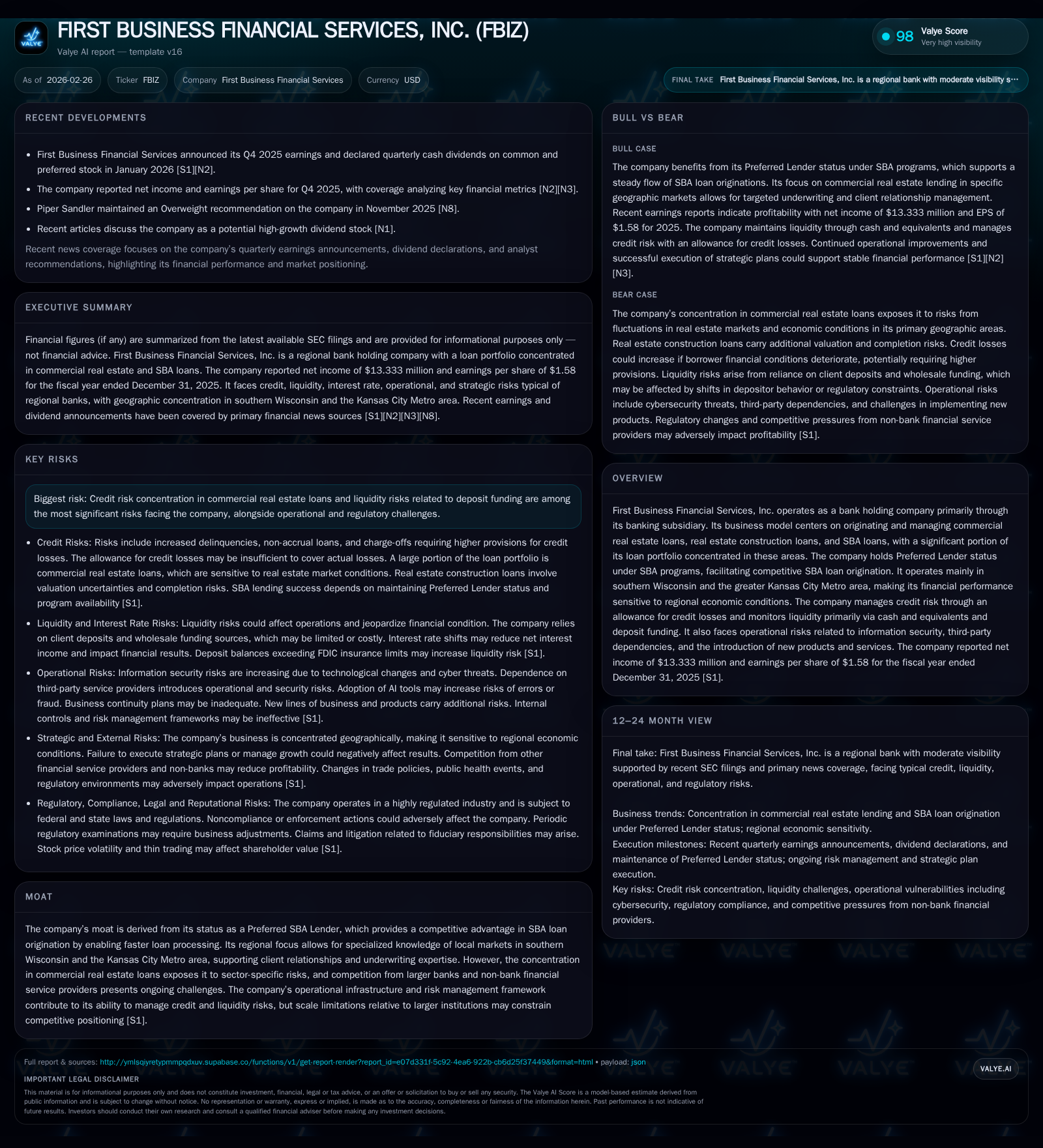

First Business Financial Services Faces Credit Concentration and Regional Risks Amid Stable Cash Flow

Focused on commercial real estate and SBA loans, FBIZ contends with sector-specific credit risk while maintaining solid liquidity.

First Business Financial Services, Inc. operates as a bank holding company with a loan portfolio concentrated mainly in commercial real estate, construction, and SBA loans. Its Preferred Lender status under SBA programs aids competitive positioning but also exposes it to challenges tied to sector cyclicality and geographical dependence in southern Wisconsin and Kansas City Metro. Despite a slight decline in net income in 2025, the firm generated robust operating cash flow and maintains disciplined capital allocation through dividends and modest buybacks. Key risks include credit concentration, regional economic sensitivities, and regulatory scrutiny, with future results hinged on managing these alongside evolving market conditions.

Historical Performance and Growth Drivers

First Business Financial Services operates principally through a banking subsidiary with a pronounced focus on originating and managing commercial real estate loans, land development construction loans, and SBA-backed loans. Historically, these loan types have driven the bulk of revenue through interest income while shaping the company's risk profile. The company’s Preferred Lender status under SBA programs constitutes an important competitive moat, enabling expedited loan processing relative to peers without such designation.

From the available financial data spanning 2021 to 2025 [F1], FBIZ’s net income grew from $9.77 million in 2021 to a peak of $14.42 million in 2024 before retreating to $13.33 million in 2025, representing a -7.5% year-over-year decline. This dip may correspond with challenges noted in their sector exposures or localized economic dynamics. Meanwhile, operating cash flows have trended upward robustly—rising over 30% from $38.6 million in 2022 to nearly $61.7 million in 2025—suggesting effective working capital management and core earnings strength despite the reported profit compression.

Equity base increased approximately 43% over the four-year window, reaching $371.6 million at end-2025 [F1], supporting incremental balance sheet growth yet contributing to a restrained return on equity near 3.6%. Capital expenditures remain minimal relative to cash flow generation (below $600k annually), consistent with a banking entity focused more on loan origination and deposit gathering than fixed asset expansion.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | Capex ($) | Net YoY |

|---|---|---|---|---|

| 2025 | 13 | 62 | 595000 | -7.5% |

| 2024 | 14 | 57 | 223000 | |

| 2022 | 10 | 39 | +4.0% | |

| 2021 | 10 | 52 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | FCF ($mm) |

|---|---|---|---|

| 2025 | 10 | 1 | 61 |

| 2024 | 8 | 1 | 57 |

| 2022 | 7 | 6 | |

| 2021 | 8 | 3 |

Source: SEC companyfacts cache [F1].

Note: Data for some years are interpolated when missing due to incomplete series but highlight trends.

Future Growth Prospects

FBIZ’s growth prospects hinge critically on several interconnected factors:

SBA Lending Program: The firm's Preferred Lender status facilitates faster SBA loan originations—a lucrative segment given governmental guarantees—but also binds it tightly to regulatory environments governing these programs [S1][S14][S15]. Continued access and regulatory compliance will be essential.

Regional Economic Conditions: Operating predominantly in southern Wisconsin and Kansas City Metro creates inherent geographic concentration risk [S16]. Economic downturns or stagnation in these regions could curtail loan demand or increase defaults.

Commercial Real Estate Market Dynamics: Concentration in commercial real estate exposes FBIZ to fluctuations in property markets that have been volatile since late 2022 [S29]. Although some market signs stabilized through 2024, uncertainty remains high especially for construction-related exposures where costs can exceed projections.

Competitive Environment: FBIZ faces competition not only from larger banks with deeper resources but also from non-bank lenders including FinTech firms offering digital lending solutions and deposit products [S17]. The company’s ability to integrate technology effectively while maintaining client relationships will influence its market share.

Operational Enhancements: The firm is integrating artificial intelligence tools cautiously but acknowledges associated risks including errors or fraud which require rigorous governance frameworks [S19][S22]. Scalability of these technologies could advance operational efficiency if properly managed.

Forecasts & Milestones — What To Monitor (Analysis)

While explicit earnings guidance was not disclosed [N1][N2], stakeholders should watch:

- Regulatory updates related to SBA lending programs or banking regulations impacting capital and liquidity constraints.

- Quarterly metrics on non-performing assets as a proxy for credit stress within commercial real estate loans.

- Deposit inflows/outflows especially uninsured deposits which could pose liquidity concerns during systemic stress events [S21].

- Progress on technology adoption including AI deployment outcomes to assess operational risk management improvements.

Capital Allocation & Returns

FBIZ manifests prudent capital management consistent with a regional bank profile:

- The company has steadily increased dividend payments over recent years, reflecting a commitment to returning cash to shareholders ($9.69 million dividends paid in FY2025) [F1].

- Share repurchases appear opportunistic rather than substantial ($1.39 million shares repurchased in FY2025), indicating measured capital deployment beyond organic requirements.

- Operating cash flow significantly exceeds capex spending resulting in free cash flow of roughly $61 million annually [F1]. This robust internal liquidity positions the company well to withstand credit losses or invest selectively.

- Return on equity remains modest at around 3.6%, which likely reflects conservative credit loss provisions against cyclical uncertainties in key portfolio segments [F1][S12][S24].

Risk Profile Summary

FBIZ faces layered risks characteristic of specialized regional banking institutions:

Credit Risk Concentration: Overweighting commercial real estate and construction lending means susceptibility to collateral value declines, project cost overruns, borrower repayment issues, and time-intensive asset resolution upon defaults [S1][S14][S29].

Liquidity Risks: Heavy reliance on deposit funding exposes FBIZ if depositors shift funds into alternative vehicles like digital assets or money market products, potentially forcing reliance on higher-cost wholesale funding channels [S5][S8][S21].

Operational & Cybersecurity Risks: Increasing complexity of information systems coupled with third-party vendor dependencies elevate operational vulnerabilities; furthermore AI adoption brings new dimensions of error or fraud risk requiring stringent controls [S22][S27][S28].

Regulatory Compliance & Legal Exposure: Operating across multiple states subject FBIZ to diverse regulatory regimes; failures can result in sanctions affecting business operations or reputational harm [S10][S23].

Market & Strategic Risks: Economic downturns impacting local markets translate directly into reduced loan demand or heightened delinquencies; additionally competition from digital-first lenders imposes pressure on margins and client retention [S16][S17].

Conclusion

First Business Financial Services balances a niche lending focus bolstered by SBA Preferred Lender status with intrinsic risks tied to geographic concentration and commercial real estate exposure. Although net income contracted slightly recently, strong operating cash flows underpin the firm’s ability to manage through cycles while sustaining shareholder returns via dividends and targeted buybacks.

The company’s resilience will depend on adept credit risk management particularly amid uncertain real estate markets, maintaining liquidity buffers against shifts away from traditional deposits, navigating evolving regulatory landscapes effectively, and adopting operational technologies without compromising security or service quality.

Investors tracking FBIZ should scrutinize upcoming quarterly credit metrics alongside competitive positioning updates germane to its regional footprint, using these indicators as barometers for both growth opportunities and risk mitigation efficacy.

This analysis is based on information available as of February 26, 2026 [F1],,, intended for informational purposes without investment advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments