Enanta Pharmaceuticals Struggles with Revenue Growth Amid High R&D Investment and Patent Litigation

Enanta's latest quarter highlights ongoing losses driven by heavy clinical-stage antiviral development and litigation costs.

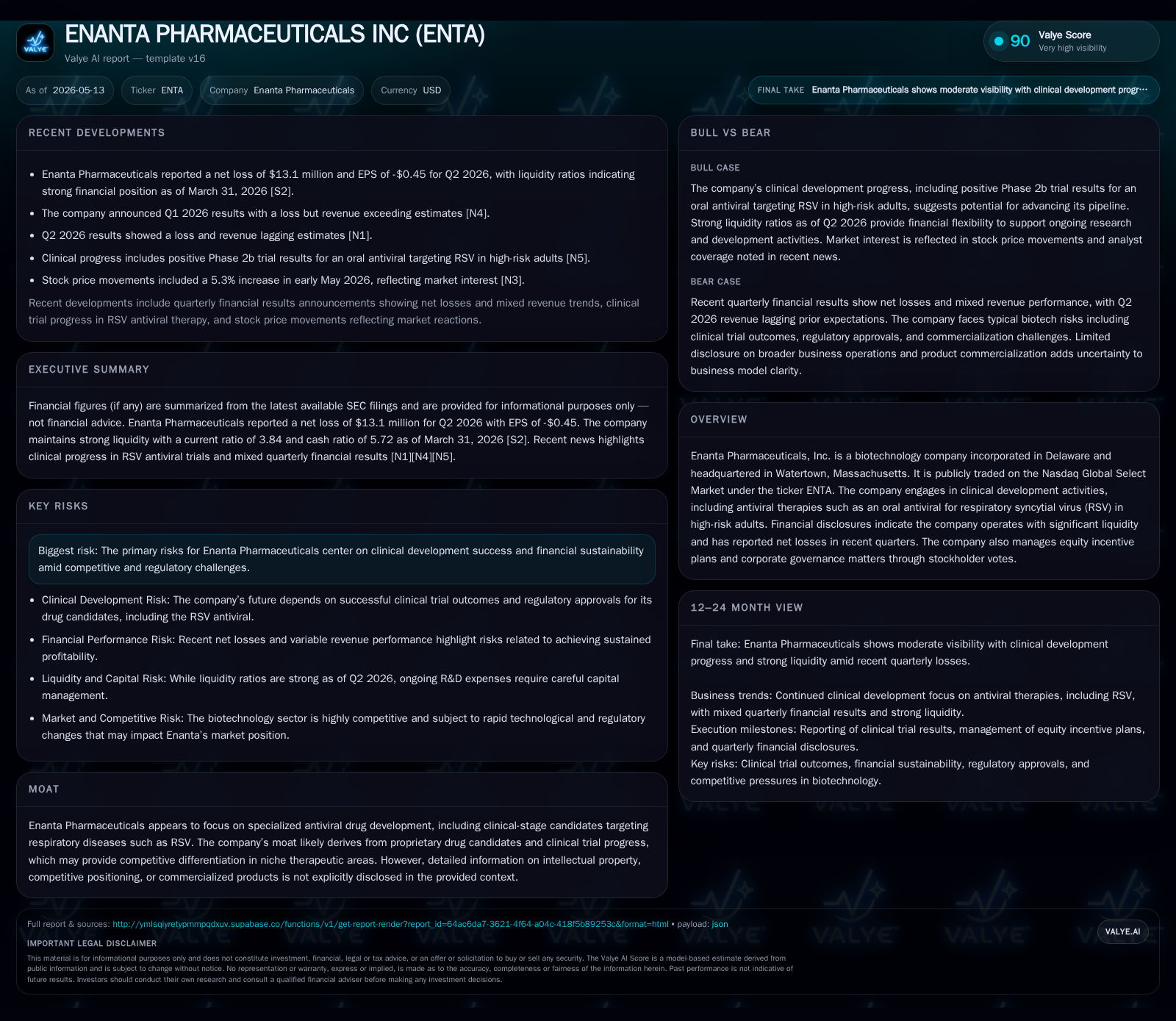

In its 2026 Q1 filing, Enanta Pharmaceuticals reported continued net losses, underscoring the challenges of advancing its antiviral pipeline with limited current revenue. The company’s business model centers on clinical-stage proprietary antiviral drug development, with a focus on respiratory diseases such as RSV. Competitive positioning depends heavily on successful trial outcomes and intellectual property enforcement, notably ongoing patent litigation over Pfizer's Paxlovid. Structural growth drivers include expanding indications in respiratory viruses and commercialization of clinical candidates, but risks remain around clinical success, financial burn rate, and regulatory hurdles. Monitoring near-term trial data readouts and litigation outcomes will be critical for assessing Enanta's path to sustainable growth.

Recent Operating Update

Enanta Pharmaceuticals’ latest quarterly filing for Q1 2026 (ended March 31) reflects ongoing operational challenges typical of a clinical-stage biotech focused heavily on antiviral drug development [S2]. The company announced results characterized by net losses continuing from prior periods, reflecting sizable spending on clinical trials without significant revenue inflows. The associated press release dated May 11, 2026, confirms weaker-than-expected revenue performance against estimates while highlighting sustained investments in R&D programs [S3][N1]. Liquidity remains supported by $34.9 million in cash and equivalents at quarter-end with minimal debt obligations, indicating prudent balance sheet management despite financial losses [F1].

Notably, Enanta continues active legal pursuits centered on patent infringement claims involving Pfizer’s Paxlovid antiviral (nirmatrelvir tablets), challenging manufacturing and commercial use based on their intellectual property rights [S6]. Oral arguments were scheduled before the Federal Circuit in May 2026, making this a key event that could influence future licensing revenues or defensive positioning.

Business Model

Enanta primarily operates as a biotechnology developer specializing in small-molecule antivirals targeting high-risk populations affected by respiratory viruses such as Respiratory Syncytial Virus (RSV). Its approach involves discovery through proprietary chemistry techniques followed by preclinical studies and phased clinical trials designed to prove safety and efficacy necessary for regulatory approval and commercialization [S1].

Currently, Enanta does not possess marketed drugs generating significant commercial revenue; instead, its model relies on successful progression of pipeline assets through clinical phases to attract partnership deals or launch products independently eventually. This yields a revenue profile highly dependent on milestone payments from collaborators (if any), grants or government funding, and ultimate drug sales post-approval.

Product quality is anchored in targeted antivirals with oral administration routes which are favorable for outpatient treatment paradigms targeting viral respiratory infections. However, without commercial products yet available broadly in the market, the company faces typical biotech risks associated with dependency on trial success probabilities.

Industry Structure and Competitive Position

Within the pharmaceutical value chain, Enanta situates itself upstream in drug discovery and early-to-mid stage development. Unlike large pharmaceutical firms engaged in global commercialization with extensive marketing infrastructure, Enanta’s competitiveness derives principally from innovation within niche antiviral chemistries and IP rights coverage.

The respiratory antiviral space is competitive but fragmented. Larger players like Pfizer dominate with products such as Paxlovid for COVID-19 treatment while various firms pursue RSV antivirals due to growing recognition of its severe impact on elderly and immunocompromised patients. Enanta’s ability to carve out positions depends heavily on successful clinical differentiation and robust patent protections.

The pending patent litigation against Pfizer signals an important competitive defense aimed at protecting Enanta's intellectual property assets tied to COVID-19 therapeutics. This action also illustrates their strategy to monetize IP either via licensing or settlements if commercialized competing products gain market traction.

Growth Drivers

Growth potential for Enanta emanates mainly from several vectors:

- Advancing Clinical Pipeline: Progression of lead oral antiviral candidates through pivotal trials can unlock regulatory approvals essential for market entry and revenue generation.

- Broader Antiviral Indications: Expanding indications beyond initial target diseases such as RSV to other respiratory viral infections creates larger addressable markets.

- Intellectual Property Enforcement: Favorable outcomes in ongoing patent litigation may yield licensing revenues or enhance bargaining power for co-development partnerships.

- Strategic Collaborations: Deals with pharmaceutical companies could provide non-dilutive funding via milestone payments tied to developmental progress.

KPIs to watch include trial enrollment rates, interim efficacy/safety data releases, FDA submissions/approvals timelines, backlog or agreement announcements from collaborators.

Risks / Watchpoints / Growth Constraints

Several significant risks loom over Enanta's prospects:

- Clinical Development Failure: The inherent uncertainties in trial results present a risk that late-stage failures could stall growth entirely.

- Financial Sustainability: Ongoing operating losses necessitate effective cash management; lack of near-term revenue streams places pressure on working capital.

- Regulatory Hurdles: Delays or rejections from health authorities can extend timelines or force modifications increasing costs.

- Competitive Threats: Entrants with superior efficacy or wider distribution networks may capture disease segments first.

- Litigation Outcomes: An unfavorable ruling or protracted patent battle could diminish expected returns from COVID-19 antiviral IP enforcement efforts.

Monitoring these factors is crucial to understanding Enanta's long-term viability.

What To Watch Next

Key upcoming events that will serve as barometers for execution include:

- Oral arguments outcome related to Pfizer patent appeal scheduled around May 11, 2026 [S6]

- Progress reports or interim data readouts from ongoing Phase trials targeting RSV or other viruses [S2]

- Potential announcements regarding new collaborations or licensing agreements following clinical milestones [N1]

- Continuing management guidance updates embedded within quarterly financial disclosures for adjustments reflecting developmental pacing or fund raising needs [S2]

- Investor sentiment shifts around equity incentive plan expansions approved earlier in 2026 signaling efforts to retain scientific leadership talent amid tough R&D cycles [S10]

Together these milestones will inform trajectory toward eventual product commercialization or further investor scrutiny.

Financial Profile

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Cash & equivalents | $35mm | |

| 2026-03-31 | ||

| Current assets | $178mm | |

| 2026-03-31 | ||

| Current liabilities | $46mm | |

| 2026-03-31 | ||

| Current ratio | 3.84x | |

| 2026-03-31 |

Source: SEC companyfacts cache [F1].

Enanta’s financial posture as of Q1 2026 combines manageable liquidity amid negative earnings: cash & equivalents total approximately $34.9 million supporting operational runway with minimal debt reported around $2 million [F1]. Current ratio stands robust at about 3.84x indicating solid near-term solvency against current liabilities roughly at $46.4 million [F1]. Nevertheless, continual R&D expense drives net losses persistently affecting operating income.

This pattern is emblematic of biopharmaceutical enterprises prioritizing heavy upfront investment over immediate profitability until pipeline maturation enables revenue conversion. While financially strained relative to commercial peers signed notable partnerships could ease capital intensity downstream.

Source: Latest Quarterly Filing and Companyfacts [S2], [F1]

This analysis synthesizes filings through May 2026 to provide an informed view of Enanta Pharmaceuticals’ operational dynamics within its specialized niche. The company exemplifies a classic high-risk/high-reward biotech poised at a critical juncture between heavy R&D commitment and nascent commercial potential shaped by intellectual property litigation outcomes.

Disclaimer: This report is for informational purposes only and does not constitute investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments