results on January 26, 2026.

- The company maintains a diversified loan portfolio with detailed credit classifications.

- Net income and EPS figures indicate operational profitability in the prior quarter.

- Deposits remain sizable, supporting funding stability.

- No new guidance or liquidity ratios were disclosed in the release.

- Credit risk remains the main area of concern due to classified and special mention loans.

Industry Analysis

- The report aligns with common patterns in regional banking where steady credit risk monitoring and deposit stability underpin financial health.

- Continued diversification across loan types is typical to mitigate concentration risk in regional banks.

- Credit risk disclosure granularity is an industry best practice aiding transparency, especially amid economic uncertainties.

- A plausible scenario is stable earnings continuity if credit quality remains stable, but regional economic headwinds could pose downside risk.

- Lack of updated liquidity information reflects a recurrent opacity challenge among smaller regional banks.

Valye Beyond the Headlines

- The update provides visibility on recent financial outcomes but lacks new guidance or liquidity data, limiting forward-looking assessment.

- Materiality hinges on future quarters’ credit loss provisions and loan performance indicating risk trajectory.

- Stable deposit levels are positive for funding but upcoming stress tests or regulatory changes could shift outlook.

- Investors would prioritize monitoring any changes in the classified loan categories and allowance for credit losses.

- Upcoming SEC filings and earnings calls represent critical milestones to reassess operational and risk metrics.

Tech Context

- No new technology implementations or innovations were disclosed in this financial results release.

- The bank’s credit risk management appears reliant on internal assessments rather than external tech-driven analytics disclosed.

- Digital banking or fintech integration updates are absent, indicating no immediate tech-driven operational shifts.

- Data transparency and reporting remain traditional, with focus on financial metrics rather than technology-enabled capabilities.

Business Trends

- The quarterly results reinforce Eagle Financial Services’ core regional banking model with a diversified loan base and deposit funding.

- Internal credit categorizations signal a proactive approach to risk monitoring but the impact of special mention and classified loans remains the largest uncertainty.

- Stable net income and EPS reflect operational consistency but are vulnerable to regional economic shifts affecting borrower performance.

- The absence of updated liquidity metrics could reflect either stable funding or limited disclosure willingness, both important to watch.

- Transparency in periodic SEC filings supports investor confidence but more frequent updates on loan portfolio health would deepen insight.

- The business model depends heavily on interest income generation and deposit retention in a competitive regional market.

- Potential external pressures include interest rate volatility, regulatory changes, and local economic conditions shaping credit risk and profitability.

- Future financial results will need to demonstrate effective management of emerging credit risks to maintain financial stability.

Valye context (from report)

- Eagle Financial Services operates as a regional bank with a diversified loan portfolio including commercial real estate, consumer, and construction loans.

- Credit risk is managed through detailed internal assessments categorizing loans into 'Pass', 'Special Mention', and 'Classified'.

- Reported net income and EPS indicate stable profitability as of the latest filings.

- Deposits exceed $1.5 billion, underpinning funding stability.

- Interest and fee income from loans constitutes a major revenue source.

- Risks include credit risk from classified loans, limited liquidity disclosures, and regulatory pressures.

- Financial disclosures are consistent with regulatory filings providing transparency to investors.

- The company’s moat includes regional focus, diversified portfolio, and credit risk management.

- Recent announcement confirms ongoing commitment to transparent quarterly reporting.

Risks / what to watch

- Credit risk exposure in 'Special Mention' and 'Classified' loan categories may lead to future losses if borrower performance deteriorates.

- Limited disclosure on liquidity ratios restricts assessment of short-term financial flexibility.

- Regional economic downturns, especially in commercial real estate, could increase credit stress.

- Regulatory changes or heightened compliance costs could pressure profitability.

- Competitive pressures in the regional banking sector might affect deposit growth and loan origination.

- Interest rate volatility could impact net interest margins and loan demand.

- Concentration in certain loan types or geographic areas may increase vulnerability.

- Absence of new guidance or strategic updates leaves forward outlook uncertain.

- Monitoring allowance for credit losses and provision trends is critical for risk evaluation.

News Context

- Eagle Financial Services announced its 2025 fourth quarter financial results on January 26, 2026.

- Financial summary data includes net income of $5.58 million and EPS of $1.04 from the prior quarter ended September 30, 2025.

- Deposits were reported at approximately $1.58 billion with interest and fee income from loans around $81.8 million.

- The company’s loan portfolio is diversified across commercial real estate, consumer loans, construction, farmland residential loans, marine loans, and HELOCs.

- Credit quality is tracked internally with categories 'Pass', 'Special Mention', and 'Classified'.

- No new liquidity metrics or forward guidance was provided in the announcement.

Sources

This article is general in nature and often relies heavily on company press releases and other third-party public sources, which may be promotional, incomplete, or occasionally inaccurate. It also incorporates AI-generated analysis, assumptions, scenarios, and broader public background context to help place the news in a wider industry narrative. As a result, it may contain errors or omissions. Always verify important details using primary sources (company filings, official releases, and direct statements). This is not financial advice and is not a recommendation to buy or sell any security.

Disclaimer: Research-only. Not investment advice.

Comments