Surge Components Strengthens Liquidity Amidst Steady Electronic Component Distribution

Surge Components’ Q2 2026 results reveal a stable revenue base and robust liquidity amidst limited public business detail.

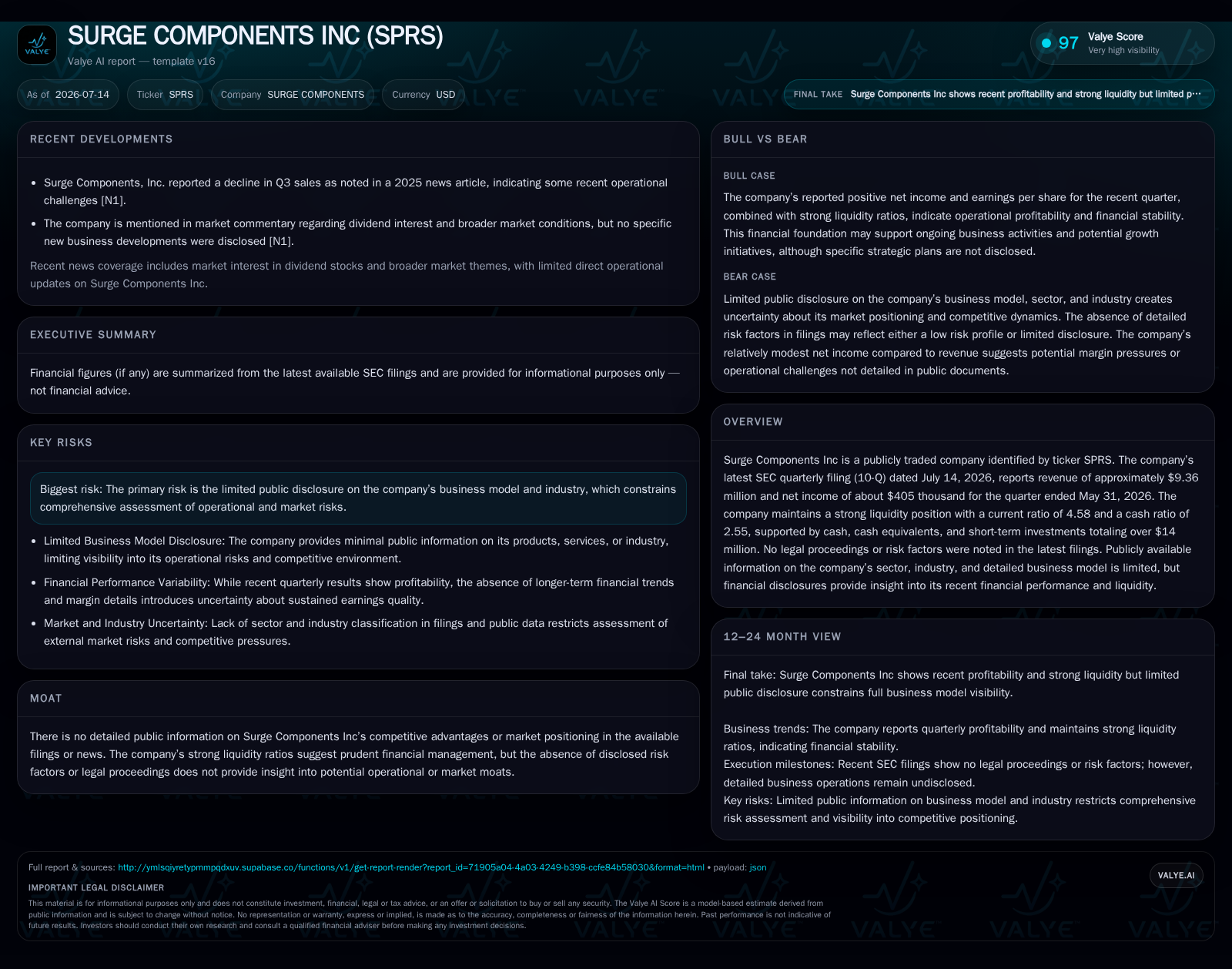

Surge Components Inc reported $9.36 million in revenue and $405,000 in net income for Q2 2026, maintaining strong liquidity with a current ratio of 4.58 and cash equivalents exceeding $5 million. While the company provides minimal detail on its operational model or market positioning, its financial stability suggests disciplined supply chain management consistent with electronic component distribution industry norms. Key risks remain opaque due to limited disclosure, necessitating close monitoring of inventory management and demand trends in a cyclical sector.

Q2 Results Illustrate Stability without Major Upside

Surge Components Inc’s second quarter ended May 31, 2026, saw reported revenue of approximately $9.36 million alongside net income near $405 thousand [S2][F1]. These figures indicate ongoing operational stability given the company’s scale but do not signal any significant growth acceleration or margin expansion at this early point. Importantly, no risk factors or legal proceedings were noted in the filing, underscoring a clean risk profile for now [S2][S4]. In the context of a cyclical electronic components market prone to fluctuating OEM demand and semiconductor shortages, maintaining profitability suggests effective cost control and order fulfillment capability.

This steady financial snapshot matters because small- to mid-sized distributors often face pronounced volatility from component availability and pricing shifts, making consistent quarterly earnings an indicator of disciplined supply chain management. Future quarters showing continued revenue growth or rising margins would confirm this steadiness as more structural rather than transient.

Decoding Surge’s Electronic Component Distribution Model Amid Limited Public Detail

Although the company provides scant specifics on its detailed business model in filings, it can be reasonably inferred that Surge acts as a downstream intermediary in the electronic components supply chain—purchasing semiconductors and passive components from manufacturers for resale primarily to original equipment manufacturers (OEMs) and electronic manufacturing services (EMS) providers [S1][S2]. Such distributors commonly monetize by volume sales across broad bills of materials (BOMs), capturing margin via pricing markups balanced against inventory holding costs.

Revenue dynamics likely tie closely to managing just-in-time (JIT) inventory programs that minimize customer lead time while mitigating Surge's own inventory obsolescence risk amid rapid technology changes typical in electronics. Further differentiation often emerges from value-added services including kitting components per BOM requirements or providing supply chain logistics support that raise switching costs for customers.

Margins in this archetype hinge on inventory turnover ratios, procurement efficiency under volatile semiconductor supply conditions, and ability to price dynamically around product mix shifts. The absence of explicit disclosures precludes granular visibility into Surge’s SKU breadth or service scope but suggests reliance on established industry economics common among mid-tier distributors.

Industry Context: Supply Chain Dynamics and Competitive Benchmarks

Within the broader electronic components distribution landscape, large players such as Arrow Electronics and Avnet exemplify scale advantages with extensive global inventories and embedded value-added service capabilities that enhance customer retention through technical design support and flexible delivery models. Conversely, firms like Mouser Electronics specialize in rapid delivery from comprehensive catalogs addressing engineer requirements directly.

Surge's reported scale positions it below these giants but within a competitive tier where operational agility and liquidity become critical differentiators. Efficient supply chain resilience—including minimizing backorders through sophisticated demand forecasting—and optimizing days sales of inventory (DSI) are key metrics shaping profitability.

Pricing pressures stem from manufacturer direct sales initiatives alongside competing distributors who may erode margins via promotional pricing. Surge’s ability to maintain positive net income signals some effective navigation of these pressures despite competitive headwinds.

Growth Vectors Supported by Outsourcing Trends and Emerging Technologies

Industry growth drivers align with broad trends boosting electronic components demand: expanding consumer electronics driven by IoT device penetration; accelerating automotive electronics adoption for electric vehicles; rollout of 5G network infrastructure requiring specialized semiconductors; and increased industrial automation fostering complex BOMs.

Outsourcing strategies by OEMs increasingly favor distributors who can provide integrated supply chain services reducing lead times and supporting BOM complexity through kitting or testing services. For Surge to capture these tailwinds sustainably would require scaling value-added offerings alongside enhancing inventory efficiencies.

KPIs such as increasing order fulfillment rates, improving gross margin percentages through better product mix control, and managing DSI effectively will act as leading indicators whether Surge capitalizes on these macro trends.

Watchpoints: Demand Cyclicality and Supply Constraints as Potential Risks

Persistent risks for Surge include inherent cyclicality in electronics sector causing order volume volatility tied to end-market product launches or macroeconomic fluctuations. Semiconductor shortages remain relevant globally due to constrained capacity expansions impacting suppliers upstream; this can elevate backorder levels forcing costly expedited shipping or lost sales if unmet.

Pricing erosion from intensified distributor competition or manufacturer direct channels could pressure margins absent scale advantages. Inventory obsolescence due to rapid technological shifts mandates vigilant inventory turnover management—slow-moving stock risks realization losses.

Further opacity regarding customer concentration elevates credit risk considerations as exposure to few key accounts could materially impact revenues unexpectedly [S1][S2]. Logistics disruptions also pose threat given global transportation complexities.

Near-Term Milestones: Monitoring Order Fulfillment Efficiency and Inventory Measures

Given limited disclosure granularity, market observers should prioritize tracking quarter-over-quarter trends in revenue growth signaling demand capture effectiveness. Gross margin stability or improvement would indicate tighter pricing power or operational gains.

Inventory turnover ratio enhancements reflect tighter working capital deployment critical for small distributors balancing cash flow needs against component availability risks. Days sales of inventory (DSI) trends will elucidate if Surge improves just-in-time inventory alignment reducing capital tied up in stock.

Customer retention metrics—though not publicly reported—are vital downstream indicators influencing repeat order volumes amid competitive pressures. Consistent positive net income coupled with these operational KPIs can validate execution capabilities beyond headline financials.

Financial Profile Discussion: Liquidity Strength as Capital Buffer

As of May 31, 2026, Surge Components held approximately $5.23 million in cash & equivalents supported by total current assets nearing $27 million against current liabilities below $5.9 million, yielding a healthy current ratio of about 4.58 [F1]. This liquidity buffer is robust relative to the company’s operating scale providing significant runway for navigating potential industry demand troughs or temporary supply chain disruptions.

A cash ratio near 2.55 further reflects solid short-term financial flexibility uncommon among smaller electronic components distributors who typically face working capital constraints given inventory-intensive operations [F1]. This positions Surge favorably compared with many peers who must rely more heavily on credit lines or factoring arrangements under stress.

However, the relatively modest absolute scale limits financial leverage versus much larger peers like Arrow Electronics or Avnet that couple size with diverse global funding access allowing more aggressive capital investments or acquisitions enhancing competitive moats.

In summary, Surge Components exhibits prudent balance-sheet management underpinning operational steadiness amid sector cyclicality though absent detailed disclosures limit full assessment of strategic positioning or growth durability.

Disclaimer: This analysis is based solely on public filings dated July 14, 2026 ([S2], [S1]) and company facts data ([F1]). It does not constitute investment advice nor predict future performance.

Financial position in context

As of 2026-05-31, companyfacts shows $5mm in cash and equivalents [F1]. Current assets of $27mm and current liabilities of $6mm imply a current ratio near 4.58x for 2026-05-31 [F1].

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments