Select Medical’s Earnings Slip Amid Regulatory Headwinds and Expansion Moves

Select Medical reported robust operating income growth in 2025 despite regulatory reimbursement pressures, with joint ventures supporting expansion but cash flow showing contraction.

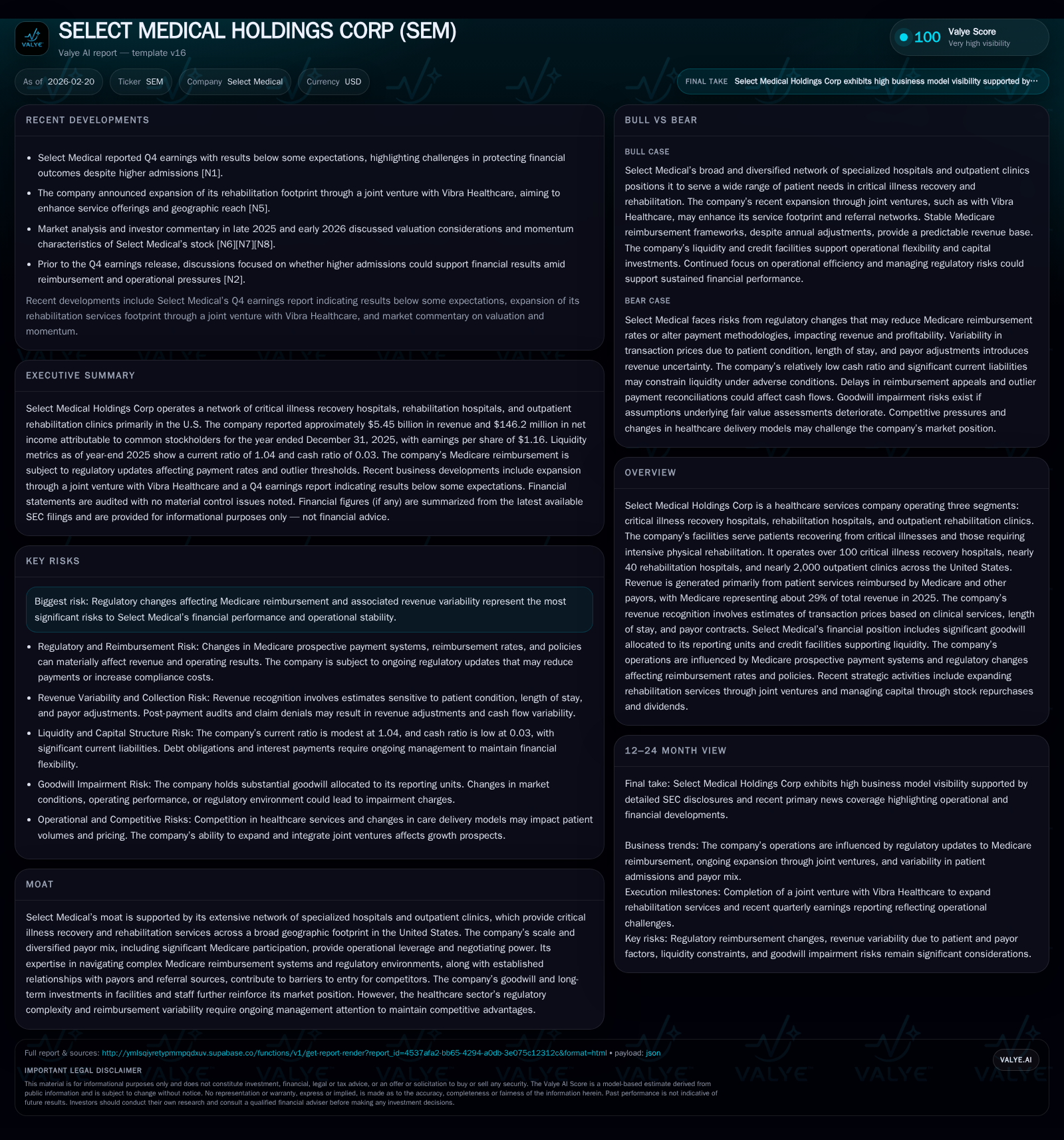

In fiscal 2025, Select Medical Holdings Corp (SEM) delivered a substantial 25.3% year-over-year increase in operating income and a strong net income rebound after a prior year loss; however, operating cash flow declined sharply by 33%. This divergence stems largely from delayed Medicare outlier payment reconciliations caused by recent CMS policy changes affecting long-term acute care hospitals (LTCHs) and the inpatient rehabilitation facility prospective payment system (IRF-PPS). The company advanced its rehabilitation footprint through a joint venture with Vibra Healthcare early in 2026, signaling growth ambitions amid ongoing regulatory uncertainties. Capital allocation favored share repurchases over dividends, funded by a revolving credit facility that preserves liquidity while maintaining leverage well below covenant limits. Looking ahead, Select Medical faces a balance between expanding its outpatient network and managing reimbursement risks tied to evolving Medicare policies.

Financial Snapshot: 2025 Revenue and Profit Highlights

Select Medical Holdings Corp closed fiscal year 2025 with notable operational improvements despite underlying regulatory challenges. Revenue remained approximately stable near $1.27 billion — consistent with historical levels reported as of Q3 2018 but no more recent revenue data available in tags [F1] — while operating income jumped sharply by 25.3% YoY to $336.2 million from $268.3 million in 2024 [F1]. This reflects operational leverage partially offsetting reimbursement headwinds.

The company swung from a net loss of $16 million in FY2024 to a net income of $146.2 million in FY2025, marking an over tenfold improvement signifying improved bottom-line management and possibly favorable tax or nonrecurring items [F1]. However, a sharp contrast emerges in cash flow metrics: operating cash flow (CFO) contracted by over one-third (-33%) to about $346 million in FY2025 from roughly $518 million the year prior, underscoring the impact of Medicare payment timing delays and working capital demands [F1].

Historical Growth Trends: From Prior Years Through 2025

Reviewing longer-term trends reveals Select Medical’s revenue baseline has hovered near the reported $1.27 billion mark as of the latest available point (Q3 2018), but no updated revenue figures were provided for recent years in the available tags [F1]. Operating income showed pronounced volatility: strong profits above $400 million in earlier years gave way to declines culminating in losses around FY2024 before bouncing back robustly in FY2025 [F1]. Net income similarly shifted from healthy gains (e.g., $243 million in FY2023) down to losses before recovering strongly last year.

Capital expenditures have been relatively steady at approximately $220–$230 million annually since FY2023 reflecting ongoing facility maintenance and upgrades necessary for specialized care delivery [F1].

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 146 | 346 | 336 | 229 | +1011.0% |

| 2024 | -16 | 518 | 268 | 222 | -106.6% |

| 2023 | 243 | 582 | 555 | 229 | +53.1% |

| 2022 | 159 | 285 | 403 | 190 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Rev, Div, Buybacks. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | 117 | 8.6 |

| 2024 | 296 | -1.0 |

| 2023 | 353 | 18.9 |

| 2022 | 94 | 14.2 |

Source: SEC companyfacts cache [F1].

Note: Revenue data for recent years is not available from provided tags; fluctuations largely reflect Medicare reimbursement policy impacts.

Medicare Reimbursement Policy Impact on Profitability

CMS’s evolving payment policies exert critical pressure on Select Medical’s financial performance, especially LTCH outlier payments under the Long-Term Care Hospital Prospective Payment System (LTCH-PPS). A key recent change doubled the threshold for reconciling outlier payments—now requiring a minimum change of 20% rather than the former 10% in Cost-to-Charge Ratio (CCR) before reconciliations trigger — leading to increased settlements and potential recoupments from CMS starting with reports due post-Oct 2025, with expected first settlement impacts only materializing by early 2027 [S1].

This shift amplifies revenue recognition uncertainty as payments historically accrued become subject to adjustment months or years later, causing delayed cash inflows despite accruing revenue on an estimated basis.

Equally pivotal is the IRF-PPS update effective FY2024 which fine-tunes inpatient rehabilitation facility reimbursements based on patient complexity and therapy intensity metrics. These updates introduce further variability into remuneration streams for the rehabilitation segment, necessitating refined operational efficiency and billing acumen [S1]. Both factors contribute heavily to the apparent disparity between improving earnings yet softening operating cash flow reported last year.

Expansion Through Joint Ventures: Vibra Healthcare Partnership Case

In January 2026, Select Medical enhanced its rehabilitation hospital platform through a strategic joint venture with Vibra Healthcare Holdings. This collaboration injects additional scale across inpatient rehabilitation centers leveraging Vibra’s regional presence and hospital networks alongside Select’s outpatient clinics' referral channels [N5].

Such JV models provide dual benefits: economies of scale for capital deployment and expanded market reach strengthening negotiating power with payors including diversified private insurers beyond Medicare dominance. This synergy aims to boost top-line growth prospects modestly yet sustainably while providing operational leverage anchored by deeper geographic penetration and integrated continuum-of-care offerings.

Liquidity and Credit Position: Managing Debt Under Tight Covenants

Select Medical retains a disciplined approach managing its capital structure amid expansion needs and volatile reimbursement regimes. As of December 31, 2025, total debt stood at approximately $1.85 billion comprising a $1.04 billion term loan (due December 2031) bearing Term SOFR + ~2%, revolving borrowings totaling $100 million from a secured credit facility expiring late-2029, plus senior notes amounting to $550 million maturing in 2032 at a fixed coupon of 6.25% [S4][S5][S6].

Financial covenants remain comfortably met with reported leverage ratio (~total indebtedness/EBITDA) at about 3.67x against a maximum allowed threshold of 7x [S4], highlighting headroom for liquidity maneuvers.

The revolving credit line delivers flexible liquidity ($469 million available net of current draws), enabling the company to fund acquisitions or opportunistic growth without jeopardizing compliance or risking costly refinancing under stressed conditions.

Capital Allocation: Share Repurchases Versus Dividends Dynamics

Capital deployment highlights reveal an aggressive share repurchase strategy prioritized over dividend growth or reinstatement following disruptions earlier in the decade. The board authorized up to $1 billion for buybacks through end-2027; Select expended nearly $697 million cumulatively through FY2025 including ~$96.5 million just last year acquiring more than six million shares at an average price near $15 per share inclusive of transaction costs [S7].

Dividend payments resumed modestly during FY2025 after absent payouts previously, evidenced by quarterly dividends totaling approximately $31 million across the year at roughly $0.0625 per share rate [S7] though yield remains low relative to equity size.

Repurchases have sometimes leveraged revolver borrowings alongside operational cash flow; however this strategy incurs additional costs such as the newly imposed federal excise tax on stock buybacks exceeding set thresholds under the Inflation Reduction Act effective from early-2023 causing ~$0.8 million excise fees accrued last year [S14].

Future Outlook: Navigating Regulatory Risks and Growth Opportunities

Looking forward, Select Medical's growth trajectory hinges critically on stabilization of Medicare reimbursement policy particularly regarding LTCH outlier payments where forthcoming CMS administrative rulings will determine settlement volumes potentially impacting both cash flow timing and revenue accuracy starting FY2027 book closings onward [S1][N2].

Parallel opportunity arises from scaling outpatient clinics adjacent to established hospital footprints which benefit from referral synergies offering higher-margin services less exposed to acute reimbursement cuts.

The ongoing Vibra JV partnership represents an important channel for realization of rehab segment growth ambitions through network density effects enhancing payer negotiations and clinical throughput efficiency.

Nevertheless, regulatory scrutiny remains high amid federal investigations into billing practices involving outpatient therapy services which expose Select Medical to litigation risks and potential financial penalties that could undermine future earnings reliability if protracted or escalated beyond current provisions [S8][S9].

Stakeholders should closely monitor CMS updates on reconciliation criteria enforcement schedule alongside quarterly admission trends that may buffer revenue fluctuations caused by shifting payor dynamics.

Disclaimer: This report is based solely on data available up to February 20, 2026 from SEC filings and public news sources without providing investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments