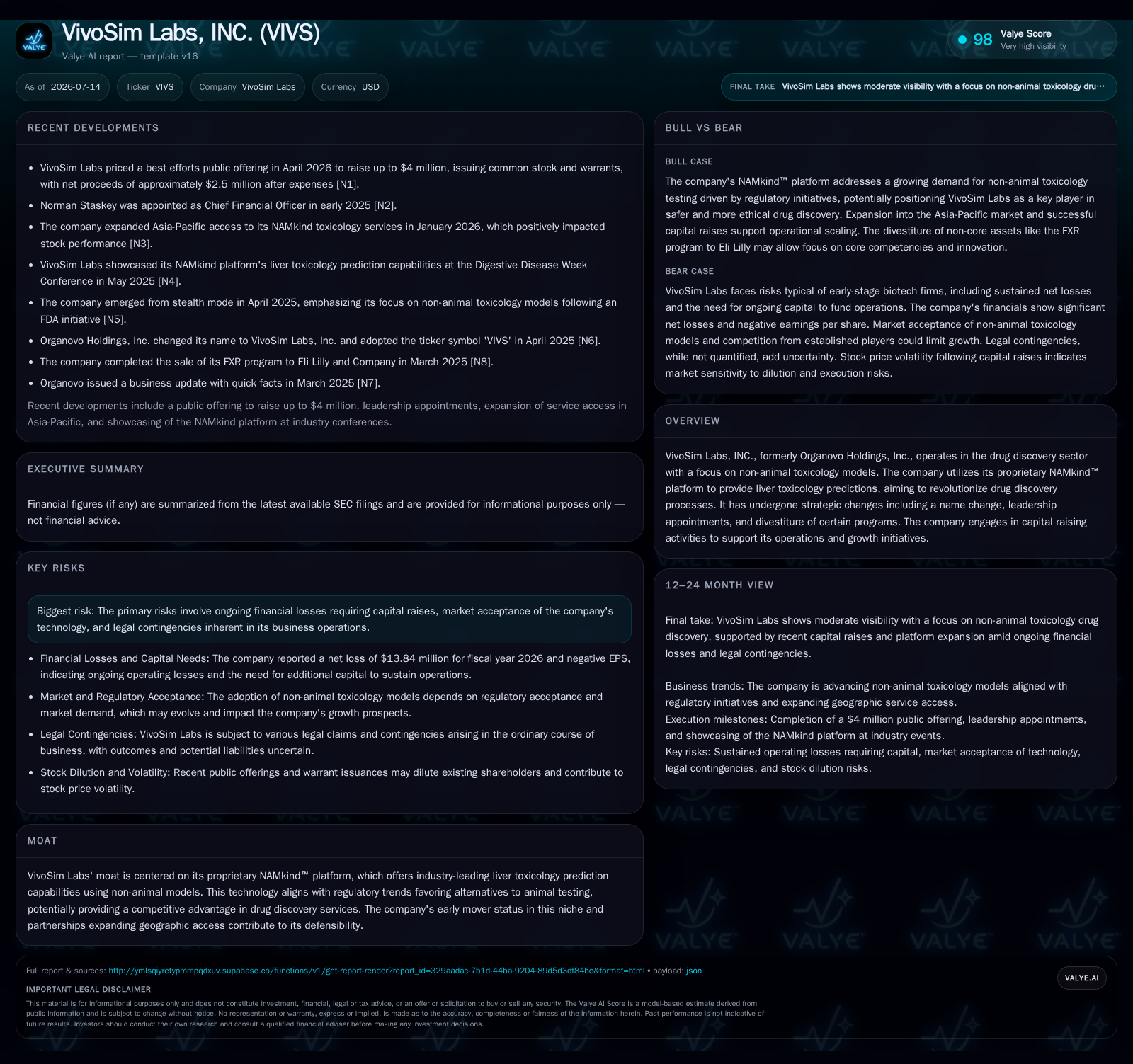

VivoSim Labs Advances Non-Animal Liver Toxicology Amid Capital and Market Adoption Challenges

The company leverages its proprietary NAMkind™ platform to provide predictive liver toxicology services aligned with regulatory shifts away from animal testing.

VivoSim Labs, formerly Organovo Holdings, focuses on non-animal liver toxicology prediction through its NAMkind™ platform, aiming to disrupt traditional preclinical drug testing paradigms. The company reported ongoing operating losses in its latest filings and is actively raising capital to support R&D and corporate activities. Its moat relies on early positioning in regulatory-driven alternatives to animal testing, but widespread market adoption and financial sustainability remain key risks. Monitoring collaboration growth, regulatory milestones, and cash runway will be critical for assessing progress.

Recent Operating Update

VivoSim Labs, Inc., formerly known as Organovo Holdings, filed its latest annual report (Form 10-K) on July 14, 2026, outlining its strategic pivot towards non-animal liver toxicology prediction through its proprietary NAMkind™ platform [S1]. This platform integrates advanced in vitro assays with computational biological modeling to deliver predictive insights into drug-induced liver injury, addressing a critical bottleneck in preclinical drug discovery. The company’s repositioning reflects growing regulatory and industry momentum favoring alternatives to traditional animal testing, aiming to provide pharmaceutical clients with faster, ethically aligned toxicology data.

Business Model

Operating within the biotechnology drug discovery sector, VivoSim Labs focuses on preclinical toxicology prediction services centered on liver toxicity. Its NAMkind™ platform combines biological modeling and high-throughput screening to generate predictive toxicology reports that pharmaceutical and biotechnology companies use during early candidate screening phases. Revenue is primarily derived from service contracts for toxicology assessments and licensing agreements granting access to the NAMkind™ technology.

The company’s business model hinges on expanding pharmaceutical partnerships, achieving regulatory validation milestones, and strengthening its intellectual property portfolio to build a competitive moat. The NAMkind™ platform’s ability to reduce time-to-data delivery compared to animal models is a key value proposition, potentially accelerating go/no-go decisions in drug development. However, VivoSim’s current revenue remains limited, with historical top-line just above $1 million as of fiscal year 2018, reflecting its developmental-stage profile and reliance on ongoing R&D investment [F1]

Industry Structure and Competitive Position

The drug discovery toxicology landscape includes large contract research organizations (CROs) such as Charles River Laboratories and Covance, which offer comprehensive in vivo animal testing services critical for regulatory submissions. In contrast, VivoSim occupies a niche as an early innovator in non-animal liver toxicology prediction, targeting pharmaceutical clients seeking faster, ethically compliant preclinical testing alternatives.

Regulatory agencies like the FDA have increasingly encouraged the adoption of validated non-animal methodologies, enhancing VivoSim’s strategic opportunity. Nonetheless, competition arises from both established CROs expanding into alternative models and emerging biotech firms developing organ-on-chip systems or AI-driven computational toxicology platforms. VivoSim’s success depends on demonstrating the NAMkind™ platform’s predictive validity, report turnaround times, and seamless integration into pharmaceutical workflows.

Growth Drivers

Several structural trends support VivoSim’s growth prospects:

- Regulatory Pressure to Reduce Animal Testing: Global legislative and ethical initiatives are driving pharmaceutical companies to adopt validated non-animal toxicology platforms.

- Pharmaceutical Demand for Efficiency: Rising R&D costs incentivize faster, cost-effective preclinical screening to streamline candidate selection.

- Technological Advances: Improvements in biological modeling accuracy and assay reproducibility enhance platform reliability.

- Expanding Collaborations: Partnerships with global pharmaceutical firms broaden market access and facilitate iterative platform refinement.

- Regulatory Acceptance Milestones: Formal endorsements or guidances from regulatory bodies validate platform utility and encourage adoption.

- Growing Pharmaceutical R&D Budgets: Increased investment in drug discovery fuels demand for specialized toxicology services.

- Geographic Expansion: Targeting emerging biotech hubs may unlock new client segments.

Key performance indicators to monitor include the number of active pharmaceutical partnerships, validation studies confirming NAMkind™ predictive accuracy against clinical or animal benchmarks, client retention and contract renewal rates, and regulatory communications evidencing acceptance progress.

Risks and Watchpoints

VivoSim faces several risks that could impact its trajectory:

- Capital Dependency: The company reported operating losses of $11.5 million and net losses of $13.8 million for fiscal year 2026, reflecting substantial R&D spending typical of early-stage biotech [F1]. This loss profile necessitates frequent capital raises, with recent equity offerings generating approximately $2.5 million net proceeds in April 2026 to support operations and intellectual property protection [S6][S7][S8]. Sustained funding is critical to maintain R&D and commercial activities.

- Technology Adoption Uncertainty: Pharmaceutical sponsors may be cautious in replacing established animal models due to regulatory conservatism and validation requirements.

- Competitive Pressure: Established CROs and innovative biotech startups intensify competition, potentially compressing margins and client acquisition.

- Legal Contingencies: The company acknowledges potential claims and litigation inherent to biotech operations, which could impact financials and reputation [S1][S4].

- Long Sales Cycles: Contract negotiations with pharmaceutical clients are typically protracted, influenced by shifting development priorities.

- Platform Validation Challenges: Scientific reproducibility and regulatory acceptance of novel biological systems remain hurdles.

- Dilution Risk: Frequent equity financings may dilute shareholder value.

- Partner Concentration Risk: Dependence on a limited number of pharmaceutical partnerships could increase revenue volatility.

Monitoring capital raise outcomes, partnership announcements with milestone disclosures, regulatory feedback on NAMkind™, litigation updates, and scientific validation publications will be essential to assess risk mitigation and progress.

What To Watch Next

Near-term indicators of VivoSim’s advancement include:

- Expansion of drug discovery collaborations or licensing agreements signaling commercial traction.

- Regulatory milestones such as guidance letters or approvals endorsing non-animal liver toxicology predictions.

- Follow-on capital raises and their terms, reflecting investor confidence and operational funding stability.

- Quarterly financial disclosures detailing burn rate trends and cash runway beyond the reported $5.0 million cash balance as of March 31, 2026 [F1].

- Scientific publications or public commentary demonstrating NAMkind™’s predictive accuracy relative to competitors.

- Management updates on product pipeline development and commercial expansion strategies in SEC filings.

These markers will help determine whether VivoSim can transition from a developmental-stage biotech incurring losses to a sustainable service provider leveraging its differentiated technology amid evolving industry standards.

Financial Profile Discussion

As of March 31, 2026, VivoSim Labs held $5.0 million in cash and equivalents against current liabilities of $2.8 million, resulting in a current ratio of 2.38, indicating adequate near-term liquidity [F1]. The company’s total debt is negligible, approximately $9,500 last reported, minimizing leverage risk but underscoring reliance on equity capital markets for growth financing.

The April 2026 equity offering raised net proceeds of about $2.5 million through the issuance of common stock and warrants, intended to fund working capital, research and development, regulatory affairs, and intellectual property protection [S6][S7][S8]. Given the persistent operating losses and negative operating cash flow of $10.8 million in fiscal 2026, further capital raises may be necessary to sustain operations and commercial expansion [F1].

Comparatively, large CROs such as Charles River Laboratories generate multibillion-dollar revenues with positive EBITDA, highlighting VivoSim’s early-stage status focused on technology development rather than scalable service delivery. Similarly, smaller organ-on-chip and computational toxicology firms face analogous challenges bridging scientific innovation to commercial revenue, reflecting sector-wide structural hurdles despite robust demand for animal testing alternatives.

Overall, VivoSim’s financial position requires careful monitoring of capital efficiency, partnership growth, and regulatory validation to balance its technological moat with the realities of funding-intensive biotech commercialization.

Disclaimer: This analysis is for informational purposes only and does not constitute investment advice. Readers should verify details with primary sources.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments