Evolution Petroleum: Navigating Dividend Consistency Amid Break-Even Earnings and Operational Constraints

A nuanced exploration of Evolution Petroleum’s dividend-focused ownership model within a non-operated asset framework facing liquidity and reserve pressures.

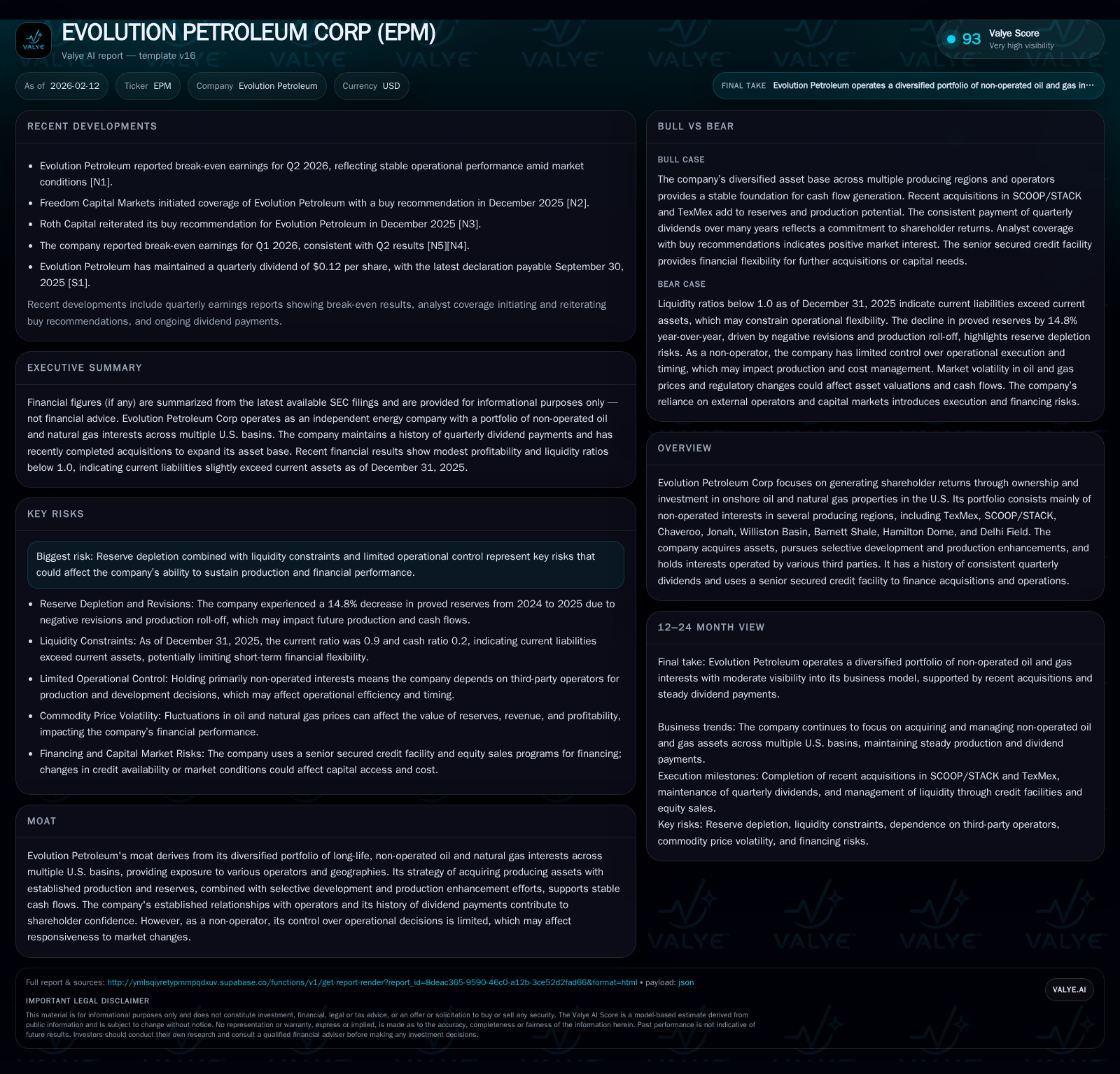

Evolution Petroleum stands out by maintaining a robust history of quarterly dividends despite recent break-even earnings reports, reflecting a business rooted in diversified, non-operated U.S. oil and gas interests. This unique structure offers stability from its broad geographic portfolio while simultaneously limiting its ability to influence daily operations. The company is managing tight liquidity conditions, reflected in a sub-1 current ratio and reliance on secured credit facilities. Growth prospects hinge on strategic asset acquisitions and enhancement efforts, yet the looming risks of reserve depletion and limited operational control shape an intricate risk-reward profile.

Evolution Petroleum: Owner of Diverse Yet Non-Operated U.S. Oil & Gas Interests

At the heart of Evolution Petroleum Corp’s business model lies an intriguing paradox: it owns substantial interests in several producing onshore oil and natural gas properties across the United States without operating these assets directly. Instead, Evolution holds non-operated stakes spread across multiple basins such as TexMex, SCOOP/STACK, Chaveroo, Jonah Field, Williston Basin, Barnett Shale, Hamilton Dome, and Delhi Field [valye_report_excerpt][S1]. This broad geographic footprint tempers the risks inherent in any individual reservoir or operator relationship.

However, owning without operating means Evolution defers day-to-day field management decisions to partners who control drilling, production techniques, and capital deployment. The result is a portfolio whose performance partly rests on others’ operational choices — a double-edged sword that provides steady revenue streams but limits Evolution’s tactical agility.

Geographic breadth reduces exposure to localized declines or operator-specific challenges but attenuates responsiveness to rapid market shifts or technology-driven enhancements. This framework frames much of the company’s financial dynamics.

Behind the Headlines: Understanding the Break-Even Earnings Report

In its most recent quarterly report ending December 31, 2025, Evolution Petroleum posted earnings essentially at break-even—a status that initially rings alarm bells for an upstream energy firm [N1][S2][F1]. Revenues remain modest (in line with prior quarters), but net income compressed to approximately $1.06 million on revenues around $13.7 million highlights slim margins amid cost pressures.

This break-even reflects both static production volumes—as assets mature—and market price fluctuations that eclipse the benefits from incremental operational efficiencies. Notably though, cash flows have remained stable enough to support core obligations and ongoing dividends.

It is important to differentiate break-even accounting profits from cash performance here. While earnings stagnate due to depreciation charges and non-cash expenses inherent in asset-heavy portfolios, cash flows—bolstered by established mineral positions—remain resilient enough to uphold shareholder payouts. Yet, this equilibrium signals limits to earnings growth absent either acquisitions or significant operational improvements upstream.

Dividend Durability: A Legacy of Consistency in Quarterly Payouts

Since launching its cash dividend program in December 2013, Evolution Petroleum has paid out 47 consecutive quarters of dividends—currently fixed at $0.12 per share each quarter [S1]. This consistency is remarkable against the backdrop of volatile commodity prices and often uneven earnings reports.

The dividend policy signals a corporate commitment to returning capital steadily to investors despite fluctuating internal metrics. It suggests an emphasis on shareholder confidence as a strategic priority. Dividends provide a reliable income stream that can attract yield-focused investors looking beyond immediate earnings volatility.

However, maintaining dividends amid earnings constraints requires careful balancing; any sustained deterioration in liquidity or reserve base would challenge this continuity. The board explicitly retains discretion over future payouts based on evolving financial health and capital requirements—a prudent guardrail ensuring flexibility should conditions tighten further.

Financial Balancing Act: Cash, Credit, and Liquidity Constraints

Examining Evolution’s balance sheet reveals underlying tensions beneath apparent stability. As of December 31, 2025, current assets stood at roughly $17.16 million while current liabilities slightly exceeded that at $19.13 million—producing a current ratio near 0.9 [F1].

Such below-par short-term liquidity means the company relies significantly on its senior secured credit facility to finance working capital needs and acquisitions [valye_report_excerpt][S2]. Cash and equivalents—about $3.76 million—represent only part of this cushion.

This precarious positioning requires vigilant cash flow management and could limit flexibility during downturns or unexpected expenses. At the same time, leveraging credit allows Evolution to pursue selective acquisitions without immediate equity dilution but adds debt servicing obligations reducing net income further.

Thus, liquidity constraint is not merely theoretical; it could materially impact strategic options if market headwinds or operational hiccups arise unexpectedly.

The Moat in Detail: Portfolio Diversification vs. Operational Limitations

Evolution’s competitive advantage—or moat—is principally embedded in its diversified portfolio spanning multiple productive U.S. shale plays and conventional basins [valye_report_excerpt]. This breadth mitigates basin-specific risk factors such as regulatory shifts or geology-driven performance swings.

Yet this moat is unconventional; it arises not from direct operational mastery but from investment diversity coupled with prudent acquisition timing targeting mature properties with proven reserves. Such assets typically exhibit more predictable cash generation compared to early-stage drilling plays.

Operational control being surrendered to third-party operators means Evolution cannot unilaterally implement cost-cutting measures or technology upgrades if partners are slow or unwilling—a clear limitation when rapid adaptation becomes necessary.

While diversification provides revenue stability—a tried-and-true buffer—it also blunts responsiveness when market conditions rapidly evolve thus tempering upside potential.

Risks on the Horizon: Reserve Depletion and Limited Control

A looming risk for Evolution arises from reserve depletion inherent in mature producing fields under non-operated ownership [valye_report_excerpt][S2]. Without direct control over enhanced recovery techniques or accelerated development programs tailored aggressively toward reserve replacement, production volumes naturally gravitate downward over time unless offset by acquisitions.

Liquidity constraints compound this risk by restricting capital available for opportunistic investments into life-extension projects or bolt-on assets aimed at replenishing reserves.

Furthermore, reliance on operators imposes uncontrollable elements—partner priorities may diverge; cost structures may rise beyond optimal levels; technological upgrades may lag industry leaders—all negatively impacting Evolution’s realized returns.

These factors underscore structural vulnerabilities embedded in Evolution’s business model requiring continuous vigilance to sustain production longevity and financial health.

Growth Through Selective Asset Acquisitions and Enhancements

Despite these headwinds, Evolution pursues growth through deliberate acquisition strategies focused on accretive producing assets—the aim being acquisition-driven production replacements coupled with selective development initiatives undertaken by operators where possible [valye_report_excerpt][S1].

Rather than aggressive exploration or large-scale field development—which demand substantial capital outlays—Evolution opts for measured additions that complement its existing portfolio quality and scale. This conservative approach harmonizes with liquidity realities while trying to arrest reserve decline trends.

Selective enhancements might include participating marginally in infill drilling programs or secondary recovery techniques championed by operators confident in field economics.

Such disciplined asset management helps maintain cash production levels within manageable capex envelopes preserving dividend capacity amidst earnings pressure.

Shareholder Structure and Equity Incentive Plans: Motivations and Implications

As outlined in recent filings, approximately 34.3 million shares are outstanding distributed among roughly 220 registered shareholders as of mid-2025 [S1]. This shareholder concentration denotes a relatively tight ownership base typical for smaller-cap energy firms emphasizing specialized dividend models.

Management alignment is fostered through equity incentive plans permitting issuance of up to 5.7 million shares under long-dated Amended and Restated Equity Incentive Plan provisions extending through 2034 [S1]. Notably about 2.5 million shares remain available for future grants according to disclosures.

These incentives are designed to motivate executive decisions aligned with sustaining shareholder returns including prudent capital allocation decision-making critical given constrained earnings environment.

Nevertheless, incremental share issuances tied to incentive awards pose modest dilution risks over time—a factor warranting monitoring if share-based compensation expands amid capital scarcity or acquisition funding needs.

Outlook: Navigating Market Volatility Without Operational Command

Looking ahead, Evolution Petroleum faces a complex landscape defined by its steadfast dividend legacy juxtaposed against margins pressured near break-even levels amid tight liquidity conditions [valye_report_excerpt][N1][S2].

Its defending strength lies in diversified holdings that afford resilience even when operational levers are not directly controlled internally—a rare balance between ownership stability and managerial detachment uncommon among traditional exploration & production companies.

Yet an absence of direct operator control limits rapid adaptations necessary in harsh market downturns or accelerating technological revolutions reshaping upstream efficiency standards across the sector.

Continued success will depend heavily on disciplined acquisition activity targeting stable producing assets alongside maintaining stakeholder trust via consistent dividends while navigating inevitable production declines inherent in maturing fields.

Evolution represents an instructive case study in deriving value through “ownership without operation”—a nuanced approach that requires constant calibration between financial discipline, partner collaboration,and market realities.

This analysis is provided solely for informational purposes based on publicly available data as of the stated dates without any recommendation for investment action.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments