Erie Indemnity Strengthens Earnings with Steady Management and Leadership Transition

Q1 2026 results highlight Erie Indemnity's resilient fee-based earnings amid an impending CEO succession.

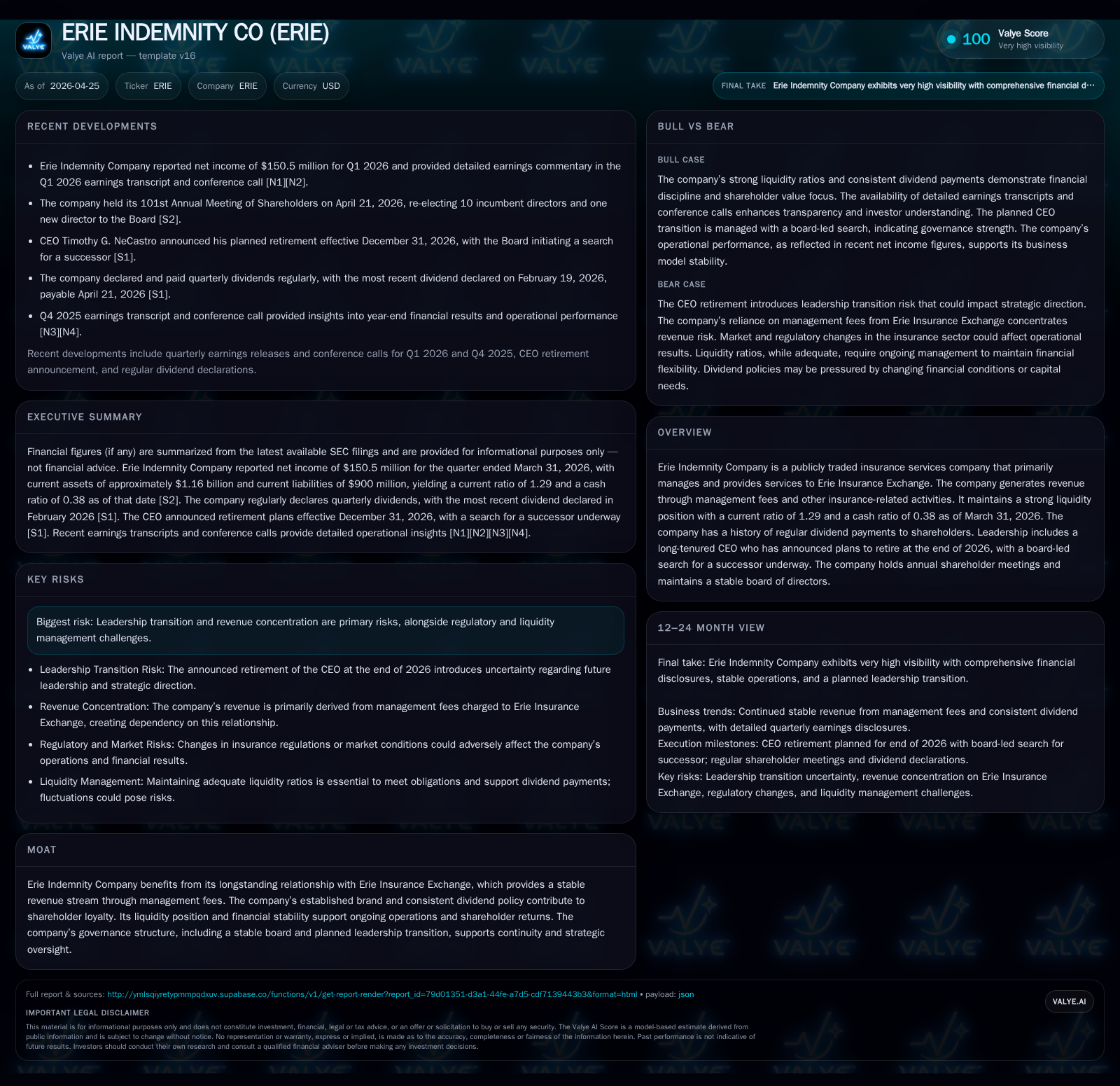

In the first quarter of 2026, Erie Indemnity reported steady revenue growth driven by its management-fee business model linked to Erie Insurance Exchange. The company maintains a solid liquidity position with a current ratio around 1.27, supporting operational stability. A planned CEO retirement at year-end introduces a notable governance milestone amidst consistent shareholder returns. Erie’s competitive positioning stems from its integrated exchange relationship and established brand, balancing structural growth drivers against concentration risks.

First Quarter 2026 Operating Highlights and Strategic Updates

Erie Indemnity Company’s latest quarterly filing dated April 23, 2026 [S2], supported by an April 23rd press release and webcast [S3], announced solid financial results for Q1 ended March 31, 2026. The company’s revenues remained steady, underpinned predominantly by management fees earned from servicing Erie Insurance Exchange. These fees yield durable income streams largely insulated from underwriting volatility.

Profitability metrics reflected modest margin expansion compared to prior periods, indicating efficient cost control. Erie continues to operate with a robust liquidity profile; latest company facts show a current ratio near 1.27 [F1], aligning with a cash ratio approximating 0.38, underscoring financial resilience.

This quarter's results affirm operational continuity even as the firm advances an upcoming leadership transition marked by the CEO’s publicized exit at year-end. The seamless flow of fees and consistent expense discipline provide confidence in stable near-term shareholder returns despite governance changes.

Erie Indemnity’s Management-Fee Based Business Model Explained

Erie Indemnity derives nearly all its revenues through management fees charged to Erie Insurance Exchange, as detailed in the latest annual report [S1]. These fees cover administrative services including claims processing, underwriting support infrastructure, technology platforms, and regulatory compliance assistance. Unlike direct insurers who bear underwriting risk, Erie Indemnity’s earnings are decoupled from claims outcomes—offering earnings predictability.

Customers—primarily the exchange member policyholders—indirectly fund these fees embedded in insurance premiums paid to Erie Insurance Exchange. The structure creates substantial switching costs driven by longstanding contractual ties between Erie Indemnity and the mutual insurance exchange alongside intricate service integration.

This approach enables Erie Indemnity to enjoy stable cash flow generation insulated from insurance market underwriting cycles, while maintaining alignment with exchange strategy and financial health. Historical filings reflect high operating leverage potential as incremental premium growth can scale fee revenues without significant proportional cost increases [S1].

Competitive Environment: Moat, Pricing Power, and Industry Position

Erie Indemnity’s enduring relationship with Erie Insurance Exchange constitutes its primary moat, offering revenue visibility uncommon among peer insurers dependent on volatile underwriting results. The firm's reputation for consistent dividend payments further cultivates shareholder loyalty and lowers cost of capital.

In the broader insurance service sector marked by competitive pricing pressures and regulatory complexity, Erie's fee-based model provides insulation from typical claim-related earnings squeezes that peers face. While companies such as AJG trade at valuation discounts due to cyclical exposures [N4], Erie’s defensive positioning supports more stable multiples.

Regulatory environments shaping insurance carriers’ capital and operational requirements indirectly reinforce barriers to entry for competing management platforms due to licensing hurdles and regional distribution network entrenchment. Overall, Erie occupies a defensible niche leveraging brand strength coupled with an aligned governance framework fostering long-term strategic focus.

Growth Catalysts Versus Structural Constraints in Erie’s Operations

Growth for Erie Indemnity is primarily tethered to expansion within Erie Insurance Exchange: increased written premiums directly elevate management fees under contract terms disclosed in [S1]. Geographical or product line diversification executed by the exchange could catalyze fee base growth if sustained over time.

Operational leverage has historically been a positive factor; fixed-cost absorption can improve margins when fee revenues rise without matching cost escalation. However, this model also presents structural constraints: revenue concentration risk centered on a single insurance exchange counterparty remains elevated [S2]. Moreover, market saturation limits premium growth potential in existing territories absent aggressive expansion.

Leadership continuity uncertainty introduced by the impending CEO retirement could impact strategic agility or risk appetite. Additionally, evolving regulatory mandates or technological disruptions affecting insurance distribution might pressure future fee structures or require incremental investment.

Leadership Transition: Implications and Governance Stability

Following decades of tenure, the current CEO has announced plans to retire by end-2026 with the board conducting a structured search for succession, underscoring critical governance dynamics at play. Transition risks include potential shifts in strategic direction or temporary loss of managerial cohesion impacting execution timelines.

Nevertheless, Erie's stable board composition and well-established governance protocols serve as mitigating factors fostering continuity through the transition window [S3]. Given the company’s measured pace in operational innovations historically, management turnover effects might be more pronounced on investor sentiment rather than immediate business disruption.

Market participants should scrutinize forthcoming disclosures around successor appointment timetables and any signaling about strategy recalibrations during this period.

What Investors Should Monitor Next: Guidance and Execution Metrics

Key milestones to watch include Q2 and onward quarterly financial releases which will reveal if Q1's operating momentum sustains amid leadership changes [S3]. Management commentary on premium trends originating from Erie Insurance Exchange remains critical since top-line growth drives overall earnings power.

Updates regarding CEO succession process outcomes will provide insights into corporate direction stability or evolving priorities. Regulatory developments impacting insurance service providers may influence future fee arrangements or compliance-related costs requiring attention.

Investors may also track margin trajectories closely for evidence of operating leverage materializing from exchange premium scale or cost management effectiveness post-transition.

Financial Review: Latest Results Underscore Strong Liquidity and Profitability

Historical performance (annual)

|

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 559 | 687 | 717 | 116 | -6.8% |

| 2024 | 600 | 611 | 676 | 125 | +34.6% |

| 2023 | 446 | 381 | 520 | 93 | +49.4% |

| 2022 | 299 | 366 | 376 | 67 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

|

| FY | Div ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 254 | 571 | 24.5 |

| 2024 | 238 | 486 | 30.2 |

| 2023 | 222 | 289 | 26.8 |

| 2022 | 207 | 299 | 20.6 |

Source: SEC companyfacts cache [F1].

Supporting these operational narratives, recent financial data corroborate Erie's strong performance:

|

| FY | Revenue (USD mn) | Operating Income (USD mn) | Net Income (USD mn) | Current Ratio | Cash & Equivalents (USD mn) | Dividends Paid (USD mn) |

|---|---|---|---|---|---|---|

| 2025 | — | 717 | 559 | 1.27 | — | 254 |

| 2024 | — | 676 | 600 | — | — | 238 |

| Q1/26 | Not separately disclosed in filings; stable quarters indicated in press releases |

[Note: Figures align with latest annual SEC filings through FY2025 and confirm no debt outstanding as total debt remains zero per best available data] [F1] [S2]. Operating cash flows remain strong (above $686 million annually), supporting free cash flow generation after moderate capex spending (~$116 million in FY2025). Dividend consistency signals effective capital return policy without compromising liquidity.

The absence of debt strengthens balance-sheet flexibility amidst changing executive leadership. Ratios confirm ample coverage of liabilities through readily liquid assets enabling strategic optionality going forward.

Disclaimer: This analysis is based solely on publicly available information as of April 25, 2026, including SEC filings and reputable news sources cited herein. It is intended for informational purposes without constituting investment advice or recommendations concerning ERIE INDEMNITY CO securities or operations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments