ESSENTIAL PROPERTIES REALTY TRUST: Middle-Market Net Lease Niche Fuels Portfolio Expansion and Resilient Cashflows

Essential Properties Realty Trust (EPRT) leverages a granular, diversified portfolio of net leased single-tenant assets focused on middle-market service tenants to generate stable growth and income.

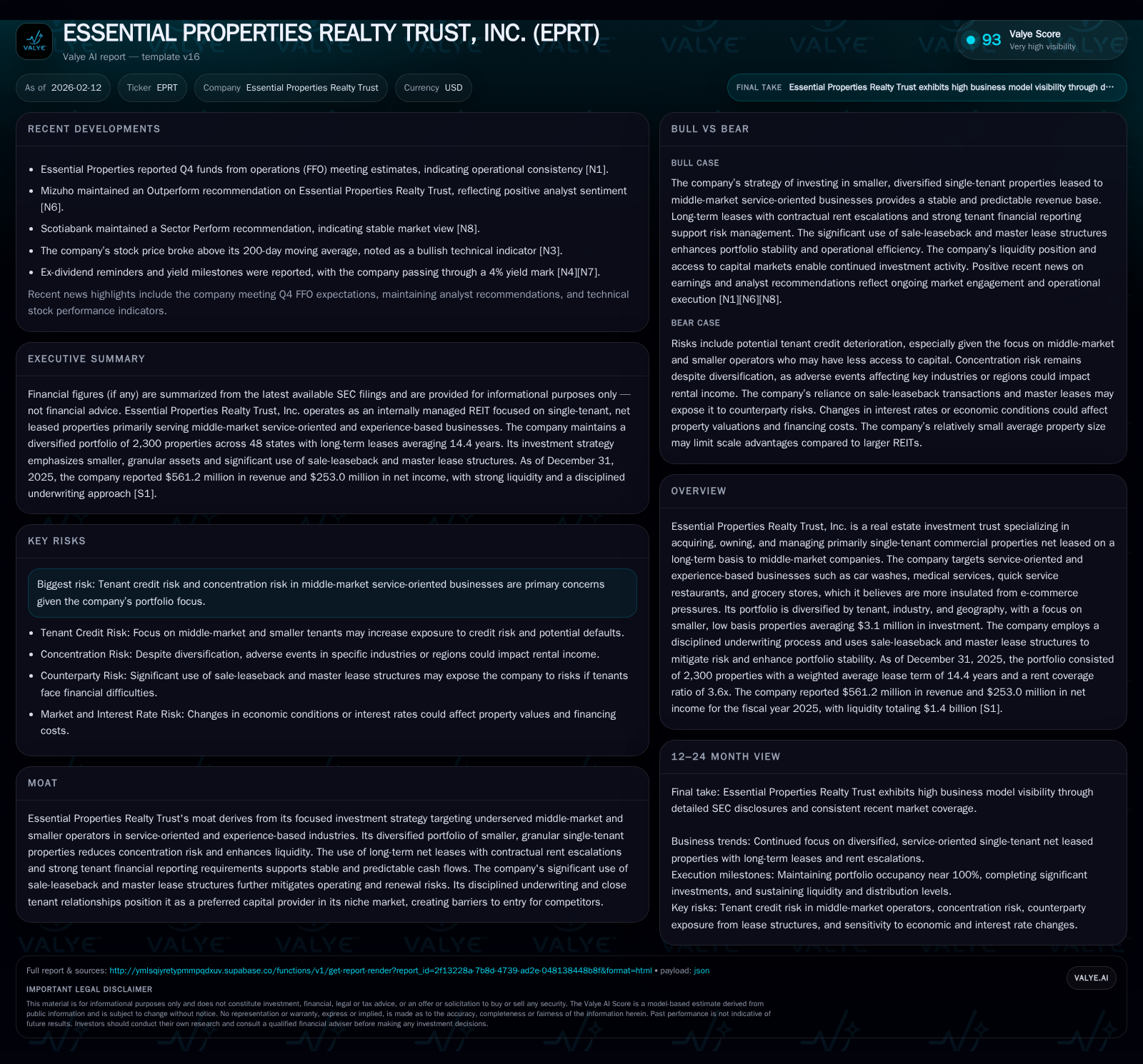

ESSENTIAL PROPERTIES REALTY TRUST, INC. specializes in acquiring and managing single-tenant net lease properties leased primarily to middle-market operators in service-oriented and experiential sectors. Its portfolio—spanning 2,300 properties with a weighted average lease term exceeding 14 years—benefits from high occupancy, significant sale-leaseback transactions, and strong rent escalations that support predictable cash flows. Despite inherent tenant credit risks in the middle market, EPRT’s disciplined underwriting and diversification across hundreds of tenants and brands mitigate concentration risks, underpinning steady financial performance amid broader market volatility.

Niche Focus: Middle-Market Tenants as a Moat

Essential Properties Realty Trust has carved a distinctive competitive position by focusing its investment strategy on single-tenant commercial properties leased to middle-market companies operating in service-oriented and experience-based sectors. According to the company’s regulatory disclosures [S1], approximately 91.5% of EPRT’s annualized base rent comes from such businesses including car washes, medical offices, quick service restaurants, grocery stores, and automotive services—industries generally perceived as more insulated from the structural headwinds posed by e-commerce. This strategic targeting creates a moat by concentrating on tenants whose physical locations are essential to their operations and customer interactions.

Unlike typical retail-focused REITs vulnerable to online retail displacement, EPRT's tenants perform services or experiences less susceptible to digital substitution. The nuanced focus on middle-market operators — smaller companies typically underserved by large institutional capital providers — enables EPRT to establish close tenant relationships supported by disciplined underwriting and extensive unit-level financial reporting rights (covering 99.2% of annualized base rent), enhancing credit visibility [valye_report_excerpt]. This combination erects barriers for competitors who lack the scale or expertise to penetrate this niche efficiently.

Diversification across more than 659 distinct tenant concepts further fortifies this moat; no single tenant contributes over 3.4% of revenues while the company's policy strives for less than 5% from any one tenant long term [S1]. By mitigating concentration risks along tenant and industry dimensions EPRT enhances portfolio resilience against isolated downturns.

Portfolio Dynamics: Growth and Granularity Driving Stability

EPRT’s investment approach favors a granular assembly of predominantly “small-box” single-tenant properties with an average investment around $3.1 million per asset as of December 2025 [S1]. This contrasts with REIT peers that may concentrate holdings in fewer but larger commercial sites. The practical outcome is a highly diversified portfolio now totaling approximately 2,300 properties scattered across 48 states — up from about 1,947 assets the prior year — supporting robust net operating income expansion by diluting idiosyncratic property-level risks [F1][S1].

The portfolio exhibits exemplary occupancy at roughly 99.7%, reflecting sustained demand for service-oriented locations fitting into local economies’ essential business fabric. Such near-full utilization coupled with geographic breadth limits vulnerability to regional economic shocks or localized disruptions.

The diversified composition spans industries including healthcare/medical offices, entertainment venue spaces, education facilities, quick service restaurants, convenience stores, casual dining venues—and other essential service providers—enhancing cash flow predictability through economic cycles.

The Lease Landscape: Long-Term Contracts and Escalations

A defining characteristic bolstering EPRT’s financial stability is its portfolio’s weighted average lease term (WALT) of approximately 14.4 years based on annualized base rent [S1]. This extended duration embeds secure horizons for rental income streams far beyond typical retail leases which frequently cluster under a decade.

Complementing long duration are embedded contractual base rent escalations averaging about 1.8% annually across nearly all leases (97.9%), fostering growth in rent rolls even absent new acquisitions or re-leasing activities [S1]. Additionally, the portfolio benefits from a strong weighted average rent coverage ratio near 3.6x—a metric expressing tenants’ EBITDA relative to their rental obligations—which indicates healthy underlying tenant cash flows versus rental outlays.

Collectively these elements underpin stable top-line revenue generation accompanied by controllable volatility.

Strategic Use of Sale-Leaseback and Master Leases

A notable facet of EPRT’s acquisition cadence involves its predominant use of sale-leaseback transactions wherein middle-market businesses divest real estate ownership while concurrently leasing back their operating facilities under long-term net lease agreements [S1]. During fiscal year 2025 approximately 95% of new investments were executed via sale-leasebacks—a method that simultaneously delivers transaction volume while aligning incentives between landlord and occupier.

Master leases form another cornerstone; these embody about two-thirds (66.8%) of EPRT’s annualized base rent [S1]. Master leasing structures consolidate multiple properties under umbrella agreements with single corporate tenants or operating entities facilitating administrative efficiency and reducing exposure to operational fragmentation. This format also lessens renewal risk as master lessees have expanded footprint responsibility permitting internal reallocation without disrupting EPRT’s overall cash flow.

Such transaction types strengthen tenant relationships and foster income stability rare among conventional net lease REITs reliant heavily on triple-net individual leases.

Financial Performance Deep Dive: Revenue, Expenses, and Margins

Fiscal year 2025 brought pronounced financial growth reflecting successful execution of EPRT’s expansion strategy against a backdrop of moderately rising interest rates and inflationary cost pressures [S1][F1]. Rental revenue surged almost 24%, reaching $527.5 million from $425.7 million the previous year driven chiefly by property acquisitions swelling the investment base from $5.2 billion to $6.2 billion.

Interest income stemming primarily from loans receivable also expanded by more than $8 million year-over-year owing to higher loan balances maintained pursuant to direct financing arrangements.

Operating expenses rose correspondingly with scale; general administrative costs climbed approximately 16% largely attributable to salary inflation and augmented professional fees while property-related expenses increased over fifty percent propelled by additional reimbursable taxes and maintenance demands linked to larger asset footprint.

Depreciation expenses marked a proportional increase consistent with asset additions totaling roughly $153 million in FY25.

Importantly impairment charges on real estate decreased modestly from prior periods indicating stable asset valuations while provision for credit losses dipped marginally highlighting prudent credit evaluation mechanisms.

On the bottom line net income grew near twenty-five percent hitting just over $253 million despite interest expense inflation (+37.6%) stemming from heightened borrowing deployed for acquisitions [S1][N1][N2]. This dynamic underscores how yield accretive growth can balance financing costs when underpinned by durable rental income streams.

Risk Architecture: Tenant Credit, Concentration, and Mitigation

While EPRT meticulously diversifies tenant bases and insists on rigorous financial oversight including periodic unit-level reporting for virtually all leases [S1], its core reliance on middle-market tenants inevitably introduces elevated credit risk relative to blue-chip anchor tenants prevalent among some peer REITs [valye_report_excerpt]. These smaller operators often have less robust balance sheets rendering cash flows more sensitive to economic downturns or sector-specific stressors.

The internal risk controls revolve around several facets: limiting individual tenant exposure to below ~5% of annualized base rent; avoiding excessive concentration in any single property (>1% target); leveraging master leases which allow redistribution risk management; maintaining rent coverage multiples that provide adequate cushion; employing disciplined underwriting standards factoring thorough tenant due diligence; continuously monitoring loan loss reserves which trended slightly downward recently [S2].

This layered approach does not eliminate risk but attempts to structurally minimize downside shocks thus preserving overall cash flow integrity despite operating within more volatile end-markets.

Comparative Context: Where EPRT Stands Among REIT Peers

Against larger net lease REIT peers such as Realty Income (ticker O), which operate portfolios focused on larger box retail or industrial assets/tenants with arguably broader capitalization profiles [N3][N5], EPRT occupies a distinct tactical niche emphasizing sheer number of smaller discrete assets labeled as “small-box” properties averaging just over $3 million per unit [S1].

This concentration on middle-market franchises offers potential agility advantages allowing swift portfolio scaling via frequent sale-leaseback transactions but could pose challenges related to integration complexity, bid discipline enforcement and managing widespread asset dispersion.

Technical trading signals recently hinted investor recognition of this differentiated model with Essential Properties’ shares breaking above their pivotal 200-day moving average—a bullish indicator in technical analysis parlance—suggesting growing market acceptance of their niche approach [N4].

Capital Structure & Debt Profile Insights

EPRT’s funding for accelerated growth depends heavily on debt financing which experienced marked increases during FY25 culminating in interest expense rising over $29 million compared prior year, or +37.6%, reflecting both larger principal balances outstanding amid active acquisition activity as well as upward pressure from increasing benchmark rates [S1].

Balancing this enhanced leverage requires careful stewardship since debt servicing consumes material share of cash flow despite long-dated secure leases backing substantial recurring rents.

However, stable occupancy metrics combined with predictable escalating rents provide confidence in debt coverage ratios remaining manageable if macro conditions do not deteriorate sharply.

Continuous monitoring of capital cost trends alongside prudent refinancing opportunities will remain critical factors impacting liquidity flexibility going forward.

What Recent Earnings Reveal About Portfolio Execution

Quarterly disclosures through early February highlight steady operational execution underscored by earnings per share and FFO outcomes matching analyst expectations despite persistent macroeconomic uncertainty including inflationary pressures [N1][N2]. The company successfully translated property additions into rental revenue gains without compromising occupancy or credit quality metrics materially — reflective of disciplined acquisition vetting processes.

Moreover steadiness amidst external headwinds reinforces confidence that portfolio quality remains intact supporting near-to-medium term cash flow projections integral for ongoing dividend distributions intrinsic to REIT investor value propositions.

Forward Views: Sustainability of Growth and Risk Challenges

Looking ahead ESSENTIAL PROPERTIES faces the balancing act common among aggressively expanding REITs: pursuing accretive acquisitions targeting further diversification without sacrificing yield stability or increasing exposure to deteriorating tenant credit profiles especially amid persistent inflation-driven cost escalations impacting maintenance overheads and taxation burdens ["Risk Factors"][S1].

With just over five percent of annualized base rent tied to leases expiring before January 2031 there is limited immediate rollover risk but vigilance around longer-term renewal economics remains warranted given evolving market rents could fluctuate significantly depending on economic cycles.

Management emphasis on proprietary underwriting frameworks integrated with continued broad geographical dispersion bodes well for containing localized downturn exposures but external factors such as higher interest rates or disruption within core industrial sectors always bear watching for indirect impacts on tenants’ operating environments.

In sum ESSENTIAL PROPERTIES' distinctive focus affords it several competitive advantages affording stable predictable cashflow streams anchored by extensive lease terms compounded with incremental contractual hikes while navigating inherent challenges typical within middle-market funding environments requiring ongoing prudent portfolio stewardship.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments