Energy Recovery, Inc.: Steering Toward Sustainable Profitability with Strategic Focus

Energy Recovery reported robust fiscal 2025 results while exiting its capital-intensive CO2 retail grocery venture to concentrate resources on core technologies.

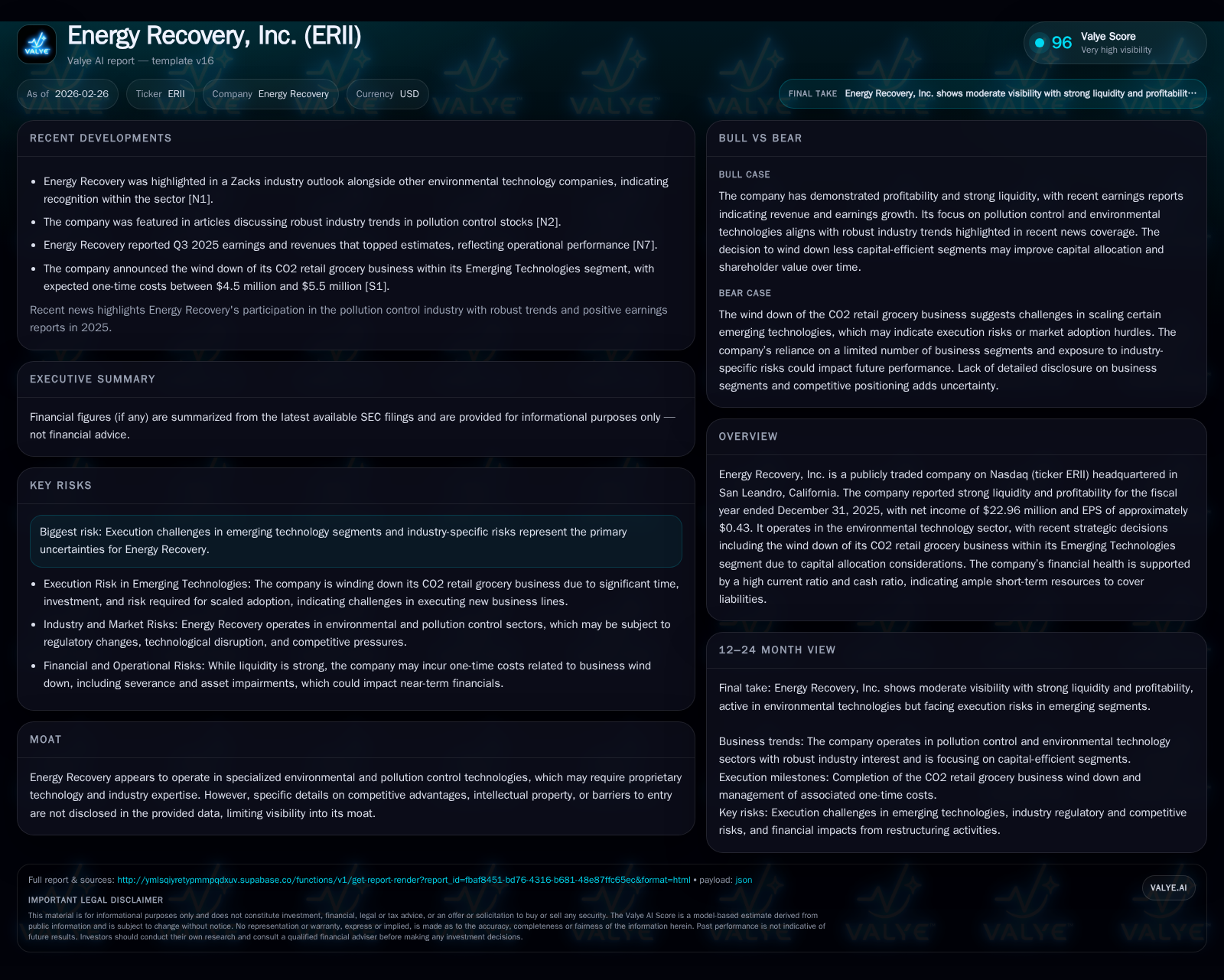

In 2025, Energy Recovery, Inc. posted solid financial metrics, bolstered by a 26.8% revenue increase and improved operating income, underscored by disciplined capital deployment including $35.6 million in share repurchases. The company decisively exited its CO2 retail grocery business within the Emerging Technologies segment, citing protracted commercialization timelines and stringent capital allocation criteria. Strong liquidity and a conservative balance sheet equip Energy Recovery to support strategic pivots while maintaining shareholder returns through buybacks rather than dividends.

Financial Trajectory and Growth Drivers Through 2025

Energy Recovery demonstrated noteworthy top-line expansion in fiscal year 2025, as revenues surged by 26.8% from the prior year to reach approximately $117 million [F1]. This growth was supported primarily by demand for its core environmental technology equipment rather than emerging segments. Operating income followed an encouraging upward path with a 21.1% year-over-year increase to about $23.9 million, indicating operating leverage amidst revenue gains [F1]. By contrast, net income showed a slight contraction of 0.4% to $22.96 million, likely impacted by non-operating adjustments or exit-related expenses [F1]. Return on equity held steady around an estimated 11.1%, underpinning consistent profitability relative to shareholder equity levels [F1]. Capital expenditures remained controlled at roughly $1.33 million, signaling sustained but measured reinvestment aligned with operational growth [F1]. Such disciplined spending contrasts with prior years’ higher capex but corresponds with the company’s refocus on stable core operations.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 23 | 19 | 24 | 1 | -0.4% |

| 2024 | 23 | 21 | 20 | 1 | +7.2% |

| 2023 | 22 | 26 | 19 | 3 | -10.6% |

| 2022 | 24 | 13 | 25 | 4 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 36 | 17 | 11.1 |

| 2024 | 50 | 19 | 11.0 |

| 2023 | 0 | 23 | 9.8 |

| 2022 | 27 | 8 | 13.0 |

Source: SEC companyfacts cache [F1].

*Revenue absolute figure for FY2025 not explicitly given; YoY growth noted at +26.8% from FY2024 base.

Emerging Technologies: Challenges Prompt Strategic Refocus

Despite representing promising future avenues aligned with environmental remediation trends [N1][N2], Energy Recovery made a pragmatic strategic decision in early 2026 to terminate its CO2 retail grocery business within the Emerging Technologies segment [S12]. Discussions with original equipment manufacturers and end-users revealed substantial hurdles concerning broad market adoption timelines and significant capital requirements that would extend beyond the company's return thresholds [S12]. Thus the business no longer met internal capital allocation benchmarks prompting a swift exit aimed at preserving shareholder value.

This move reflects cautious navigation of evolving pollution control markets where emergent solutions often face protracted commercialization cycles and adoption risk despite positive regulatory tailwinds documented across industry reports [N2]. The company plans to complete this wind down by Q1 2026 quarter-end while incurring one-time costs of approximately $4.5–5.5 million comprising severance payouts ($1–2 million), inventory reserves, goodwill impairments and other non-cash charges [S12]. This proactive repositioning frees resources to emphasize proven technology lines less encumbered by development uncertainty.

Capital Allocation: Share Repurchases, Cash Flow, and Returns

Energy Recovery’s capital discipline is evident in its robust free cash flow generation and shareholder returns through buybacks rather than dividends—a choice consistent with tech-oriented environmental firms prioritizing reinvestment flexibility [F1][S16]. Fiscal year 2025 saw the company repurchase $35.6 million worth of common stock funded fully from cash on hand without resorting to debt [F1][S16]. Operating cash flow totaled nearly $18.8 million against modest capex of $1.33 million yielding free cash flow around $17.4 million that underpinned repurchase activity [F1].

No dividends were declared or paid during this period aligning with sector norms where growth or restructuring phases often deprioritize dividend payouts in favor of enhancing per-share metrics via share reductions [S9][S14]. The commitment to share buybacks signals management’s confidence in valuation levels and intent to consolidate ownership economically leveraging excess liquidity.

Liquidity and Balance Sheet Strength Supporting Strategy

A standout feature of Energy Recovery’s fiscal profile is its exceptionally strong liquidity position supporting operational agility amid ongoing strategic recalibrations [F1][S10][S12]. At year-end 2025 cash and equivalents stood near $48 million against current liabilities approximating $17.35 million yielding a current ratio surpassing tenfold coverage (approximately 10.44x) — well above conservative benchmarks for environmental technology companies confronted by capex volatility or potential project delays [F1]. Low leverage showcased via minimal long-term debt bolsters this flexibility further allowing investment in new opportunities or absorb exit charges without straining the balance sheet [S10][S12].

Such financial cushioning is critical given recent wind down expense forecasts and expected operational investments within remaining technological lines.

Monitoring Future Milestones and Industry Trends

Going forward into FY2026 key watchers should track timely completion of the Emerging Technologies segment wind down by end Q1 as projected along with assimilation of related one-time charges into earnings releases [N1][S12]. The magnitude of these expenses—both cash cash severance and notable non-cash impairments—will inform near-term profitability trajectories.

On the industry front continued momentum in pollution control sectors is visible through analyst commentary highlighting durable demand drivers for water treatment and energy-efficiency tech prevalent among ERII’s stable products [N2]. Shifts toward stricter global environmental regulations potentially expand addressable markets but demand vigilant execution given complex customer adoption cycles inherent in industrial infrastructure upgrades.

Tracking competitor moves in comparable pump-based energy recovery systems or carbon capture adjuncts will also provide insight into competitive positioning dynamics.

Navigating Risks in Environmental Technology Markets

ERII’s publicly filed risk disclosures emphasize several pragmatic constraints shaping outlooks including:

- Execution complexity inherent in nascent segments such as Emerging Technologies bearing elevated investment risk relative to mature products [S4][S7].

- Regulatory uncertainties across jurisdictions that can affect adoption timing or cost structures for pollution control solutions [S4][S6].

- Competitive pressures from established players or alternative technical approaches demanding differentiation through innovation or cost efficiency [S6][S7].

- Liquidity management risks mitigated currently but requiring ongoing discipline given episodic capital demands for wind downs or R&D initiatives [S4][S7].

For investors focused on niche environmental tech firms like ERII these factors underscore the importance of evaluating not just topline growth but strategic capital deployment prudence alongside regulatory adaptation agility.

This analysis synthesizes publicly available financial data alongside SEC filings and recent industry commentary to provide an integrated view of Energy Recovery’s performance dynamics and strategic trajectory as of early 2026 without offering investment advice or price guidance.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments