Jubilant Flame International Faces Acute Liquidity Crisis with No Revenue Generation

Latest quarterly filing reveals zero revenues and a critical liquidity shortfall, raising substantial operational sustainability concerns.

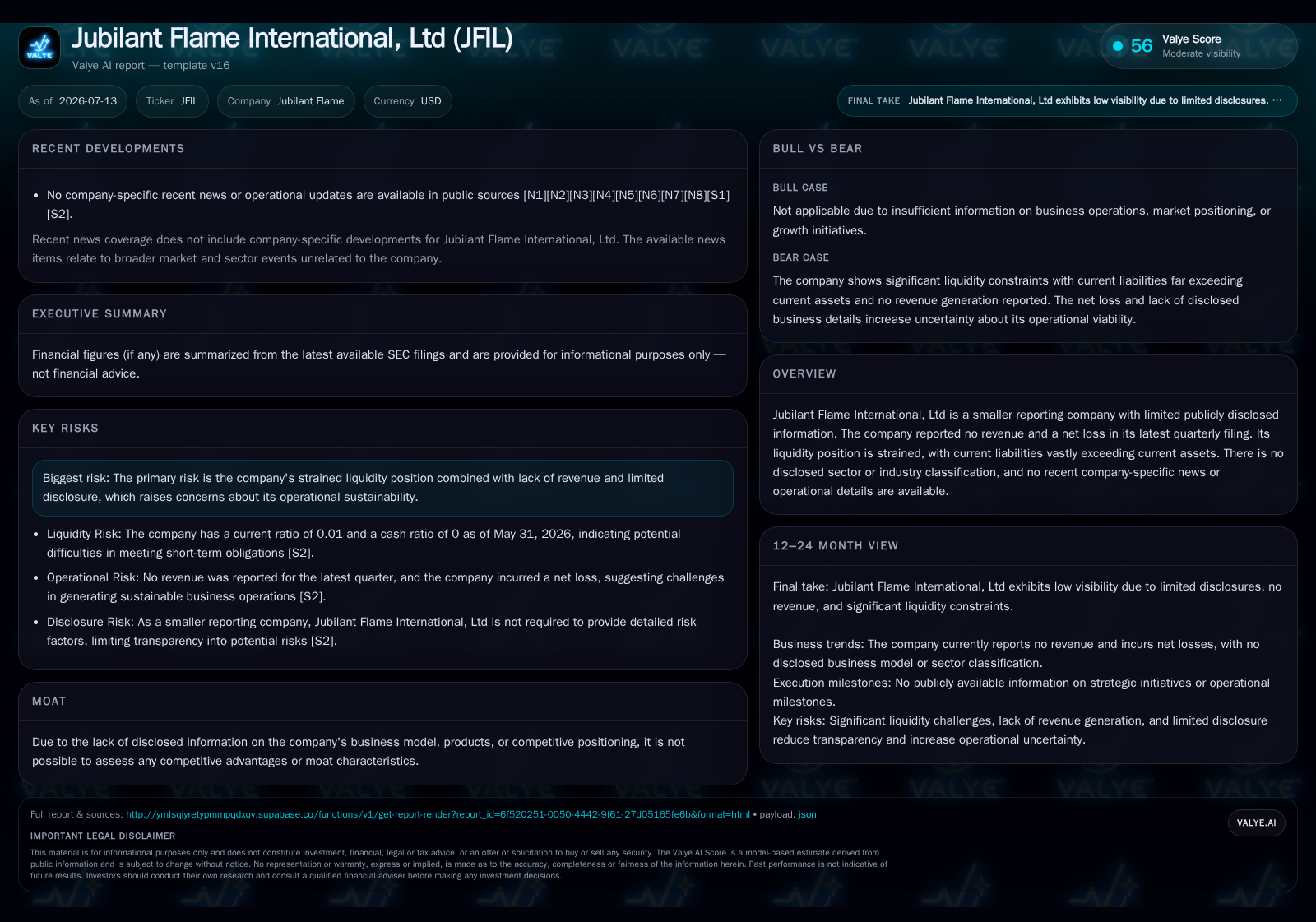

Jubilant Flame International’s most recent 10-Q filed on July 13, 2026, reports no generated revenue alongside a significant net loss and a current ratio near zero, indicating an acute liquidity crisis [S2][F1]. The lack of disclosed operating activities and capital expenditure contrasts sharply with typical energy sector businesses whose capital intensity demands steady cash flow. Without clear information on its business model or operational KPIs, Jubilant Flame faces high going concern risks amid industry capital intensity and volatility. Comparisons to integrated oil&gas and midstream peers underscore the challenges for this smaller company to stabilize or grow without improved liquidity and operational transparency.

Latest Quarterly Results Highlight Zero Revenue Amidst Widening Liquidity Gap

Jubilant Flame International’s latest quarterly filing dated July 13, 2026 [S2] affirms continuation of its challenging financial state. The company recorded no revenue during the quarter ended May 31, 2026 [F1], while net losses persisted with a negative net income of approximately $63,507 for the most recent reported period ending February 28, 2026 [F1]. More critically from a solvency standpoint, current liabilities stand at about $1.46 million compared to current assets barely totaling $9,725, culminating in an alarmingly low current ratio near 0.01 [F1].

This grotesquely imbalanced working capital position implies acute near-term liquidity stress threatening ongoing operational viability absent new financing or revenue generation. The lack of any operating revenues combined with growing losses underscores that Jubilant Flame has yet to develop active business operations typical for energy sector participants. This latest filing effectively signals no material progress toward stabilization or turnaround in the company’s operating profile.

Inferring Business Model and Sector Challenges Amid Limited Disclosure

Beyond numeric distress markers, Jubilant Flame offers scant disclosure elucidating its business model or market engagement beyond its corporate name. The inclusion of "Flame" hints at potential linkage to energy commodities—likely within the hydrocarbon space—but neither the annual (2026-04-28) nor quarterly filings provide clarity regarding specific upstream exploration and production (E&P), midstream pipeline infrastructure operations, or downstream refining activities [S1][S2]

Industry-standard reporting norms encompass detailed production volumes expressed in barrels of oil equivalent (BOE), reserve replacement metrics reflecting asset sustainability, capital expenditure outlines capturing investment intensity, and commodity sales revenue that collectively signal operational health and growth trajectory. None of these fundamental indicators appear in Jubilant Flame’s disclosures leaving considerable ambiguity about actual business scope or scale.

This opacity severely constrains analysis; unlike integrated majors who transparently disclose asset bases and segment results endorsing their capital-intensive operations (e.g., ExxonMobil's large-scale E&P and refining platforms), Jubilant Flame’s non-disclosure precludes confident positioning along the energy value chain.

"Flame" Suggests Energy Link but Absence of Operating KPIs Fuels Uncertainty

The word "Flame" arguably connects the company to fossil fuel activities—natural gas combustion phases involved in upstream flaring practices or downstream gas heating applications could be hypothesized. Typically, firms engaged in exploration or pipeline transport rigorously track KPIs such as daily BOE production rates, lifting costs per BOE extracted, pipeline throughput volumes, or refinery utilization rates.

Unfortunately, Jubilant Flame fails to report any such key performance indicators across its filings [S1], depriving stakeholders from visibility into operational scale or efficiency. This is markedly different from independent exploration companies like Devon Energy which regularly update reserve replacement ratios and production volumes critical for assessing asset longevity and earnings quality.

The absence of each standard metric prevents evaluation of market positioning against well-established competitors and raises significant doubts about whether active upstream/midstream operations exist at all.

"Energy Resource" Value Chain Contextualizes Capital Intensity Risks

Energy resource companies across the upstream-to-downstream spectrum face inherently capital-intensive demands: large-scale drilling and exploration programs require multi-million dollar expenditures (CapEx); midstream operators depend on costly pipeline construction; refiners need continuous maintenance investment.

Capital intensity dictates dependence on steady commodity sales generating operating cash flow sufficient to cover expenditures while servicing debt obligations. For entities lacking strong cash generation like Jubilant Flame—with no reported commodity sales revenue—the discrepancy quickly manifests as severe working capital deficits.

This is reflected in Jubilant Flame's excessive current liabilities vastly outstripping assets by nearly two orders of magnitude [F1], highlighting a breakdown typical when capital availability cannot match operational commitments. Without explicit disclosures of project pipelines or investment efforts indicating future capacity expansion ([S2]), it is difficult to envision how Jubilant Flame might resolve this structural mismatch.

Comparing Lack of Core Production Metrics Against Industry Peers

Leading integrated oil & gas companies such as ExxonMobil routinely publish comprehensive data on total production volumes across crude oil and natural gas segments along with realized commodity prices driving revenue recognition. Midstream firms like Kinder Morgan report on pipeline capacity utilization critical for stable fee-based income streams derived from transporting hydrocarbons.

Independent explorers such as Devon Energy also disclose liftings costs per BOE alongside their reserve replacement ratios informing investors about asset base replenishment vital for sustaining future production levels.

Jubilant Flame's silence on these fundamentally informative metrics sets it apart negatively—investors rely heavily on these standardized data points for valuation models focused on cash flow predictability amid commodity price volatility. Their absence introduces informational disadvantages exacerbating uncertainty surrounding ongoing operations.

Growth Outlook Severely Limited by Current Financial Stress

Typical growth drivers in energy involve capital allocation toward expanding reserves via drilling programs responsive to rising global demand and infrastructural investments accommodating increasing throughput capacities. However, Jubilant Flame’s current liquidity profile—with negligible current assets relative to liabilities—and ongoing losses suggests meager capacity to finance growth internally nor apparent access to external funds without dilution or added debt risk [F1]

Given absence of disclosed CapEx expenditures coupled with zero top-line receipts [F1], it appears unlikely that Jubilant Flame is currently undertaking significant project developments which would otherwise signal forward momentum.

Major Risks: Liquidity Shortfall, Market Visibility, Operational Sustainability

Several inherent risks crystallize from Jubilant Flame’s latest disclosures. First and foremost is acute liquidity risk where daily working capital needs cannot be met due to the imbalance between liabilities ($1.46 million) versus assets ($9.7 thousand) yielding a dangerously low current ratio reflected at roughly 0.01 [F1]. This ratio is far below typical healthy thresholds (>1) observed even among smaller energy firms signaling near-term solvency dangers.

Market visibility deficit stems from lack of transparency regarding core operations: no reference to revenues hinders assessment of pricing power; no disclosure around reserves obstructs analysis around long-term sustainability; absence of CapEx undermines insights on reinvestment capability [S1][S2]

Combine these factors with historical debt carrying burdens exceeding $58 million from previous periods—the overall financial strain translates into heightened going concern considerations noted previously by auditors transitioning from KCCW Accountancy Corp citing uncertainties around viability despite no adverse opinions [S10]

Commodity price volatility common across hydrocarbons further compounds risk profile since absent diversified income streams leave Jubilant Flame exposed should recovery efforts fail.

Key Milestones And Metrics To Watch Next

Monitoring future filings for concrete signs of business stabilization will be critical. Key metrics include:

- Emergence of any reported revenue indicating commencement of sales activities,

- Improvement in liquidity ratios suggesting successful recapitalization or cost rationalization,

- Disclosure related to project developments hinting at resumed investment spending,

- Management commentary clarifying strategic direction addressing current distress,

- Changes in auditor remarks reflecting shifts in going concern assessments [S2][S1]. Progress against these markers would serve as positive indicators moving beyond speculative status toward operational normalization. Absent them, uncertainties will persist requiring heightened scrutiny from investors and stakeholders alike.

Financial Profile Discussion: Acute Solvency Concerns Demand Close Monitoring

The company’s financial snapshot paints a dire picture amidst an industry characterized by high upfront capital deployment requirements balanced by subsequent commodity-generated cash flows supporting sustainability [F1]. As of May 31, 2026 latest reporting shows current assets at $9,725 against overwhelming short-term obligations totaling roughly $1.46 million yielding a dangerously low current ratio near 0.01—a level indicative of extreme funding stress unprecedented even by small-cap exploration standards

Historical total debt reportedly stands around $58 million from earlier periods while net debt remains elevated given negligible cash reserves recorded at just over $2,500 as late as November 2023 [F1]. Persisting net losses nearing $63k for recently reported periods compound erosion of equity buffers further weakening financial footing.

Together the weak liquidity profile paired with zero reported revenues portends significant going concern risks escalated by limited disclosure obstructing confidence restoration pathways absent immediate remedial actions or fresh capital infusion discussions noted publicly so far [S2]. Vigilant examination post forthcoming quarters will be essential to judge survival prospects more definitively.

Financial position in context

Current assets of $9725 and current liabilities of $1459548 imply a current ratio near 0.01x for 2026-05-31 [F1]

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments