SemiLEDs Corp Wrestles with IP Risks and Operational Losses in LED Chip Market

SemiLEDs’ latest quarter reveals ongoing net losses and liquidity constraints amid intellectual property challenges in the competitive LED chip segment.

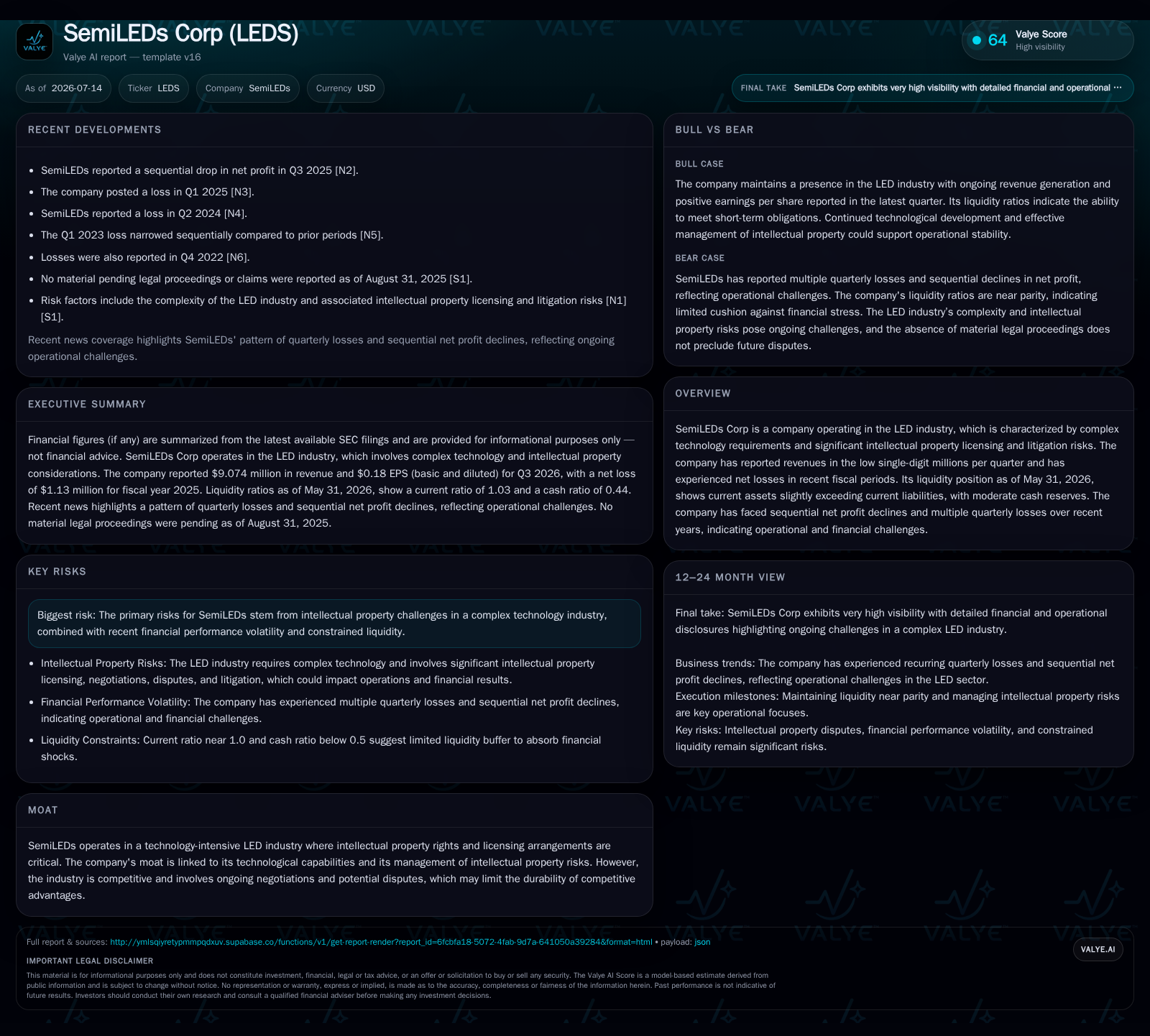

In its Q3 fiscal 2026 results, SemiLEDs Corp reported continued net losses and modest liquidity, highlighting persistent operational weaknesses in a capital-intensive LED chip manufacturing environment. The company’s revenue streams derive primarily from LED chip design and fabrication, supplemented by intellectual property licensing, yet profit recovery remains elusive. Structural industry factors such as intense patent litigation risk and pricing pressure further strain margins, while manufacturing yield variability and capacity utilization challenges limit scale benefits. Upcoming milestones center on licensing expansion and operational efficiency improvements to stabilize the business.

Q3 Fiscal 2026 Results Highlight Persistent Operational and IP Challenges in LED Chip Manufacturing

SemiLEDs Corporation’s third quarter fiscal 2026 results, reported for the period ended May 31, 2026, reaffirm ongoing operational difficulties characterized by net losses and constrained liquidity amid a complex intellectual property environment [S2][S7]. The company continues to operate in a capital-intensive LED semiconductor wafer fabrication sector, where production yield rates, capacity utilization, and patent-related risks critically influence financial outcomes.

Business Model: LED Chip Design, Wafer Fabrication, and Intellectual Property Licensing

SemiLEDs primarily generates revenue through the design and manufacturing of LED chips, involving semiconductor wafer fabrication processes such as epitaxial growth, die bonding, and packaging. These upstream and midstream activities supply LED components to downstream manufacturers who integrate them into lighting modules, consumer electronics displays, and automotive lighting systems [S1]. Maintaining high production yield rates and minimizing defect rates are essential KPIs that directly impact unit costs and gross margins. The company’s wafer fabrication operations must optimize substrate material selection, phosphor conversion efficiency, thermal management, and luminous efficacy to remain competitive.

In addition to chip sales, SemiLEDs derives revenue from intellectual property licensing fees. This licensing revenue stream depends on the company’s ability to monetize its proprietary LED technologies, which involves navigating a dense patent landscape and managing ongoing patent litigation risks. Licensing income can provide a recurring revenue component but is subject to negotiation outcomes and potential disputes, adding variability to overall cash flow.

Intellectual Property Risks and Competitive Positioning

The LED manufacturing industry is marked by a complex and aggressive intellectual property environment, with overlapping patents and frequent litigation among competitors. SemiLEDs acknowledges exposure to patent litigation risks that can constrain operational flexibility and increase legal expenses [S1]. This environment challenges smaller players to maintain a sustainable technological moat.

In comparison, larger vertically integrated competitors such as Cree Inc. and Nichia Corporation benefit from extensive wafer fabrication capacity and broad IP portfolios, enabling them to leverage economies of scale and invest heavily in advancing quantum efficiency and light extraction efficiency. These peers can reduce unit costs through higher capacity utilization and improved production yields, placing pricing pressure on smaller manufacturers like SemiLEDs.

Operational Challenges: Capital Intensity, Yield Variability, and Pricing Pressure

The semiconductor wafer fabrication process for LED chips requires significant capital investment in advanced equipment capable of precise epitaxial growth. SemiLEDs’ ability to absorb fixed costs depends heavily on capacity utilization rates; suboptimal utilization inflates per-unit costs and compresses already thin gross margins [S1]. Production yield rates remain a critical operating variable, as defective chips increase scrap rates and extend customer qualification cycles, delaying volume ramp-up and revenue recognition.

Price competition in the LED chip market is intense, driven by established players with scale advantages. This competitive pressure limits SemiLEDs’ ability to increase average selling prices (ASP), constraining revenue growth despite efforts to improve product differentiation through R&D innovation.

R&D Investment Amid Cyclical Demand and Cash Flow Constraints

SemiLEDs allocates a substantial portion of its operating budget to research and development, focusing on enhancing thermal management, luminous efficacy, and exploring new substrate materials to improve chip performance [S1]. These R&D efforts are vital for maintaining technological relevance in fast-evolving LED applications, including automotive lighting, consumer electronics, and emerging niches such as horticultural and UV LEDs.

However, the company’s relatively modest revenue base limits the scalability of R&D spending, placing pressure on cash flow. Demand cyclicality in end markets like consumer electronics further exacerbates revenue volatility, complicating working capital management and extending customer qualification cycles.

Key Risks: Patent Litigation, Margin Pressure, and Customer Qualification

SemiLEDs faces ongoing risks from patent litigation common in the LED semiconductor industry, which can result in costly legal proceedings or royalty obligations that erode margins [S1]. Additionally, variability in production yields increases both direct costs of goods sold and indirect costs associated with prolonged qualification cycles required by OEM customers.

Customer qualification processes represent a significant barrier to scaling chip sales volume. These cycles involve rigorous defect rate control and performance validation, with delays potentially stalling capacity utilization improvements and margin expansion.

Growth Prospects Linked to Licensing and Technological Advances

Future growth for SemiLEDs hinges on expanding intellectual property licensing revenues and achieving operational efficiencies that enable higher chip output volumes at competitive ASPs. Technological advancements that improve quantum efficiency and thermal dissipation could facilitate entry into higher-value segments such as automotive LED lighting, which benefits from regulatory incentives promoting energy-efficient illumination.

Emerging applications like miniaturized high-brightness LEDs and UV-LEDs offer additional avenues for leveraging R&D investments into niche market penetration beyond commoditized general lighting.

Financial Position: Tight Liquidity Amid Ongoing Losses

As of May 31, 2026, SemiLEDs held approximately $6.0 million in cash and cash equivalents against current liabilities of about $13.5 million, resulting in a current ratio of approximately 1.03 [F1]. Total current assets stood near $13.9 million, indicating limited working capital buffer to absorb operational disruptions or fund strategic initiatives without external financing [F1].

The company has reported consistent quarterly net losses through fiscal 2025 and into 2026, underscoring the challenge of achieving sustainable profitability in a capital-intensive and competitive industry [S2][F1]. Although total debt figures date back several years and no recent refinancing activities have been disclosed, the existing debt obligations form part of the company’s financial structure [F1].

What to Watch: Licensing Revenue, Yield Improvements, and Capacity Utilization

Key near-term indicators to monitor include quarter-over-quarter changes in intellectual property licensing revenue, which could signal successful contract negotiations or dispute resolutions enhancing recurring income stability. Operational metrics such as improvements in production yield rates and capacity utilization will be critical to reducing unit costs and expanding gross margins.

Additionally, reductions in defect rates and shortened customer qualification cycles would indicate progress toward faster time-to-market and stronger competitive positioning against larger incumbents.

This analysis integrates SemiLEDs’ latest regulatory filings through mid-2026 with industry context highlighting the capital intensity, intellectual property complexities, and competitive dynamics shaping the company’s operational and financial outlook.

Financial Snapshot Summary

- Cash and equivalents: ~$6.0 million (as of 2026-05-31) [F1]

- Current assets: ~$13.9 million (as of 2026-05-31) [F1]

- Current liabilities: ~$13.5 million (as of 2026-05-31) [F1]

- Current ratio: ~1.03 (as of 2026-05-31) [F1]

- Ongoing quarterly net losses reported through fiscal 2025 and early 2026 [S2][F1]

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments