Ford Motor Company 2026: Navigating Electrification Amid Competitive and Financial Challenges

Ford remains a pivotal global automaker balancing traditional strengths with a strategic pivot to electrification amidst market headwinds.

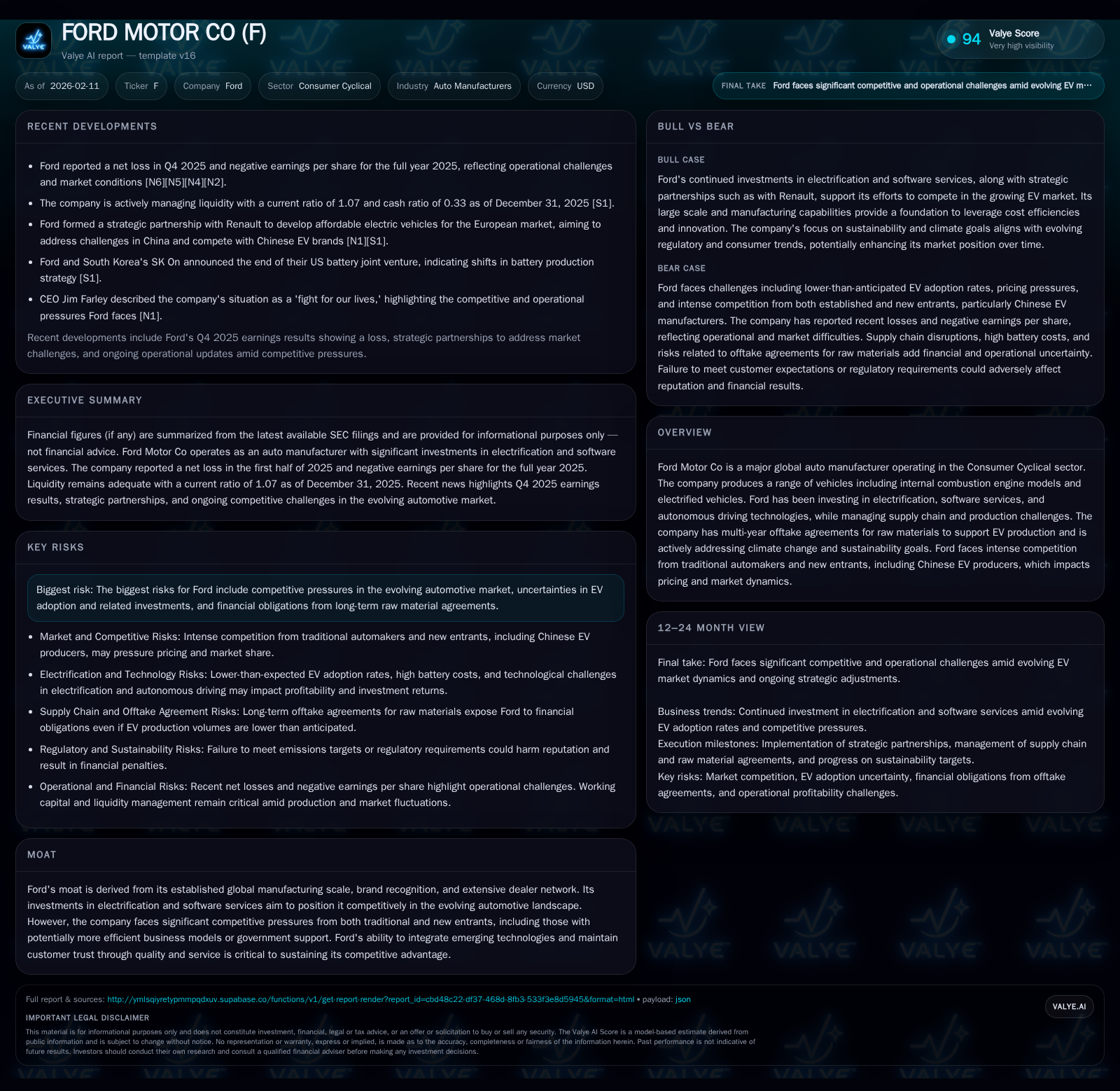

Ford Motor Co, a century-old automotive giant, is managing the transition from internal combustion engines to electrified vehicles and software-driven services in a fiercely competitive global landscape. Despite missing recent earnings estimates and facing declining revenue year-over-year, Ford's strong brand, scale, and dealer network provide a moat. The company’s significant investments in EV technology and raw material offtake agreements highlight its commitment to electrification, though slower-than-expected EV adoption and evolving regulatory frameworks pose risks. Operational complexities including supply chain challenges and working capital management remain critical factors impacting cash flow and profitability as Ford navigates this transformative period.

Overview: Legacy Meets Transition

Ford Motor Company stands as one of the most resilient players in the global automotive industry. With roots stretching back over a century, it epitomizes mass manufacturing scale, an iconic brand portfolio, and an unparalleled dealer network. Yet today’s automotive market is in a historic transition—from gasoline-powered vehicles toward electrification and software-integrated mobility solutions—pressuring Ford to adapt rapidly while managing legacy complexities.

Financial Performance Snapshot

As of December 31, 2025, Ford reported annual revenue near $185 billion (representing stable top-line scale) yet experienced a net loss for the first half of 2025 (-$36 million), signaling emerging profit pressures amid transformation [F1]. The Q4 2025 earnings release notably missed Wall Street expectations on both EPS and revenues with investors closely watching operational execution indicators [N2][N7]. Despite this, Ford’s stock price showed resilience post-earnings due partly to investor confidence in long-term strategy execution and robust cash balances totaling $23.4 billion at year-end [N1][F1]. The current ratio of approximately 1.07 underscores adequate near-term liquidity but highlights tight working capital management dynamics still at play [F1].

Strategic Shift Toward Electrification & Technology

In response to increasing environmental regulations worldwide and shifting consumer preferences, Ford has committed substantial investment into electrification pathways—and while it continues to offer internal combustion engine (ICE) models across several segments including pickups and SUVs, the emphasis on plug-in hybrids and battery electric vehicles (BEVs) is accelerating. However, in late 2025 Ford strategically scaled back certain EV spending initiatives to reallocate capital toward higher-return areas amid slower-than-anticipated EV adoption rates industrywide [S1]. This cautious rebalancing reflects an adaptive stance given uncertain regulatory incentives—most notably subdued government support for EVs in the U.S. in 2025—and evolving fuel economy standards.

Ford's footprint in software-enabled services is also growing; connectivity solutions, over-the-air (OTA) updates for vehicle systems, digital service offerings, and autonomous driving technologies constitute critical pillars of its future revenue streams. This landscape is highly competitive with traditional OEMs expanding their technological capabilities while newer entrants—especially from China—benefit from government backing or innovative business models that challenge overhead structures of incumbents like Ford [S1].

Supply Chain & Offtake Agreements

To secure critical inputs essential for battery production such as lithium, nickel, cobalt, and other materials, Ford has entered multi-year offtake agreements ensuring steady access amid global raw material constraints. These arrangements mitigate supply disruption risks but introduce financial obligations that may strain cash flow if demand forecasts misalign or if raw material pricing fluctuates markedly. Further complicating cash conversion cycles are working capital dynamics; Ford notes that typical supplier payment terms extend approximately 45 days while receivables remain relatively low due to wholesale financing via Ford Credit—a setup helping short-term liquidity but vulnerable to production stoppages or volume fluctuations [S1][S2].

Additionally, Ford may stockpile inventory proactively against supplier shortages—a tactical buffer that can temporarily inflate working capital needs and depress free cash flow despite overall operational viability.

Competitive Dynamics

The automotive sector's competitive intensity remains elevated. Traditional manufacturers continue ramping EV offerings globally while cost structures often reflect decades-old plants requiring modernization investment. New competitors abound: Tesla's scale benefits persist; Chinese manufacturers aggressively expand internationally leveraging favorable capital access and governmental partnerships; technology startups push autonomous vehicle innovations.

Ford is positioned firmly due to its brand strength—especially in trucks where loyalty runs high—and integrated dealership networks that facilitate customer engagement beyond transactional sales. Yet it must continuously innovate product portfolios aligned with consumer tastes for electrification without eroding margins excessively or diluting market share through dated ICE vehicle inventories.

Reputation & Consumer Sentiment Risks

Increased customer interconnectedness via online platforms enhances transparency but also fast-tracks reputational risk—unfounded allegations concerning safety or environmental impact can have outsized effects on consumer buying decisions.

Hence Ford’s ability not only to build quality products but also promptly address issues through OTA software updates or rapid recalls will be crucial. Customer trust remains a non-tangible yet potent asset influencing retention rates especially as product complexity rises.

Environmental Commitments & Regulatory Landscape

Ford publicly supports climate goals aligned with international accords such as the Paris Agreement. It has adopted interim targets for carbon emission reduction validated by recognized bodies like the Science Based Targets initiative (SBTi). However, achieving these goals necessitates continuous investments in cleaner technologies across vehicle lines and supply chains.

Aside from technical hurdles, regulatory frameworks remain fluid—with some jurisdictions dialing back incentives or modifying fuel efficiency mandates—which introduces planning uncertainty affecting long-term strategic investments.

Failure to meet emission targets could adversely impact brand reputation among environmentally conscious consumers as well as trigger penalties or restrict market access in key regions.

Cash Flow & Capital Allocation

From an operational finance perspective, Ford reported adjusted free cash flow improving year-over-year partly driven by enhanced working capital management including timely payables despite headwinds on reduced wholesale volume growth during Q4 2025 [S2]. Capital expenditures remain sizable though slightly reduced relative to prior periods as investment priorities shift toward electrification technologies rather than broad-scale capacity expansion.

Shareholder distributions continue steadily while restructuring charges have diminished recently reflecting stabilization efforts post-pandemic disruptions.

Outlook Considerations & Risks Summary

Key risks identified encompass:

- Intensifying competition compromising market penetration or margin structure,

- Changing consumer acceptance rates for electrified vehicles potentially undermining return on invested capital in EV programs,

- Financial exposure from committed raw material purchase agreements independent of actual production volumes,

- Operational disruptions due to supplier constraints affecting manufacturing cadence,

- Reputational damage linked to product quality or sustainability targets missed,

- Regulatory volatility imposing compliance cost escalations or limiting eligible markets.

Ford’s progress over coming years will hinge on harmonizing product innovation responsiveness with operational discipline and financial prudence.

Conclusion

Ford Motor Company stands at a crossroads emblematic of the automotive industry's broader evolution: leveraging its unmatched legacy assets while betwixt uncertain environment shifting decisively toward cleaner propulsion systems and digital services. Its established scale offers resiliency against economic cycles; however, sustained success demands deft management of competing priorities—from supply chain intricacies through reputation safeguarding—amid accelerated technological disruption.

This analysis reflects data available up through early 2026 documents alongside public disclosures since late 2025 capturing current company context without predictive guidance.

Disclaimer: This report is for informational purposes only and does not constitute investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments