Yinfu Gold's Shift From Minerals to Digital Data Faces Regulatory and Capital Hurdles

Recent quarterly results show Yinfu Gold’s ongoing operating losses amid challenges in monetizing its sizable customer database within a complex PRC regulatory environment.

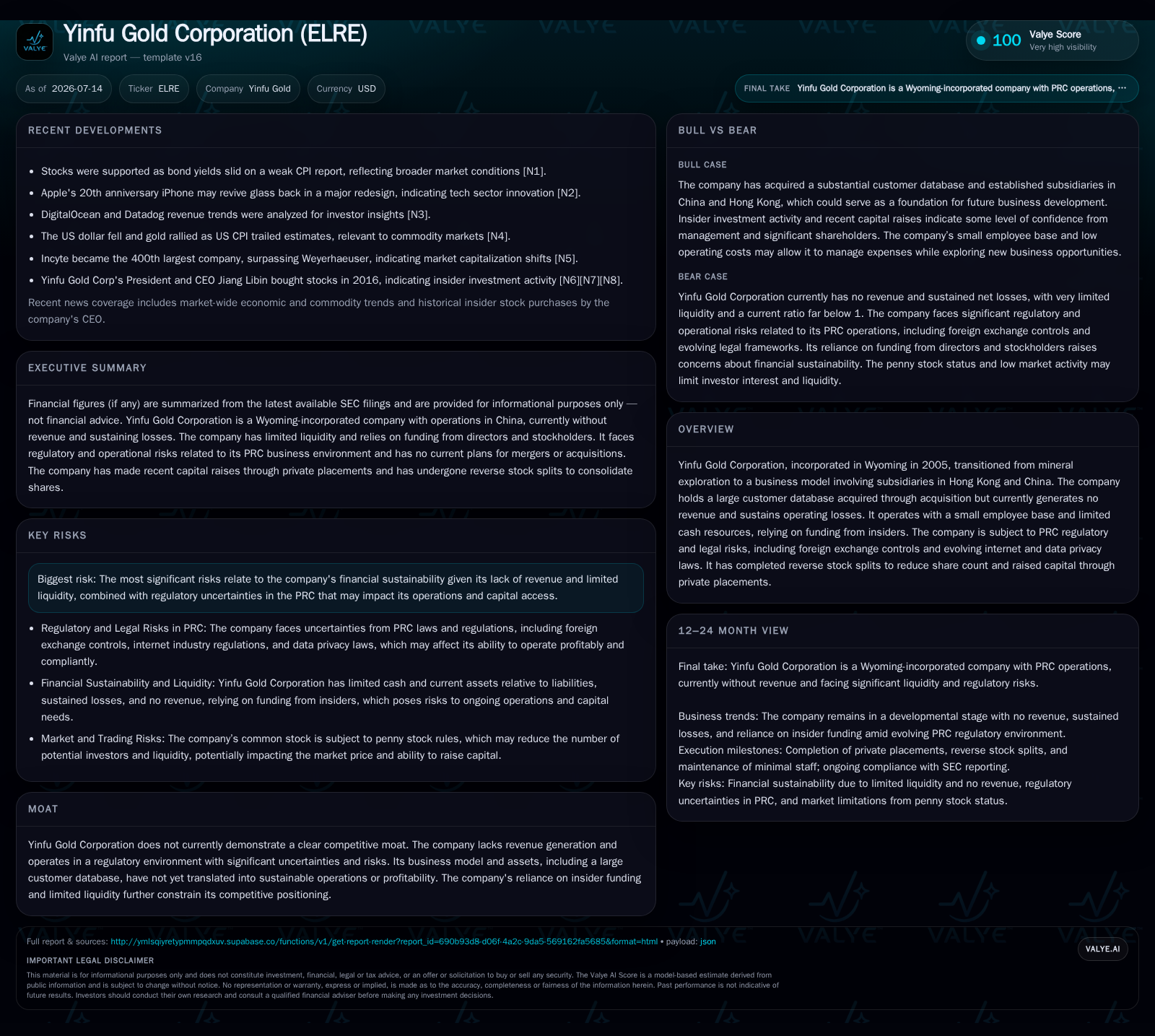

Yinfu Gold Corporation remains an internet services and data management company in transition, having shifted from mineral exploration to managing a large digital customer database. Its February 2026 quarterly filing highlights the persistence of operating losses with no revenue generation, underscoring continued dependence on insider funding. Regulatory uncertainties in China, including data privacy, foreign exchange controls, and evolving internet industry rules, weigh heavily on the company’s operational and financial viability. Despite plans to expand headcount and improve operations, monetization barriers and capital constraints pose significant near-term challenges.

Q2/2026 Filing Highlights Continued Operating Losses Without Revenue Realization

Yinfu Gold Corporation's latest quarterly report for the period ended March 31, 2026 ([S2]) confirms a continuation of the company’s struggles as it records no revenue while sustaining a net loss of $131,062 and operating loss near $148,000 ([F1]). This persistent operating deficit underscores the firm’s inability so far to monetize its core digital assets despite owning a sizeable customer database. The absence of top-line inflows places pressure on liquidity dynamics as current assets are reported at only $14,287 against current liabilities exceeding $650,000 ([F1]), yielding a razor-thin current ratio of approximately 0.02. These numbers reveal critical constraints on operational runway.

Given the lack of revenue generation capability from existing assets or service offerings at this stage, the company continues to rely exclusively on funding from its president and directors for ongoing labor contributions and working capital support ([S1]). A near-term risk is evident: failure to raise further capital could force cessation of operations—a tail risk that threatens shareholder value preservation. The quarter’s financials concretize the gap between asset potential (31 million customer records) versus commercial traction.

Legacy Customer Database: Potential Digital Asset Challenged by Monetization Barriers

The company transitioned from mineral exploration towards internet services after acquiring Yinfu Gold International Holdings Limited in Hong Kong and its Chinese subsidiary in 2017 ([S4]). Notably, through a purchase agreement finalized in late 2014 ([S3]), Yinfu secured ownership of a large customer database tied to cei.dahuacheng.com comprising approximately 31 million registered members as of that date. This accumulation represents a considerable digital asset whose latent value lies in data monetization.

Operating in the Internet Services and Data Management sector typically involves generating revenues via licensing customer data, offering online platforms with subscription fees or advertising-based models, or deploying advanced analytics services (). Yet Yinfu has yet to establish meaningful revenue streams from these activities—highlighting execution challenges common to early-stage digital asset managers lacking scale or product-market fit.

Compounding these difficulties is their limited human capital—only three employees currently support operations including the president, who receives modest monthly compensation ([S5]). Plans for gradual headcount increase up to twenty over the next year hint at intended expansion efforts necessary for building infrastructure capable of user engagement improvements or new product development ([S1]). Until such operational scaling occurs alongside clearer revenue strategies, monetization barriers will persist.

PRC Regulatory Environment Presents Significant Operational Constraints and Risks

Operating across Hong Kong and Mainland China exposes Yinfu Gold to substantial regulatory complexity. China's regulatory landscape for internet businesses is notably stringent—encompassing data privacy laws (Cybersecurity Law), restrictions on cross-border data transfers, telecom licensing mandates (ICP licenses), and governance over digital content ([S27], [S26]). Compliance costs escalate alongside risks as regulations evolve unpredictably.

Foreign exchange controls represent another considerable obstacle. Under SAFE Circular 37 issued by China’s State Administration of Foreign Exchange (SAFE) ([S1], [S20]), PRC residents holding shares in offshore special purpose vehicles like Yinfu must register such holdings; failure leads to blocking profit remittances or capital injections by subsidiaries in China. While Yinfu claims attempts to notify known PRC shareholders for registration compliance, enforcement variability creates risk exposure that may restrict liquidity movements critical for operational funding.

Further compounding uncertainty are new provisions under Article 177 of China’s amended Securities Law which curtail direct investigation efforts by overseas regulators inside China without Chinese authority cooperation ([S9], [S12]). The interpretative ambiguity heightens audit transparency risks due to PCAOB inspection limitations noted under the Holding Foreign Companies Accountable Act (HFCAA) ([S28]). Although Yinfu uses a Malaysia-based PCAOB-registered auditor compliant with inspection requirements thus far, future political or regulatory shifts could jeopardize trading eligibility in U.S. markets.

These factors collectively erode operational freedom by increasing compliance burdens while restricting timely access to offshore capital flows—a crucial challenge given Yinfu's lack of revenue or alternative external funding channels.

Structural Industry Realities: Competitive Dynamics Among Internet Data Service Firms Under PRC Law

Yinfu finds itself competing indirectly within a landscape dominated by large-scale Chinese internet platform operators like Alibaba and Tencent—entities boasting hundreds of millions of active users leveraging diversified revenue streams through advertising platforms, subscription services, e-commerce facilitation, and data analytics products (). These players benefit from established ecosystems ensuring high user engagement metrics critical for effective monetization.

Smaller firms akin to Yinfu often struggle with scale effects necessary for balancing customer acquisition costs against subscription or advertising lifetime value metrics. Additionally, stringent PRC telecommunication licensing requirements impose barriers inhibiting rapid entry or platform proliferation without local partnership arrangements or backed governmental approvals ().

Thus Yinfu’s smaller scale combined with evolving compliance complexities situates it at a disadvantage compared with mature peers possessing integrated technology stacks and extensive capital resources enabling sustained investment into user growth and retention strategies.

Growth Outlook Hinged on Expanding User Base, Monetizable Services Launch, and Regulatory Clarity

Prospective growth drivers highlighted by Yinfu’s management center around gradual expansion of their digital infrastructure—including hiring plans targeting up to twenty new staff within twelve months—as well as planned augmented reliance on independent professionals for auditing and legal compliance functions supporting their Nasdaq listing ambitions ([S1], [S3]).

Operationalizing this growth will involve transitioning dormant large-scale customer databases into active users generating measurable engagement through subscription models or advertising platforms—both requiring requisite technology upgrades like enhanced data analytics capabilities. Securing regulatory approvals while achieving smoother inter-jurisdictional data flow compliance remains a gating constraint tied directly to unlocking revenue channels.

Partnerships or acquisitions could further accelerate capabilities though no explicit deals have been disclosed recently suggestive of immediate changes. Regulatory clarity potentially arising from more precise interpretations or implementations around foreign exchange registrations and cybersecurity reviews would materially reduce overhead risks presently overshadowing strategic scaling ambitions.

Capital and Operational Risk Management Amid Limited Cash Reserves and Equity Structure Adjustments

Financially Yinfu is managing under acute constraint given a cash balance recorded at just $560 as of December 31, 2022 ([F1]), current assets totaling only about $14K against significantly higher current liabilities exceeding $650K as of March 31, 2026 ([F1]), amplifying solvency concerns. Total debt figures remain outdated but were historically elevated ([F1]) accentuating leverage vulnerability absent active deleveraging initiatives.

Capital raises have been limited predominantly to privately placed equity financings aggregating modest sums (~$120K reported in early 2023) coupled with director loans chiefly utilized for working capital needs ([S6]). The absence of external funding visibility implies concentrated reliance on insider financing which impacts scalability unless supplemented soon.

Equity structure dynamics have seen deliberate reverse stock splits undertaken—the latest one being a five-for-one consolidation approved in late 2021 designed primarily for share count rationalization purposes facilitating marketability improvements amid microcap trading challenges ([S4]). Such actions signal management focus on improving stock liquidity profiles though do not resolve underlying cashflow deficiencies.

"Reverse Stock Split" Strategy: Share Consolidation as a Liquidity and Listing Maneuver

Yinfu's history includes multiple reverse stock splits: initially enacted around late 2016 at roughly one-for-100 ratio then another five-for-one consolidation in late 2021 ([S4]). These structural equity maneuvers appear intended explicitly to mitigate issues endemic among microcap securities—namely excessive float fragmentation impacting liquidity—and preserve Nasdaq listing standards which often require minimum price thresholds per share.

While common among small public tech companies facing valuation pressure combined with thin trading volume environments—to preserve investor interest—reverse splits can carry perception risks including implied distress signals. For Yinfu this mechanism forms part of broader efforts addressing both marketability limitations caused by massive pre-split share counts (initially close to one billion outstanding pre-2016) alongside attempts at resetting shareholder base composition during phases marked by capital scarcity.

Though essential tactically given circumstances, reverse splits are not substitutes for fundamental operational progress required to unlock sustainable business momentum through real revenue streams aligned with sector growth vectors.

Financial Profile Discussion

This financial tightness reflects sector realities where nascent digital asset managers lacking recurring revenue must balance investments into user acquisition against constrained funding access—compounded here by regulatory friction encountered due to operations across Hong Kong/China jurisdictions with volatile legal landscapes controlling foreign exchange movements.[S20], [S25]

Continued reliance on private placements restricted by thin liquidity places stress on achieving planned employment growth aimed at strengthening technological capabilities necessary for monetization pilots.[S3] Absence of confirmed institutional or broad shareholder backing magnifies execution risk relative to peer benchmarks where sizeable venture or public funding supports sustained R&D ramp-up.

This analysis is based strictly on publicly available SEC filings as cited; it excludes any speculative forward-looking statements absent company confirmation. It is intended solely as an informational review grounded in verified documentation without offering investment advice or research views.

Financial position in context

Current assets of $14287 and current liabilities of $650213 imply a current ratio near 0.02x for 2026-03-31 [F1]

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments