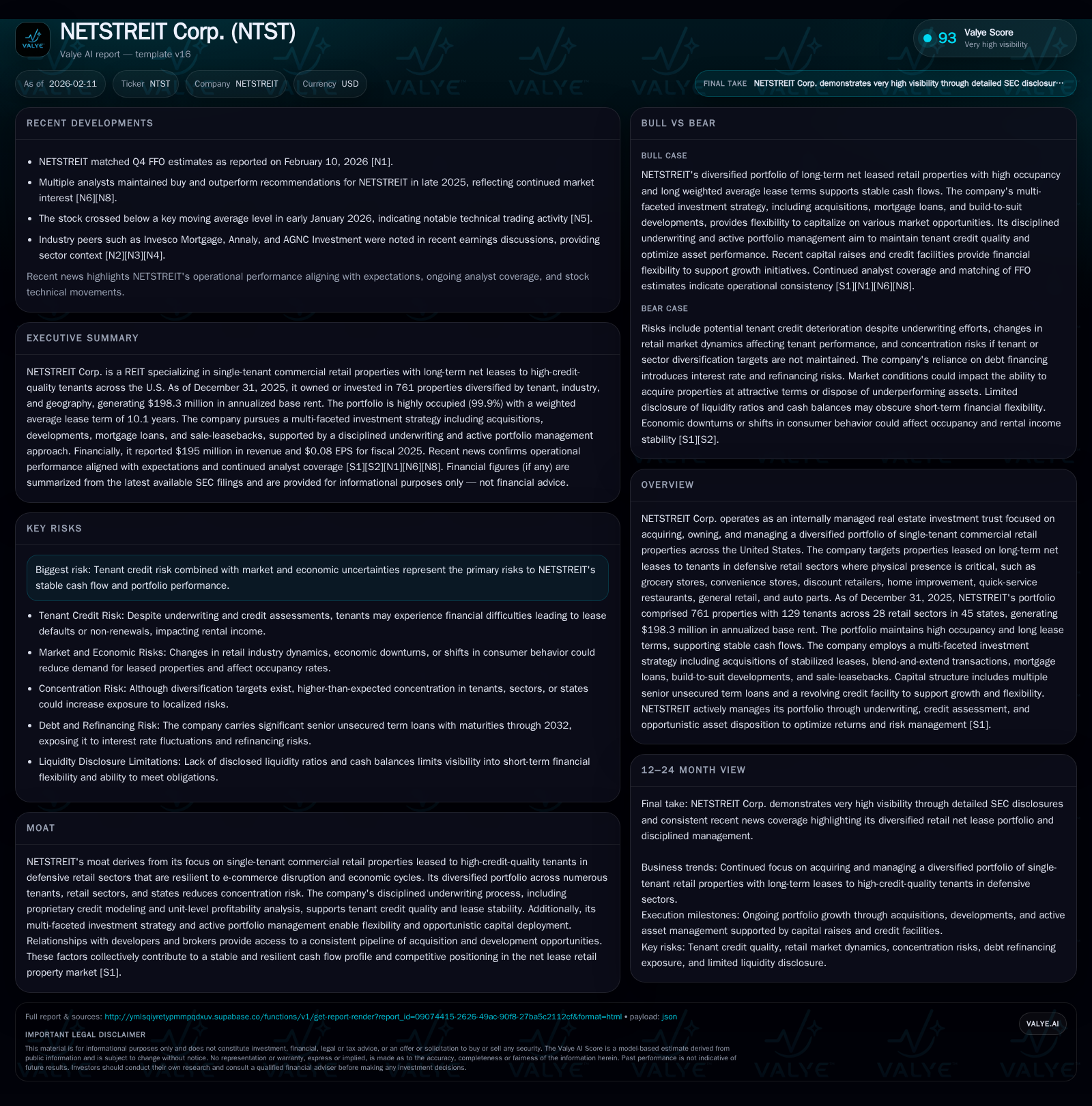

NETSTREIT Corp: Defending Stability Through Diversified Retail Real Estate Holdings

An in-depth look at NETSTREIT’s defensive portfolio strategy, credit quality, and financial resilience amid evolving debt markets and tenant risks in 2026.

NETSTREIT Corp. anchors its strategy on a broad portfolio of necessity-driven retail properties leased to high-credit tenants across 45 states, generating stable cash flows supported by long lease durations. In 2025, the company enhanced its financial flexibility through sizable acquisitions and prudent debt refinancing, benefiting from improved credit ratings that lowered borrowing costs. Key risks remain tenant credit exposure against a backdrop of economic uncertainty, yet disciplined underwriting and a multi-faceted investment approach underpin the company's competitive moat. Recent earnings matched expectations, but technical stock signals hint at caution among investors.

NETSTREIT’s Portfolio: Defense Through Diversification

In the sprawling landscape of U.S. commercial real estate, NETSTREIT Corp. stands as a custodian of necessity — managing an expansive collection of single-tenant retail properties where physical presence is not only preferred but essential. As of December 31, 2025, this portfolio included an impressive 761 properties located in 45 states, diversified across 28 retail sectors that range from grocery stores and convenience outlets to quick-service restaurants and home improvement centers [S1]. This geographic breadth combined with sector diversity creates a sturdy framework against localized economic shocks or shifting consumer preferences.

These defensive retail industries are carefully chosen for tenants whose businesses generate steady foot traffic tied to everyday consumer needs — a factor that lends resilience against the e-commerce tidal wave reshaping much of retail real estate.

The Credit Quality Backbone: How Investment Grade Tenants Anchor Stability

NETSTREIT’s strategic emphasis on tenant quality is evident in its composition of annualized base rent (ABR). Roughly 44% originates from tenants holding formal investment grade credit ratings, while another 14% comes from those with robust investment grade profiles despite lacking official ratings [S1]. This nearly 60% reliance on high-credit-quality lessees provides a substantial moat by lowering the odds of payment disruptions or defaults.

The company’s underwriting rigor extends beyond ratings alone—employing proprietary credit modeling and granular unit-level profitability analyses—that collectively bolster confidence in the tenant cohort's financial stability.

Lease Term Strengths: The Long Horizon of Cash Flow Certainty

One hallmark of NETSTREIT’s portfolio is its weighted average lease term (WALT) standing at 10.1 years [S1]. Such elongated lease durations are uncommon in many real estate subtypes yet central here for locking in predictable revenue streams over a decade or more.

Combined with an occupancy rate north of 99%, this protracted lease horizon offers a meaningful buffer against cyclical downturns. It allows management to plan capital deployment and debt servicing without the immediate pressure often seen in shorter-term leases.

Capital Strategy in 2025: Growth Fueled by Smart Acquisitions and Debt Management

The year 2025 marked an active phase for NETSTREIT’s capital deployment. The acquisition of 140 properties costing approximately $603 million expanded their footprint across 31 states while boosting lease term metrics further—these new assets carried an average WALT nearing fourteen years [S1]. This reflects a deliberate tilt towards high-quality assets ensconced with longer contractual commitments.

Simultaneously, selling off 78 properties crystallized gains totaling $7.7 million on $169 million proceeds, illustrating ongoing portfolio optimization.

Capitalizing on its upgraded investment grade rating, the company secured senior unsecured term loans aggregating $450 million split between maturities in March 2031 and September 2032. Interest margins have been trimmed thanks to this elevated credit profile—margins fell as much as twenty-five basis points on some tranches—and substantial portions of these loans are hedged at fixed rates around mid-4% levels [S1]. These moves collectively reduce financing costs while preserving flexibility for future growth opportunities.

Financial Health Check: Revenue Trends and Profitability Insights

For fiscal year-end December 31, 2025, NETSTREIT reported revenues slightly shy of $195 million [F1], a figure closely aligned with the annualized base rent metrics reflecting stable operational execution over time. Net income stood modestly positive at approximately $618 thousand for the quarter ended September [F1], typical for REITs where fair value adjustments and non-cash items temper accounting profitability.

More meaningful measures for investors often emphasize funds-from-operations (FFO), which better capture recurring cash flow generation critical to sustaining dividends and capital reinvestment—elements reinforced by the company’s maintained near-full occupancy and long lease tenor [S2].

Risks on the Radar: Tenant Credit and Market Dynamics to Watch

Despite a sturdy foundation, notable risks hover over NETSTREIT’s performance prospects. Foremost among these are tenant credit risks intensified amid uncertain macroeconomic conditions that can reverberate through retailers’ ability to maintain rent payments [S1][valye_report_excerpt].

Economic headwinds such as inflationary pressures or regional downturns could especially test single-tenant operators though diversified sectoral exposure tempers concentrated vulnerability. Additionally, shifts in interest rates bear watching since costlier capital might depress acquisition activity or valuation multiples impacting future growth avenues.

Recent Market Reactions: Stock Movement and Earnings Report Highlights

Public market sentiment has remained measured around NTST shares recently. The company met Q4 earnings per share expectations announced early February without surprises [N4], reassuring stakeholders about operational steadiness.

Yet technical indicators have registered some headwinds; notably, NTST slipped below key moving average thresholds earlier in January [N5], signaling investor caution perhaps driven by broader market volatility affecting real estate investment trusts across the board.

Such dynamics illustrate the balancing act facing REITs today — functioning between intrinsic asset resilience versus near-term price fluctuations informed by external capital market sentiment.

Strategic Outlook: Navigating Opportunities and Uncertainties Ahead

Looking forward into early 2026 and beyond, NETSTREIT's success will likely hinge on sustaining its disciplined underwriting standards and leveraging relationships within developer and brokerage communities that feed its acquisition pipeline [valye_report_excerpt][S1]. Its multi-pronged approach—acquisitions skewed toward stabilized leases coupled with blend-and-extend leasing strategies—adds layers of optionality when managing both tenants and financial resources.

As macroeconomic uncertainty persists—including tenant-level credit concerns—NETSTREIT’s inherent diversification across numerous states, sectors, and tenants should continue to serve as ballast against volatility. Meanwhile, efficient debt management backed by investment grade status will be critical in optimizing cost structures amidst the evolving interest rate environment.

By stewarding this sizeable portfolio composed predominantly of necessity-driven assets underpinned by long-duration leases to strong tenants, NETSTREIT positions itself as a defender of dependable retail real estate—a niche increasingly prized for predictable income in uncertain times.

This analysis is intended solely for informational purposes regarding NETSTREIT Corp.’s business model and market positioning as of early 2026. It does not constitute investment advice or recommendations regarding securities transactions. Readers should conduct their own due diligence or consult professional advisors before making any decisions related to investments described herein.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments