XFLH Capital Corp’s SPAC Lifecycle Begins with $100M IPO and Strong Liquidity

Newly public SPAC XFLH Capital Corp holds $100 million proceeds in trust, setting stage for de-SPAC transaction while facing typical sector execution risks.

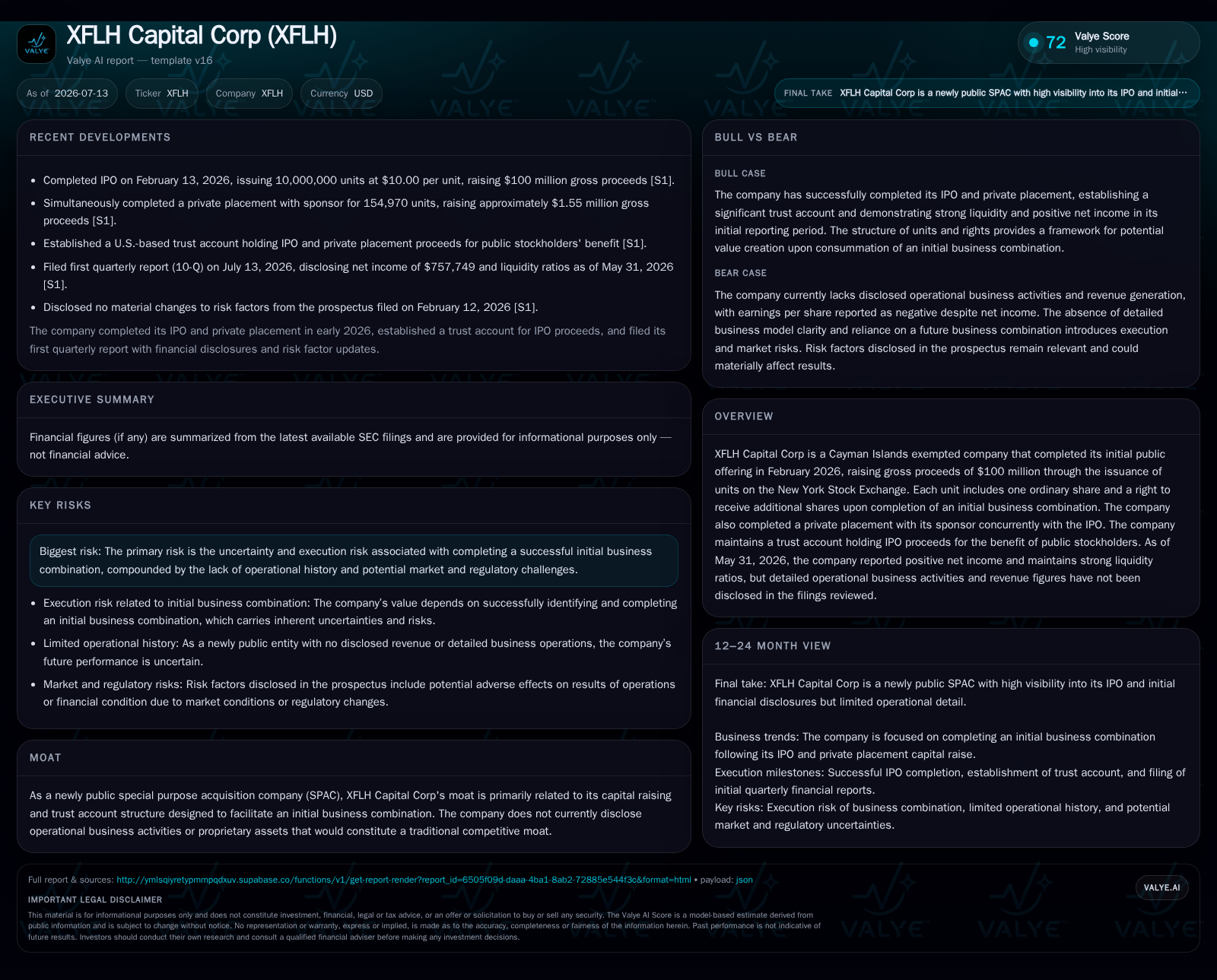

XFLH Capital Corp completed its initial public offering (IPO) in February 2026, raising $100 million through units on the NYSE. The company’s capital is held in a trust account pending an initial business combination (de-SPAC transaction), consistent with standard SPAC structures. Recent quarterly filings confirm no material changes to disclosed risks and highlight strong liquidity and positive net income derived primarily from trust account interest. As a pure acquisition vehicle, XFLH’s operational and financial prospects hinge on successful deal execution within a mandated timeframe amid common SPAC lifecycle challenges.

Recent Operating Update: Launching the SPAC Journey

XFLH Capital Corp officially entered the public markets with its initial public offering (IPO) consummated on February 13, 2026, raising gross proceeds of $100 million by selling 10 million units at $10 each [S4][S6][S13]. Each unit comprises one ordinary share plus a right to receive an additional fraction of a share upon completing an initial business combination (the so-called "Right") [S6]. This structure aligns with standard SPAC unit offerings, designed to attract investors combining equity upside with future de-SPAC warrants or rights.

Concurrently with the IPO, XFLH's sponsor conducted a private placement of approximately 155K units at the same price, contributing around $1.55 million to the total raise [S5][S13]. These "Sponsor Private Placement Units" remain restricted from transfer until after deal closure to promote alignment between sponsors and public shareholders.

Critically, the company deposited the net IPO proceeds—$100 million plus related private placement funds less underwriting fees—in a U.S.-based trust account managed by Continental Stock Transfer & Trust Company [S5]. The trust-account mechanism safeguards investor funds from premature use until specific liquidity events occur: closing the initial business combination or mandated redemption rights triggered by shareholder votes or failure to transact within the time horizon (typically 15 months post-IPO) [S5].

Shortly after listing, holders were enabled to separate their units into standalone ordinary shares and rights to trade individually on the New York Stock Exchange starting March 9, 2026 [S9]. This practice reflects established market customs facilitating trading flexibility and clearer valuation segmentation between equity shares and attachable rights.

XFLH remains in the pre-combination phase as of its July 13, 2026 quarterly report filing [S2]. There have been no material changes to disclosed risk factors since its February prospectus filing [S14], underscoring operational stability typical of SPAC shells prior to acquisitions. Importantly, reported net income is positive at approximately $758K as of May 31, largely attributable to interest income earned on cash held in the trust account [F1]. Operating income remains negative primarily due to administrative expenses but is manageable given the purpose-built capital structure.

Business Model Specificity: Pure Capital Vehicle for De-SPAC

XFLH operates under the archetypal SPAC business model: it raises capital upfront exclusively through an IPO comprising units (ordinary shares combined with rights/warrants) intended to facilitate an eventual initial business combination (also called de-SPAC transaction) with a private operating company. Until that combination occurs or time runs out, XFLH generates minimal revenue aside from interest on trust account holdings.

Monetization mechanics involve:

- Capital Raise: Proceeds from public unit sales form the principal asset base.

- Trust Account Safeguards: Nearly all IPO proceeds are segregated in low-risk instruments under trustee custody; these funds are earmarked exclusively for consummating the business combination or returned pro rata upon redemption.

- Sponsor Promote: The Sponsor invests via private placement units pre-IPO but faces transfer restrictions until closing; this aligns incentives but typically dilutes post-deal economics when warrants convert.

- Redemption Rights: Public shareholders may redeem their ordinary shares at IPO price before deal closing if dissatisfied with proposed terms or timing—this creates uncertainty over deal funding availability.

This pure capital vehicle role means XFLH’s success relies heavily on identifying high-quality private targets seeking expedited access to public equity markets versus traditional IPOs. The company does not produce products or services pre-combination nor hold proprietary technology or assets influencing traditional competitive positioning.

Industry Structure and Competitive Positioning

Within the broader SPAC sector—a class populated by vehicles like Pershing Square Tontine Holdings (PSTH), Churchill Capital Corp series, and Social Capital Hedosophia—XFLH is positioned as an emerging player initiating operations in early 2026. Its $100 million IPO size situates it towards the smaller end compared to billion-dollar-plus flagship SPACs frequently sponsored by marquee investors.

Close observation of proxy disclosures accompanying deal announcements alongside redemption election behaviors during tender offers will be critical indicators of risk calibration going forward.

What To Watch Next: Milestones Anchoring Market Sentiment

Primary upcoming milestones defining XFLH’s progression include:

- Announcement of Initial Business Combination Target: The declaration triggers detailed due diligence assessments by shareholders directly impacting vote outcomes.

- Shareholder Vote Outcomes on Deal Approval: Affirmative votes unlock release of trust account funds enabling transaction funding; high rejection rates may lead to liquidation scenarios.

- Redemption Rates During Tender Offer Periods: High redemption percentages may require supplemental financing steps impacting dilution dynamics.

- Regulatory Filings Progression Post-Signing: Timely SEC filings adhering to schedule reduce uncertainty premiums baked into unit/share prices.

- Financial Updates Tracking Liquidity Utilization: Quarterly reports monitoring administrative cost impacts and trust-account yield variations inform cash runway estimation pre-combination completion [F1][S2]

Following these indicators provides tangible visibility into execution quality within typical SPAC life cycle frameworks where uncertainty dominates absent known target disclosures.

Financial Profile Discussion

Financial position in context

As of 2026-05-31, companyfacts shows $246,742 in cash and equivalents and zero total debt [F1]. The same snapshot implies net debt of approximately negative $246,742, reflecting a net cash position [F1]. Current assets of $446,844 and current liabilities of $31,207 imply a current ratio near 14.32x as of May 31, 2026 [F1].

Disclaimer

This analysis does not constitute investment advice but aims to provide an informed perspective based on publicly available regulatory filings and industry-standard knowledge regarding special purpose acquisition companies. Readers should corroborate facts independently before forming opinions related to transactional developments or shareholdings.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments