Essent Group Ltd.'s Earnings Volatility and Capital Allocation Highlight Constraints on Growth

Essent Group reports modest revenue growth with net income pressure and significant share repurchases amid limited segment transparency.

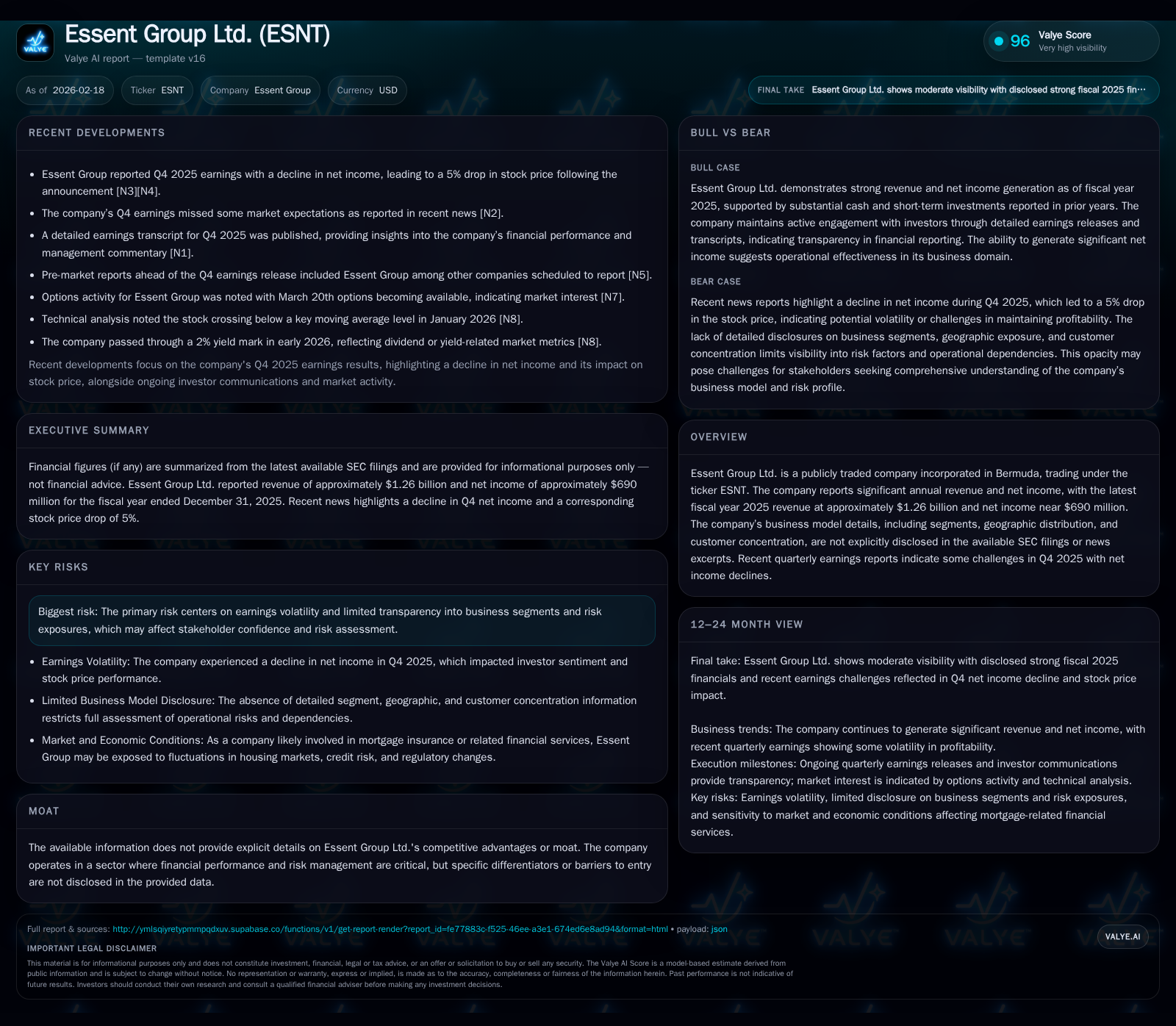

Essent Group Ltd. posted modest revenue growth of 1.5% in 2025, reaching $1.26 billion, while net income declined by 5.4% year over year to approximately $690 million. The company’s capital allocation includes increasing dividends and a substantial surge in share buybacks, indicating a focus on shareholder returns despite earnings softness. Operating cash flow remains strong, supporting these distributions. Essent operates in a sector characterized by earnings volatility and limited public detail on business segments or risk exposures, complicating assessment of future growth drivers. Investors should monitor loan default rates, new insured written volumes, and portfolio composition as key indicators of future performance.

Historical Performance and Revenue Growth

Essent Group Ltd. has demonstrated steady revenue growth over the past several years, reaching $1.26 billion for fiscal year 2025—a 1.5% increase over the prior year's $1.24 billion [F1]. This follows a trajectory from $1.00 billion in 2022 to nearly $1.11 billion in 2023 and then to $1.24 billion in 2024. Despite top-line gains, net income declined from $729 million in 2024 to approximately $690 million in 2025, a -5.4% year-over-year decrease [F1].

The net income decline coincided with challenges reported during Q4 2025, likely due to increased claims or loss reserves within their mortgage insurance portfolio [N1],[N2],[N6]. This reflects the earnings volatility typical of credit-sensitive insurers impacted by economic factors influencing default risks.

Essent Group Annual Financial Summary

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | Capex ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 1261 | 690 | 856 | 7 | +1.5% | -5.4% |

| 2024 | 1243 | 729 | 862 | 7 | +12.0% | +4.7% |

| 2023 | 1110 | 696 | 763 | 4 | +10.9% | -16.2% |

| 2022 | 1001 | 831 | 589 | 4 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): OpInc. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | FCF ($mm) |

|---|---|---|---|

| 2025 | 122 | 588 | 849 |

| 2024 | 118 | 112 | 855 |

| 2023 | 106 | 71 | 759 |

| 2022 | 92 | 98 | 585 |

Source: SEC companyfacts cache [F1].

Amounts rounded; Capex represents property & equipment purchases. Note: Operating income data insufficient for inclusion; estimated ROE is approximately 12%, calculated using latest net income and equity figures [F1].

Capital Allocation and Returns

Essent's operating cash flow remained strong at about $856 million in FY2025 [F1], supporting robust free cash flow estimated at approximately $849 million after capex deductions [F1]. This cash generation underpins rising dividends—$122 million paid in FY2025—and a marked increase in share repurchases from $111 million in FY2024 to nearly $588 million in FY2025 [F1].

The company's equity base has grown steadily from roughly $4.46 billion at end-2022 to about $5.76 billion at end-2025 [F1], underpinning an approximate return on equity near 12%. This level indicates moderate capital efficiency consistent with the capital-intensive nature of private mortgage insurance.

Business Model, Segments and Industry Context

Essent primarily operates as a private mortgage insurer underwriting credit risk for residential mortgages where borrowers have insufficient down payments [S6]. Portfolio characteristics include borrower credit scores, loan-to-value ratios, amortization periods, and geographic concentrations across key U.S states and metropolitan areas [S6]. However, the company does not disclose detailed segment revenue or customer concentration data publicly.

Private mortgage insurers generally benefit when purchase originations surpass refinancing volumes since premiums are collected upfront on new policies [S6]. Market dynamics such as interest rates and housing affordability materially influence these origination trends.

Risks and Earnings Volatility

The company acknowledges significant risks stemming from credit performance of insured loans including default rates by vintage cohorts which affect loss reserve adequacy [S4],[S8]. Recent quarterly results indicated rising claims impacting profitability [N2],[N6], illustrating inherent earnings volatility.

Limited disclosure on segment details constrains external evaluation of exposure concentrations or sensitivity to economic scenarios [S6],[S8]. Regulatory risks also persist given the compliance landscape surrounding mortgage insurers [S4],[S7].

Liquidity and Capital Structure

SEC filings reflect stable liquidity supported by resilient operating cash flows paired with prudent capital structure management [S13],[S15],[S16]. No material debt distress or covenant issues are reported despite substantial capital returned through dividends and share buybacks.

This financial strength allows Essent to maintain underwriting capacity while meeting regulatory capital requirements customary for insurers.

Future Growth Prospects and Monitoring Points

Growth drivers include expanding new insured written volumes (NIW)—particularly from purchase originations—that generate premium inflows [S6]. Effective credit risk management to reduce defaults alongside product innovation and potential geographic diversification are additional levers.

Investors should monitor:

- Quarterly NIW trends segmented by purchase versus refinancing originations,

- Default rates by loan origination vintage,

- Loss reserve adequacy relative to claim experience,

- Changes in borrower credit scores or LTV profiles,

- Regulatory developments affecting underwriting standards or capital requirements.

No explicit forward guidance or milestone disclosures were found in recent reports ([N1],[N3],[S3]). Operational metrics remain crucial indicators of Essent’s trajectory.

Conclusion

Essent Group Ltd.’s latest full-year results reveal a resilient yet volatile earnings profile typical of private mortgage insurers amid shifting housing market conditions.

While revenue growth persists albeit slowed in FY2025, net income contraction highlights transient headwinds likely linked to elevated claims late last year [N2],[N6]. Strong operating cash flows support meaningful shareholder returns through dividends and accelerated buybacks emphasizing disciplined capital deployment [F1].

However, limited disclosure on segment contributions and portfolio risk complicates comprehensive forecasting beyond macroeconomic industry themes such as housing demand shifts and credit cycle risks [S6].

Market participants should prioritize detailed loan performance data releases alongside broader residential mortgage origination trends given their outsized impact on private mortgage insurer economics.

Disclaimer: This analysis is based solely on available public financial filings and news reports without providing investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments