ONAR Holding Corp Advances AI-Enabled Marketing Platform Amid Liquidity and Integration Challenges

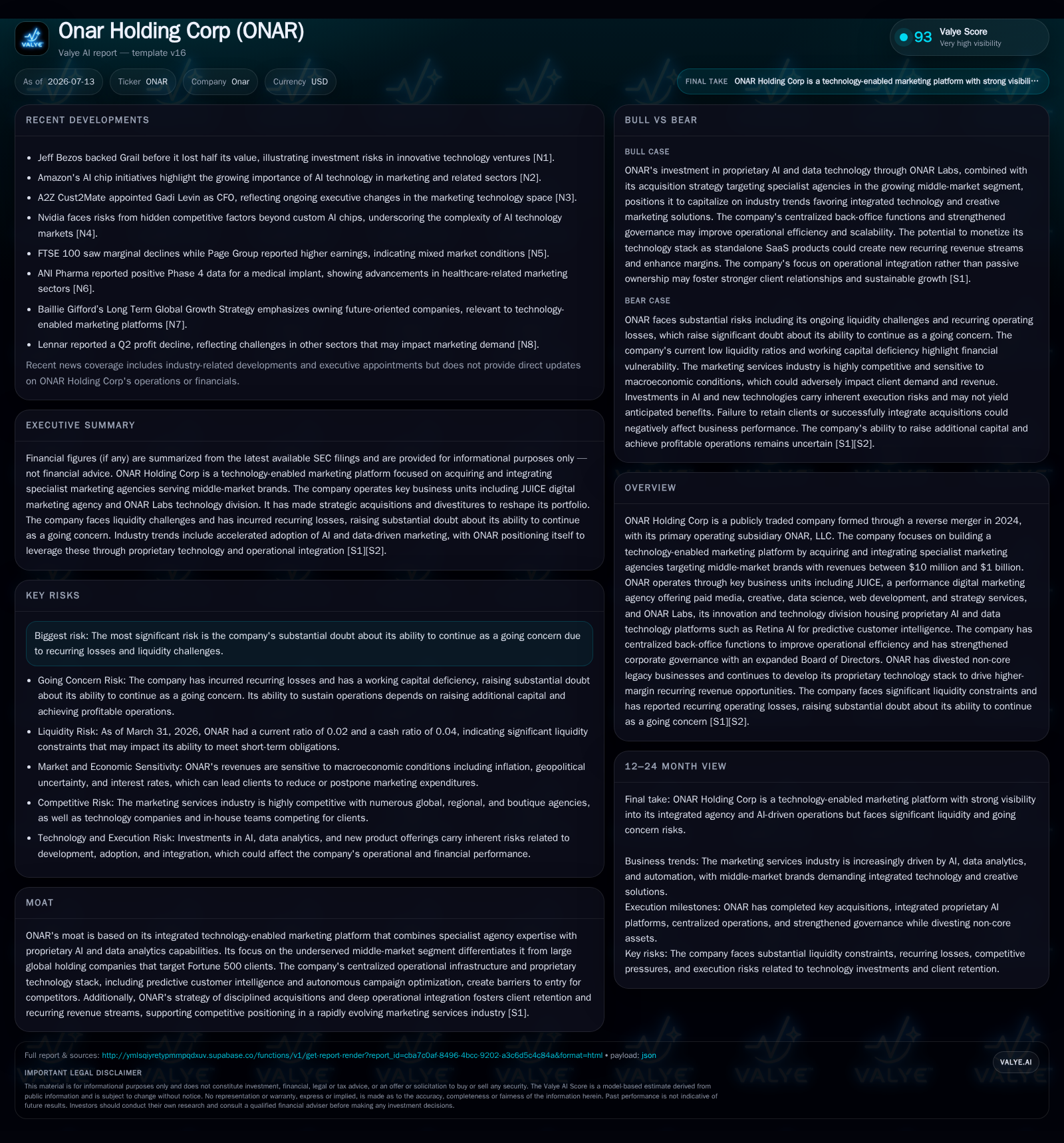

ONAR Holding is reshaping middle-market marketing through acquisitions and proprietary AI, but faces significant financial headwinds.

ONAR Holding Corp continues to build a technology-integrated marketing platform targeting middle-market brands via strategic acquisitions and proprietary AI development. Its key units, including JUICE digital agency and ONAR Labs technology division, enhance service breadth and recurring revenue potential. However, the company carries substantial going concern risks due to recurring operating losses, negative working capital, and a fragile liquidity position. Success hinges on efficient acquisition integration, monetizing its AI platform, and securing additional financing.

Recent Operating Update

ONAR Holding Corporation’s latest quarterly filing dated July 13, 2026 confirms the persistence of significant financial distress, with explicit disclosure of substantial doubt regarding its ability to continue as a going concern due to recurring losses and liquidity gaps [S2][S1]. This follows an earlier June 22 amendment increasing authorized common stock threefold to 3 billion shares—an action typically undertaken by firms anticipating equity raises to shore up balance sheet flexibility [S3]. While the company did not provide detailed Q2 financials in the publicly available excerpt, the strategic intent is clear: access capital markets for growth and survival.

Business Model Analysis

ONAR operates as a technology-enabled marketing platform focusing specifically on specialist marketing agencies serving middle-market brands with annual revenues ranging from $10 million to $1 billion [S1]. These agencies offer digital performance marketing services including paid media campaigns, creative content production, data science capabilities, web development, and marketing strategy consulting.

The company’s flagship operating subsidiary is ONAR LLC, which holds JUICE—a full-service performance digital marketing agency credited with generating over $2.5 billion in client revenues and maintaining average client tenures exceeding three years [S1]. JUICE’s broad offering spans paid digital advertising (e.g., search engine marketing), conversion rate optimization, SEO services, web development projects, creative production workflows, and data-driven campaign management. This integration of performance services addresses middle-market clients who demand enterprise-grade capabilities sans enterprise-level fees or complexity

In parallel, ONAR Labs functions as the innovation engine for the group’s technology stack. Its centerpiece is Retina AI—a predictive customer intelligence platform providing customer lifetime value forecasts, audience segmentation models, and automated campaign optimization through Cortex (real-time analytics backbone) and Agentic Ops (autonomous campaign execution). These tools are designed both to enhance internal agency efficiency and generate higher-margin recurring revenue from SaaS licensing of these proprietary tech products [S1]. Monetization beyond agency uplift involves potential standalone offerings targeted at third-party customers seeking advanced AI-powered marketing intelligence

Revenue primarily stems from client fee-for-service engagements: retainer contracts for ongoing campaign management, project-based fees for discrete initiatives like website builds or creative productions, and media management fees typically linked to paid advertising spend budgets. The push toward SaaS-derived recurring revenues via ONAR Labs’ tech stack is pivotal for margin expansion since software products benefit from high incremental margins compared with labor-intensive agency services.

Centralized back-office operations—for finance, legal compliance, accounting, HR—yield operational consistency across the portfolio agencies while enabling cost control; however, as evidenced by reported negative working capital (current assets $178K vs. liabilities $10.6M yielding a dismal current ratio near 0.02), these efficiencies have yet to resolve fundamental liquidity challenges [F1][S1]

Industry Structure and Competitive Positioning

ONAR occupies the segment between large global advertising conglomerates (WPP, Omnicom) that serve Fortune 500 multinational clients and smaller boutique or regional digital agencies targeting local or niche markets. By concentrating on the growing middle market—which lacks access to scaled enterprise marketing resources but demands sophisticated solutions—the company aims to fill a notable void.

Differentiation arises from its strategy of deep integration combining specialist agencies under one operational umbrella empowered by proprietary AI platforms—a contrast to traditional holding companies that often maintain looser affiliations among subsidiaries without unified technology stacks. This integrated model supports predictable client retention through better data-driven campaign performance insights and operational agility enabled by automation.

However, this space remains fiercely competitive with numerous mid-sized specialist agencies offering comparable digital marketing capabilities. Additionally, large holding companies increasingly invest in AI tools internally or through partnerships. ONAR's moat thus leans heavily on sustaining technology leadership via ONAR Labs platforms and fostering disciplined acquisition integration that preserves client relationships amid portfolio expansion [S1][S7].

Growth Drivers

Key growth drivers reflect secular industry shifts:

- Rising adoption of AI-powered analytics accelerates demand for predictive customer intelligence platforms like Retina AI.

- Migration of marketing budgets toward digital channels bolsters demand for integrated performance marketing services covering media buys through conversion optimization.

- The expanding sophistication of middle-market brands creates fertile opportunity for technology-forward agencies able to deliver enterprise-grade results without premium cost structures.

- Strategic acquisitions are expected to remain central; recent purchases include Juice Labs LLC (September 2025) consolidating multiple agency offerings under JUICE brand alongside the incorporation of Retina AI software to augment technological differentiation [S19][S5].

- Centralizing back-office shared services aims at improving consolidated operating margins by trimming overhead redundancies across acquired entities.

- Monetizing proprietary technology through SaaS licensing can unlock higher recurring revenue percentages relative to traditional fee-for-service agency work.

Risks and Constraints

Despite strategic promise, notable risks cloud ONAR's outlook:

- Liquidity remains precarious; recurring losses totaling nearly $9.3 million in 2025 alongside negative working capital heighten refinancing urgency [F1][S1]. Failure to secure timely additional financing could imperil continued operations.

- Integration risk looms large given recent acquisitions; misalignment could disrupt client service continuity or inflate costs undermining anticipated synergies [S12].

- Market sensitivity exists since discretionary client spends on advertising can retract abruptly during economic downturns or geopolitical uncertainty impacting revenue stability [S1].

- Litigation involving senior secured promissory notes filed by Feinberg Personal Trust poses contingent legal risk though currently considered non-material by management [S10].

- Investment in advanced AI systems incurs technical execution risk including compliance with evolving regulations on generative AI usage; failure or delays here would impair competitive positioning [S26].

- Client retention is critical; any material loss among established accounts with multi-year average tenures would badly impact financial results.

- Pricing pressures from competitors including in-house corporate teams exert margin compression forces.

What To Watch Next

Execution milestones will focus on:

- Successful raising of fresh capital leveraging increased authorized shares illuminating solvency prospects.

- Demonstrable traction in commercializing ONAR Labs technologies with clear contribution toward margin improvement and recurring revenue growth.

- Continued disciplined acquisition activity coupled with evidenced integration success metrics such as retention rates post-acquisition.

- Quarterly operating earnings improving toward break-even or profitability thresholds relieving going concern doubts.

- Resolution progress on debt-related litigation or tax penalty negotiations which could affect balance sheet liabilities.

- Macro environment stabilization supporting middle-market client spend recovery fostering organic revenue growth.

Financial Profile Discussion

Liquidity constraints are pronounced: cash & equivalents amounted to about $444K at year-end 2025 versus current liabilities surpassing $10.6 million as of March 31, 2026—leading to an extremely weak current ratio of approximately 0.02 indicating significant short-term coverage gaps [F1]. Total debt outstanding is approximately $56K as of June 30, 2024, but this is minimal relative to the substantial payables and accrued expenses reflected in the negative working capital position [F1].

Management acknowledges these stresses openly with plans centered on equity/debt raises aligned with accelerating organic top-line growth from acquired businesses alongside efficient cost rationalizations driven by centralized back-office functions [S1][S2]. Equity dilution risk is heightened accordingly given share authorization expansions recently approved [S3].

While operating losses suppress cash flow conversion presently, execution successes in monetizing proprietary SaaS platforms could materially improve future margin profiles by shifting revenue mix away from lower-margin service fees towards scalable software license income streams.

This analysis integrates public regulatory disclosures up through the July 13 quarter filing along with relevant SEC filings as cited without extrapolation beyond provided evidence. It aims to provide an informed perspective on ONAR Holding Corp's strategic positioning within its evolving industry context while highlighting critical operational risks stemming principally from financial health challenges inherent in early-stage consolidation models combining agency expertise with cutting-edge marketing technologies.

The author holds no investment positions nor provides investment advice herein.

Financial position in context

Current assets of $178,550 and current liabilities of $10,616,250 imply a current ratio near 0.02x for 2026-03-31 [F1]

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments