Cannabis Bioscience International Stakes Its Claim in Medicinal Cannabis Research and Education

CBIH pursues scientific leadership in cannabis through diverse businesses and patent-driven innovation despite financial and scale challenges.

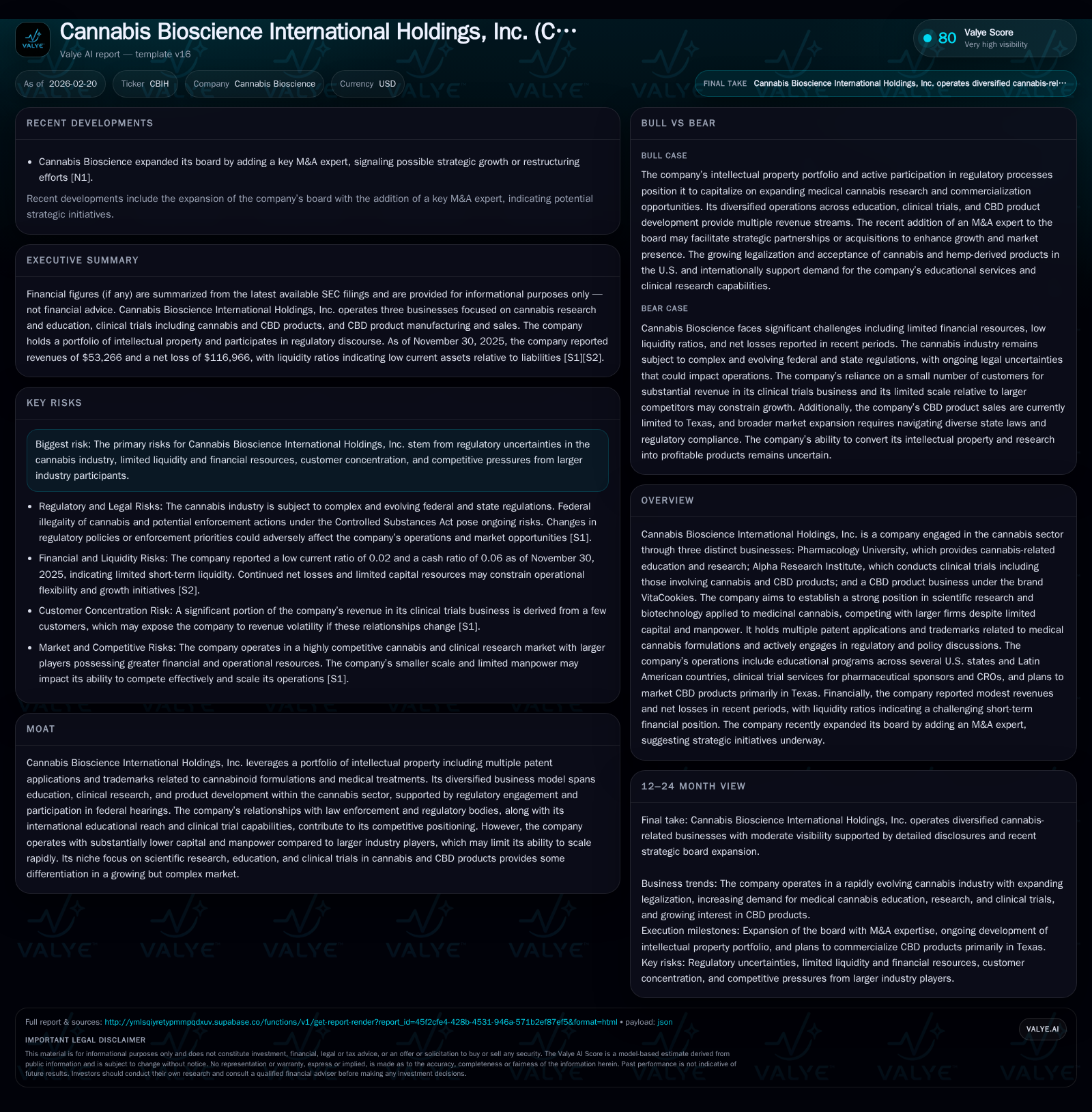

Cannabis Bioscience International Holdings, Inc. operates three main businesses—Pharmacology University (cannabis education), Alpha Research Institute (clinical trials), and the CBD product line VitaCookies—striving to carve a niche in medicinal cannabis research. The company has steadily grown revenues with a 21.8% increase from FY2024 to FY2025, largely driven by clinical trial contracts, but continues to operate at a loss amid funding constraints. Its portfolio of patent applications across cannabinoid formulations provides strategic differentiation, supporting a platform for future growth anchored in clinical trial expansion, international education programs, and anticipated commercial rollouts. Persistent regulatory uncertainties and customer concentration remain key risks. Financial metrics show negative equity nearing $1.16 million as of FY2025 with no dividends paid and minimal buybacks recorded, highlighting liquidity pressures and constrained cash flows.

Evolution of Cannabis Bioscience’s Business Model: Growth Through Diversified Segments

Cannabis Bioscience International Holdings, Inc. (CBIH) operates through three primary segments that together articulate its vision for a scientific foothold in medicinal cannabis. Pharmacology University delivers cannabis-focused educational content to diverse stakeholders, ranging from medical professionals to entrepreneurs across the United States and Latin America. This division leverages a sophisticated content library featuring 50 eBooks and over 13,000 minutes of audio translated into five languages, supplemented by AI-powered services extending reach up to 100 languages [S1][S15].

Alpha Research Institute functions both as a Clinical Research Organization (CRO) and sponsor of clinical trials, conducting studies across multiple therapeutic areas including asthma, oncology, neurology, and now increasingly cannabinoid-based drugs [S11][S16]. It employs experienced clinical research coordinators (CRCs) and collaborates with independent principal investigators to manage complex protocols aligned with FDA and IRB standards [S13][S16].

The third pillar is the CBD product enterprise under the VitaCookies brand which the Company intends to develop commercially following demonstration of safety and efficacy through clinical trials [S11][N1]. Although this segment is still emerging without final sales figures disclosed publicly, its integration complements CBIH's broad bioscience approach.

CBIH differentiates itself partly through an actively managed intellectual property portfolio including ten filed utility patents focusing on cannabinoid formulations tailored to ailments such as menopause and PTSD, alongside twelve registered U.S. trademarks relating to its brands [S1][S5]. These elements serve as foundational moat components in an otherwise capital-intensive industry dominated by larger competitors.

Despite operating with limited human resources—a total of two full-time employees supplemented by roughly fourteen contractors—and constrained facilities leasing modest office space in Houston totaling approximately 2,767 square feet combined across locations [S5], the company maintains an ambitious agenda spanning education, research and product innovation.

Analyzing Historical Financial Performance and Operating Dynamics

Financial data confirms steady top-line growth tempered by persistent losses reflecting early-stage investment in infrastructure and R&D activities characteristic of biopharmaceutical enterprises [F1]. Revenues rose 21.8% year-over-year from approximately $249K in FY2024 to $303K in FY2025 [F1], predominantly derived from Alpha Research's clinical trial services which accounted for over 90% of total revenue sourced mainly from two customers contributing 66.7% and 24.1% respectively [S11].

Operating income losses narrowed by about 13%, improving from -$486K to -$421K over the comparable periods [F1], while net losses also improved moderately by nearly 16% albeit remaining substantial at -$549K for FY2025 [F1]. Operating cash flows showed meaningful improvement with a 31.2% reduction in outflows down to -$330K though still far from positive territory [F1].

This financial profile reflects the company's small scale yet operational traction particularly within contract research where fixed expense leverage remains limited by workforce size and modest overheads aligned with leased office arrangements rather than proprietary lab spaces [S5]. Minimal capital expenditure was recorded recently aside from historical outlays exceeding $4.6 million documented a decade ago without follow-up investments as per filed reports [F1].

Historical performance (annual)

| FY | Rev ($) | Net ($) | CFO ($) | OpInc ($) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 303022 | -548820 | -329627 | -421365 | +21.8% | +15.7% |

| 2024 | 248841 | -651345 | -479382 | -486140 | ||

| 2012 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Capex, Div, Buybacks, FCF. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | ROE% |

|---|---|

| 2025 | 47.2 |

| 2024 | 60.4 |

| 2012 |

Source: SEC companyfacts cache [F1].

Note: Capex data insufficient for recent years; dividends not available; buybacks minimal at $19K recorded in FY2024.

Harnessing Intellectual Property Amidst Industry Complexity

CBIH’s patent strategy is integral to its positioning within the evolving medical cannabis landscape. Since late 2024 alone, the company has filed about ten utility patent applications covering advanced cannabinoid therapeutics targeting diverse indications such as depression management via the microbiota-gut-brain axis (Application No.18/929972), anxiety disorders (No.18/934360), multiple sclerosis (No.18/942512), oral care treatments (No.18/957035), pancreatic cancer (No.18/905128), breast cancer employing VEGF inhibition mechanisms (No.18/918386), shingles treatment (No.18/920359), knee osteoarthritis (No.18/922127), menopause symptoms (No.18/921140), and respiratory viral infections (No.18/924087) [S5][S24].

Complementing these filings are twelve registered U.S. trademarks underpinning brand identity alongside more than one hundred medical formulations encompassing various cannabinoids aimed at treating conditions including PTSD, dysbiosis, depression and Alzheimer’s disease [S1][S17]. These innovations contribute not only intellectual property protection but also establish scientific credibility critical for navigating FDA regulatory pathways.

Given that many companies within cannabis bioscience compete primarily on scale or distribution channels rather than deep biomedical IP portfolios, CBIH leverages this specialized focus on biotechnology-driven differentiation despite limitations in capital intensity.

Future Growth Catalysts Anchored in Clinical Trials, Education, and Product Launches

The company's roadmap includes several prospective drivers poised to lift growth beyond current operational levels though explicit financial forecasts remain undisclosed [N1][S7]. Alpha Research Institute aims to transition from exclusively conducting clinical trials for external Sponsors or CROs towards sponsoring Phase I cannabinoid drug trials internally—a critical step denoting control over investigational new drug development phases that test safety thresholds in small subject groups [S13][S16].

Parallel expansions target Pharmacology University's educational programs which currently distribute hundreds of digital assets through global marketplaces including Amazon and Google Books across multiple languages supported by AI-enabled translation technology poised to scale content penetration further into Latin America and other emerging markets [S15]. Expansion plans include reinstating live seminars focused on regulated state medical cannabis regimes such as Texas’ Compassionate Use Program (TCUP) following legislative enhancements via HB46 which expanded qualifying conditions for therapy [S21].

On the product front, VitaCookies’ commercialization remains an important milestone that could monetize prior R&D investments contingent on favorable clinical trial outcomes validating safety and efficacy profiles [N1][S7]. Strategic board additions with mergers & acquisitions expertise may catalyze partnerships or bolt-on transactions accelerating product pipeline advancement or geographic footprint expansion [N1].

Since formal guidance on timelines or revenue targets is absent, observers should monitor initiation announcements for Phase I trials, enrollment figures for educational courses internationally beyond Texas & Latin America deployment velocity plus any reported commercial sales progress relating to VitaCookies.

Navigating Regulatory Challenges and Company’s Policy Engagement

Federal prohibition classifies cannabis excluding hemp-derived products as Schedule I substances under the Controlled Substances Act (CSA), constraining operational latitude despite widespread state-level legalization—resulting in persistent legal complexities around manufacturing licenses, clinical research authorization via DEA registrations and FDA oversight depending on product claims [S23][S12][S25].

CBIH participates actively in policy discourse exemplified by involvement in the DEA's paused marijuana rescheduling hearings slated to resume when regulatory momentum allows it [S1][S17]. The company advocates scientific research support emphasizing regulated access frameworks vital for legitimacy.

Sector-native context recognizes that DEA scheduling directly impacts permissible clinical trial design parameters such as sourcing federally approved cannabis batches versus hemp-based compounds under less stringent rules governing investigational new drug applications (INDs). Similarly FDA scrutiny governs marketing claims requiring rigorous Phase II-III efficacy validation limiting premature commercialization absent full approvals.

Consequently CBIH’s strategy balances advancing products through initial safe-use human studies while navigating complex regulatory approvals ensuring eventual market readiness compliant with federal frameworks.

Capital Allocation Strategy: Cash Flow Profile, Equity Status, and Shareholder Returns

Despite incremental operational improvements reflected in decreasing losses across metrics — net income improved ~15%; operating cash flow improved by over 30% year-on-year — the company remains deeply cash flow negative constraining discretionary spending capacity essential for R&D scaling or marketing investments simultaneously required for expansion initiatives [F1].

Equity stands negative around -$1.16 million trending downwards from the prior year deficit near -$1.08 million reflecting cumulative losses exceeding shareholder contributions likely compounded by repeated operating shortfalls without significant capital raises disclosed recently [F1][S27]. Liquidity positioning is precarious given current assets near $22K sharply outweighed by current liabilities exceeding $1.13 million resulting in an ultra-low current ratio (~0.02) indicating substantial working capital stress at period end November 2025 [F1].

Dividend distributions are absent consistent with typical early-stage developmental biotech models while historical low-scale stock repurchase activity (~$19K buybacks recorded FY2024) suggests no routine shareholder return mechanism presently deployed [F1].

Given these factors internal cash generation appears insufficient warranting external financing or strategic alliances critical for sustaining operations or accelerating product commercialization—highlighted recently by board expansion aimed at bolstering M&A capabilities potentially signaling intent or necessity of capital market activity or partnership transactions [N1].

Risks from Market Concentration and Funding Constraints Worth Watching

Key vulnerabilities stem chiefly from client concentration within Alpha Research where two customers constitute approximately 90+% of total revenue exposing operational cash flow stability heavily reliant on renewing sizable contracts which if disrupted could materially impact results [S5][S11].

Regulatory uncertainty persists due to federal Schedule I classification maintaining legal ambiguity that could hinder licensing flexibility or escalate compliance costs impacting timelines especially given proceedings like DEA hearings remain paused indefinitely pending political will shifts [S12][S25].

Limited manpower—merely two full-time officers supplemented by fluctuating contractor counts—alongside scant liquidity restricts rapid scalability potential relative to industry leaders commanding robust balance sheets facilitating multi-phase global trials or large scale manufacturing deployments [S5][F1]. These financial/funding constraints inherently cap pace at which intellectual property can be converted into commercially viable assets.

Investors should closely monitor developments around diversification of contract sponsors within Alpha Research reducing concentration risk plus funding milestones such as successful capital raises or strategic partner integrations enhancing resource availability.

Disclaimer: This analysis is based solely on information available as of February 20, 2026 including SEC filings and recent news releases; it does not constitute investment advice but aims to provide a comprehensive understanding of Cannabis Bioscience International Holdings' business dynamics within the evolving medicinal cannabis sector.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments