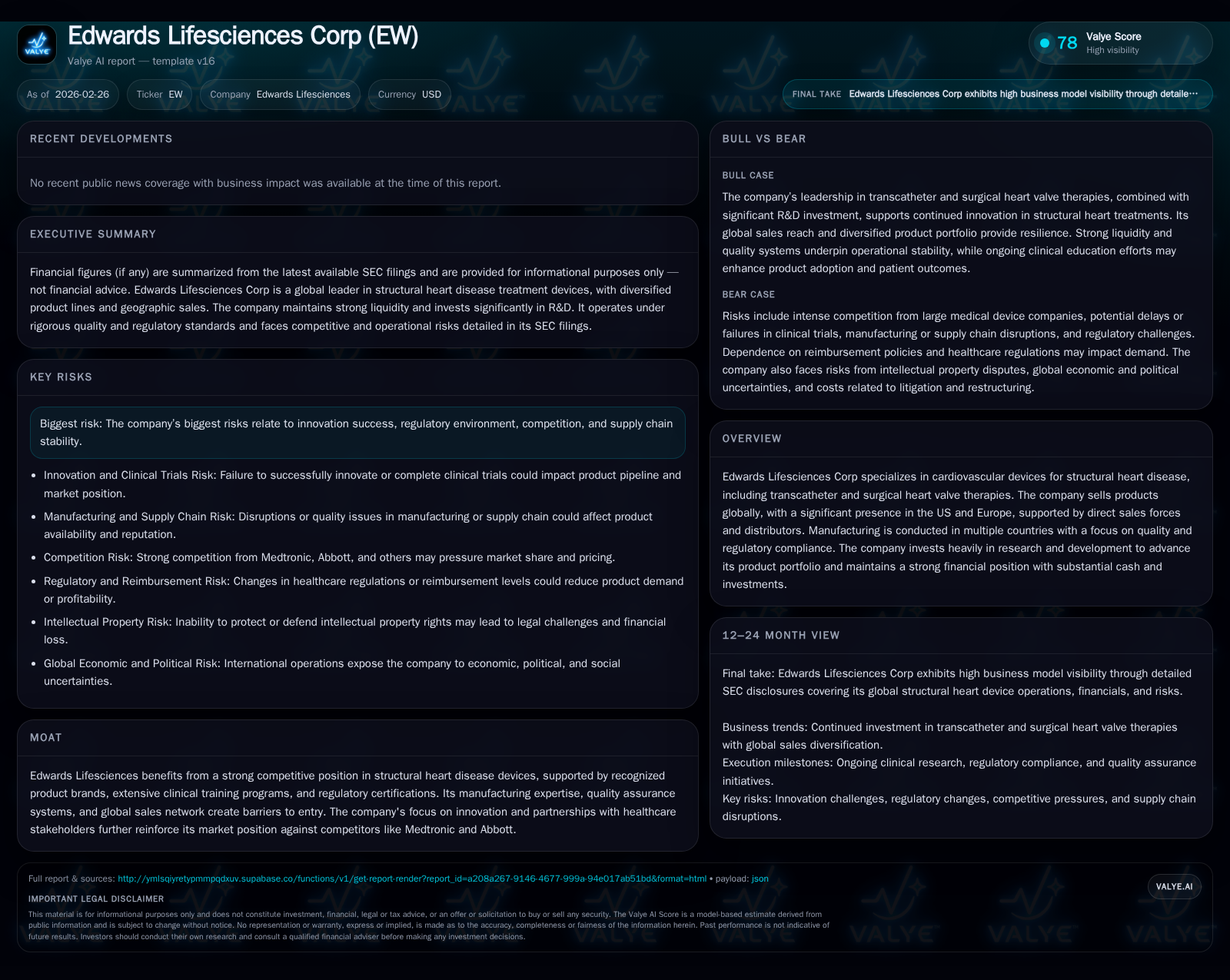

Edwards Lifesciences Advances Structural Heart Device Leadership with Innovation and Strong Financial Execution

Edwards Lifesciences Corp leverages its market position in cardiovascular devices, supported by global sales and R&D, while navigating regulatory and competitive pressures.

Edwards Lifesciences has grown steadily over recent years, driven by leadership in transcatheter and surgical heart valve technologies and expansion into new markets. Its 2025 performance features revenue growth of approximately 15.7% year-over-year, although operating income declined by 8.3% as investment and margin pressures mounted. The company’s strong cash flow generation, with free cash flow exceeding $1.3 billion, supports ongoing R&D and disciplined capital returns via share repurchases. Looking ahead, Edwards’ growth depends on product innovation, regulatory approvals, clinical adoption of new therapies, and supply chain stability amid intensifying competition from major players like Medtronic and Abbott.

Company Overview

Edwards Lifesciences Corp is an established leader in cardiovascular medical devices focused primarily on structural heart disease treatments. Its product suite centers on transcatheter and surgical heart valve therapies that address critical unmet needs in a growing patient population with valvular heart conditions [S1][S5]. The company operates globally with a direct sales force in core markets like the United States—where it derives 58% of its revenues—and Europe where it holds roughly 60% of its non-U.S. sales alongside presence in Japan (14%) and other regions (26%) [S5].

Manufacturing is diversified across the U.S., Singapore, Costa Rica, and Ireland to maintain supply continuity and meet stringent quality standards required in this heavily regulated sector [S5]. Edwards invests heavily in research and development to fuel innovation across its three key therapy areas: Implantable transcatheter aortic valve replacement (TAVR), transcatheter mitral/tricuspid therapies (TMTT), and surgical valves [S1][S5].

Historical Performance

Edwards has delivered considerable top-line growth over recent fiscal years. Revenue rose from approximately $767.7 million in FY2016 to an estimated $8.95 billion by FY2025—a compound trajectory underscoring expanding market penetration for minimally invasive valve therapies [F1]. However, operating income demonstrated some volatility; after peaking at nearly $1.75 billion in FY2022, it retrenched to about $1.26 billion in FY2025 due to intensified investment cycles [F1]. Meanwhile, net income exhibits pronounced swings influenced by various factors including tax treatment or one-offs—rising sharply to over $1 billion in the latest period [F1].

Operating cash flow shows an encouraging upward trend from about $542 million in FY2024 to more than $1.59 billion in FY2025 [F1]. Capital expenditure levels are stable near $260 million annually reflecting investment into capacity and technology renewal plans [F1]. Share repurchases remain a focal point of capital return strategy totaling roughly $893 million for FY2025 after exceeding $1.15 billion the prior year [F1]. Equity base expanded substantially driven by earnings retention.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 1074 | 1595 | 1264 | 260 | +178.4% |

| 2024 | 386 | 542 | 1379 | 252 | -72.5% |

| 2023 | 1402 | 896 | 1534 | 253 | |

| 2022 | 1218 | 1749 | 245 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 893 | 1335 | 10.4 |

| 2024 | 1159 | 290 | 3.9 |

| 2023 | 880 | 643 | 21.1 |

| 2022 | 1727 | 974 |

Source: SEC companyfacts cache [F1].

Note: Revenue figure for previous years beyond FY2017 not fully available; growth rates are based on latest disclosed data [F1].

Growth Drivers & Future Outlook

The company’s future expansion hinges on:

- Continued innovation pipeline success especially trials advancing less-invasive TMTT indications which promise to unlock larger patient cohorts.

- Geographic expansion particularly ramping up adoption outside the U.S., aligning with demographic trends towards aging populations worldwide.

- Increasing procedural volumes driven by greater clinical awareness coupled with improved reimbursement frameworks that facilitate hospital uptake.

- Adoption of digital tools such as integrating GenAI for surgical planning or post-procedure monitoring as hinted by industry outlooks referencing medtech firms adapting AI technologies [N10].

Conversely, growth could be capped due to:

- Regulatory delays or denials given that approvals require costly clinical validation under stringent FDA or EU Medical Device Regulation standards [S4][S6].

- Competitive pressure from peers like Medtronic or Abbott who wield broad device portfolios potentially eroding pricing power.

- Supply chain fragilities amplified by geopolitical tensions impacting critical raw materials sourced globally for biological tissue valves or electronics components [S5][S6].

- Patent litigation risks which may require costly legal resources diverting focus from product development [S7].

Forecasts & Milestones to Watch

While no explicit forward guidance is provided in the current filings,[N3][N4], investors should monitor the following triggers:

- Clinical trial readouts or FDA panel reviews pertinent to upcoming product launches.

- Quarterly sales momentum data indicating uptake trends particularly in emerging international markets.

- Regulatory agency notifications concerning approval timelines or recalls.

- Capital deployment announcements such as R&D spending increases or acquisitions signaling expansion prioritization.

- Market share shifts relative to competitors’ product introductions.

Financial Returns & Capital Allocation

Edwards Lifesciences showcases a solid return profile anchored by efficient capital use:

- Approximate Return on Equity (ROE) stood near 10.4% for FY2025 calculated as net income over equity reported at about $10.34 billion—both figures derived from latest annual report data [F1].

- Strong operating cash flow generation at

$1.6 billion exceeded capital expenditures ($260 million), yielding substantial free cash flow estimated around $1.33 billion facilitating debt management and shareholder returns [F1][S18]. - Share repurchase programs remain significant; $893 million deployed during FY2025 indicates a clear focus on moderating share count without explicit dividend information disclosed [F1][S12][S16].

- Maintaining a robust liquidity position with cash & equivalents reported at $2.94 billion offers flexibility for opportunistic investments or buffering macroeconomic shocks [F1][S17].

Competitive Moat & Industry Positioning

Edwards’ leadership benefits from several defensible moats:

- Market dominance with widely recognized branded products underpinning structural heart therapy solutions.

- Extensive clinical training initiatives fostering high physician proficiency that strengthens customer loyalty and sets usage standards difficult for competitors to rapidly replicate.

- Regulatory certifications demonstrate consistent compliance assuring hospitals of safe long-term device reliability.

- Intellectual property rights strategically guarded through patents cross-licensed or defended via litigation maintaining technological edge.[S7]

- A well-established global sales network balanced between direct forces in key regions complemented by distributors tailored for less mature markets.[S5]

- Strategic collaborations within healthcare ecosystems facilitate integrated solutions addressing evolving clinician needs.

Risks & Considerations

Key risk vectors reside chiefly around:

- Innovation risk inherent with medical technology where unsuccessful trials can impair pipeline value.

- Regulatory risks stemming from complex approval frameworks requiring time-consuming submissions.

- Competitive dynamics pressured by entrenched rivals deploying aggressive marketing or pricing tactics.[S8]

- Supply chain disruption potential heightening vulnerability given reliance on unique raw materials like animal tissues essential for biologic valves.[S5]

- Legal exposure linked to product liability or intellectual property disputes that could translate into financial losses.[S4][S23]

- Macroeconomic factors influencing healthcare budgets affecting reimbursement schemes crucial for procedure demand.[S20]

Conclusion

Edwards Lifesciences stands poised as one of the foremost players shaping structural heart disease treatment today through relentless innovation backed by sound financial stewardship. Its historical strength evident in top-line growth paired with robust cash flow affords the ability to invest heavily into R&D while returning capital judiciously via buybacks though operating profitability has faced headwinds recently given intensified investments. The trajectory forward will largely hinge on navigating regulatory pathways successfully along with maintaining competitive differentiation amid rising industry complexity that demands nimble adaptation across manufacturing logistics and clinical engagement practices.

This analysis is based on publicly available financial statements, SEC filings dated through February 25, 2026 ([S1]-[S29]), recent news excerpts from February 2026 ([N1]-[N14]), and company facts data ([F1]) without any projection beyond disclosed figures or speculative guidance interpretations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments