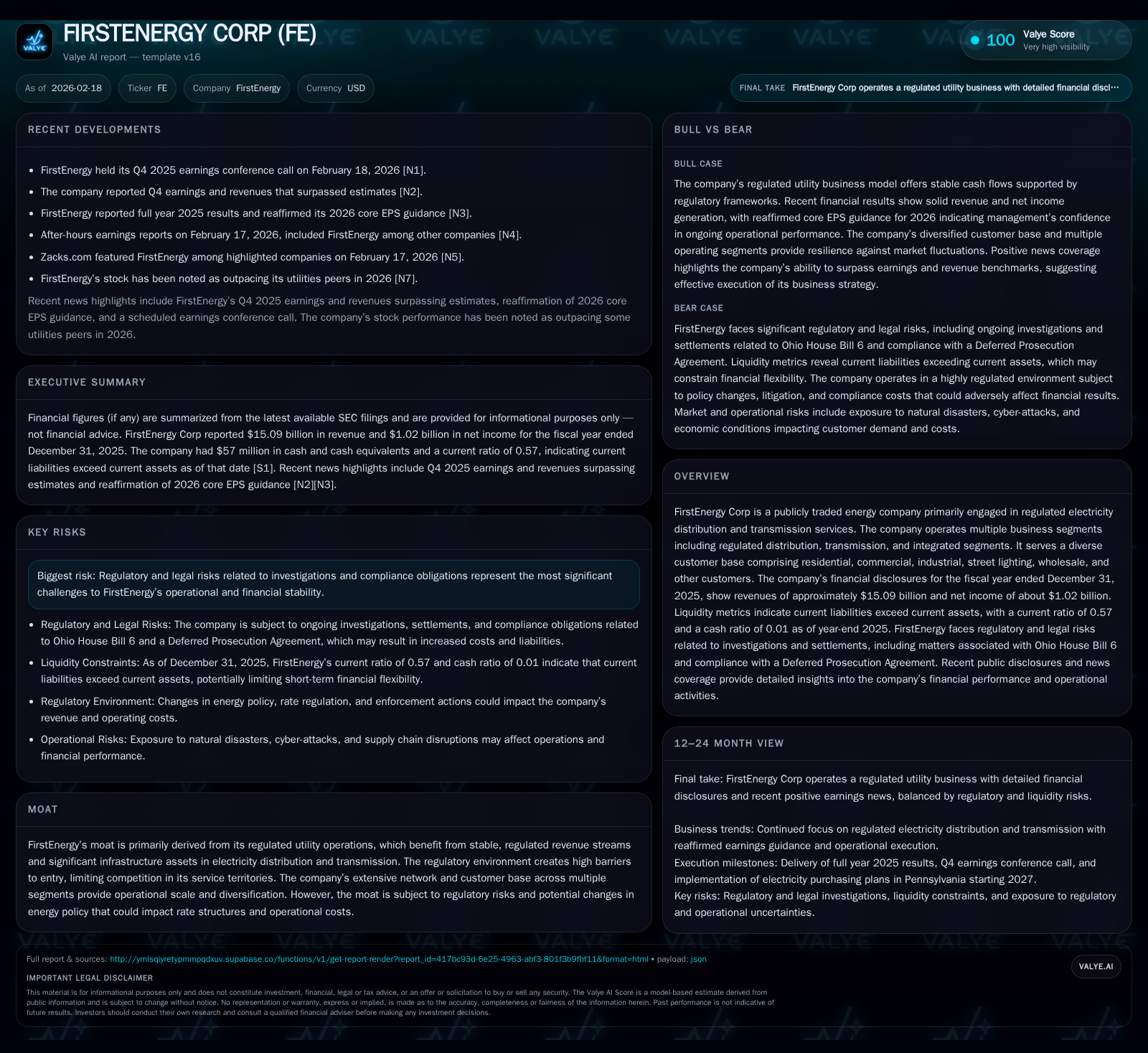

FirstEnergy Corp's Financial Rebound and Regulatory Challenges in 2025

An analysis of FirstEnergy Corp’s financial performance juxtaposed with ongoing regulatory and legal risks shaping its outlook.

FirstEnergy Corp posted solid revenue growth in 2025 driven primarily by its regulated distribution and transmission segments, yet operating income contracted due to elevated costs and regulatory headwinds. The company continues to grapple with legacy legal challenges linked to Ohio House Bill 6 investigations, which contribute to higher operational margin volatility and cost of capital. Capital allocation remains disciplined with steady dividends but no share buybacks amid heavy infrastructure investment and negative free cash flow. Investors should monitor rate case outcomes and compliance-related milestones as key indicators of future financial stability.

Revenue and Profitability Growth Trajectory Through 2025

FirstEnergy Corp demonstrated robust top-line expansion over the four-year period ending FY2025. Revenues climbed from $12.46 billion in 2022 to $15.09 billion in 2025, marking a compounded surge fueled predominantly by increased rates and volume growth within regulated electricity services [F1]. Year-over-year (YoY) growth was particularly pronounced in FY2025 at 12%, significantly higher than the preceding years' range (4-8%).

Operating income conversely exhibited a less consistent path. While it increased notably between FY2022 ($1.91 billion) and FY2024 ($2.38 billion), a contraction to $2.21 billion in FY2025 reflected pressures from growing operational costs, including storm restoration expenses, higher wages, and legal compliance costs tied to ongoing investigations [F1][S14]. This decoupling between revenue and operating income underscores rising expense burdens squeezing margins.

Net income showed a more measured recovery trajectory, nearly doubling from $406 million in FY2022 to over $1 billion in FY2023 and stabilizing around that mark through FY2025, with a slight increase of approximately 4.3% from FY2024 levels [F1]. This suggests some mitigation from non-operating factors or tax adjustments cushioning bottom-line impact.

Historical performance (annual)

| FY | Rev ($bn) | Net ($mm) | CFO ($bn) | OpInc ($bn) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 15.1 | 1020 | 3.7 | 2.2 | +12.0% | +4.3% |

| 2024 | 13.5 | 978 | 2.9 | 2.4 | +4.7% | -11.3% |

| 2023 | 12.9 | 1102 | 1.4 | 2.3 | +3.3% | +171.4% |

| 2022 | 12.5 | 406 | 2.7 | 1.9 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Capex, Buybacks. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 1016 | -1005 | 8.2 |

| 2024 | 970 | -1139 | 7.9 |

| 2023 | 906 | -1969 | 10.6 |

| 2022 | 891 | -73 | 4.0 |

Source: SEC companyfacts cache [F1].

Note: Free Cash Flow omitted due to negative values; Buybacks excluded due to no recent activity.

Segment Contributions Driving Historical Performance

FirstEnergy’s financial results draw heavily on its regulated distribution and transmission segments, both underpinning the company’s value moat characterized by regulated revenue streams insulated from market competition [S4][S5][S6][S7][F1]. The regulated distribution segment serves a broad customer base encompassing residential, commercial, industrial, street lighting, wholesale, and other users—providing both volume stability and pricing flexibility through rate cases.

The transmission segment benefits from scale economies linked to significant infrastructure assets delivering electricity across multiple states under long-term contracts or regulated tariffs [S8]. These assets entail high barriers to entry for competitors due to capital intensiveness and regulatory protections.

The integrated segment complements these regulated businesses via generation assets predominantly servicing internal needs rather than open-market sales.

Collectively, these segments contribute to a diversified revenue mix reducing overall business volatility while enabling stable earnings predictability typical of utility operations.

Regulatory Environment and Legacy Legal Issues Impacting Operations

A notable challenge clouding FirstEnergy’s operational landscape arises from ongoing regulatory scrutiny related particularly to Ohio House Bill 6 controversies dating back several years [S14][S22][S27]. Investigations into potential improprieties have resulted in settlements, compliance obligations under Deferred Prosecution Agreements (DPA), and heightened monitoring that elevate both direct expense lines and implied risk premiums.

From a utility sector perspective, such litigations tend to increase the company's cost of capital as regulators and investors demand greater risk premiums amid uncertainty [S14]. Furthermore, earnings volatility may emerge given possible fines, restitution charges, or mandated escalated investments in governance frameworks impacting operational margins.

Compliance also requires resource-intensive reporting disclosures alongside stakeholder engagement—all contributing indirectly but materially to operational expenditures.

These factors crystallize as strategic impediments constraining management flexibility while shaping forward-looking rate case considerations critical for revenue adequacy.

Future Growth Drivers Amidst Policy and Market Constraints

Looking ahead, FirstEnergy projects stable core earnings per share growth in fiscal year 2026 following reaffirmation of guidance during its Q4-25 earnings conference call [N1][N3]. Growth drivers center on sustained infrastructure investment initiatives exemplified by the Energize365 program targeting transmission & distribution upgrades [S14].

However, policy-driven constraints remain significant as evolving energy regulations impose tighter emissions standards and renewable integration requirements potentially increasing compliance costs.

Capital expenditures are expected to rise further as management seeks modernization of aged grid components coupled with resilience enhancements against severe weather risks exacerbated by climate change considerations [N3][S14]. This capex intensity weighs on free cash flows but supports longer-term rate base growth essential for stable utility returns.

Market dynamics such as customer demand patterns shifting toward electrification also support incremental volume upside albeit moderated by economic uncertainties influencing load growth trajectories.

Thus growth exhibits a balance between rate base expansion opportunities tempered by regulatory cost controls—a familiar tradeoff in regulated utility frameworks.

Financial Forecast and Key Milestones For The Upcoming Year

While explicit numeric guidance beyond core EPS affirmation is limited [N3], investors should closely monitor forthcoming rate case outcomes critical for setting authorized returns on equity—elements that directly impact valuation multiples and profitability visibility.

Key milestones also include ongoing updates related to regulatory compliance reports stipulated under DPA terms along with resolution schedules for any residual Ohio HB6 litigation aspects still active as per the latest disclosures [N3][S22].

Operational metrics such as storm restoration expense trends will remain watchpoints given their historical capacity for episodic margin shocks influencing quarterly results.

Overall credit rating evaluations following regulatory developments represent another barometer for assessing financing cost implications throughout the year.

Capital Allocation: Dividend Policy, Share Buybacks, and Investment Priorities

FirstEnergy demonstrates a classic utility-style capital allocation approach characterized by steadily increasing dividends without share repurchases reported since at least FY2009 [F1][S19][S23]. Dividends paid rose sequentially from $891 million in FY2022 to $1.02 billion in FY2025 reflecting confidence in sustainable cash flow generation despite capex-related free cash flow deficits.

Heavy investment spending averaging around $4–$5 billion annually limits excess liquidity available for buybacks or debt reduction beyond scheduled maturities [F1]. Return on equity approximates a modest ~8%, aligned with industry norms emphasizing consistent income streams over aggressive profitability expansion.

Such policies underscore a disciplined balance prioritizing infrastructure renewal necessary for regulatory compliance alongside maintaining shareholder distributions deemed appropriate for utility-grade risk profiles.

Cash Flow Dynamics and Balance Sheet Resiliency

Operating cash flows surged approximately +28% YoY reaching $3.7 billion in FY2025 supporting ongoing capital expenditures which rose about +17% to nearly $4.71 billion [F1]. The resulting negative free cash flow near −$1 billion indicates external financing needs likely met through debt issuances given historical capital structure patterns [S9][S10][S11][S13].

Balance sheet assessments reveal current liabilities exceeding current assets yielding a low current ratio of roughly 0.57 at year-end reflecting relatively tight short-term liquidity cushions pictured by a meager cash ratio near zero ($57 million cash vs $5.27 billion current liabilities) [F1][S29]. These figures suggest active working capital management is crucial amid elevated payables or upcoming debt maturities—but do not imply immediate distress given robust operating cash inflows.

Long-term indebtedness remains high consistent with capital intensive business models typical among utilities; however, stable regulated cash flows substantiate debt servicing capacity assuming no major adverse regulatory shifts occur [S16][S21].

Risks Spotlight: Investigations, Compliance Obligations, and Their Financial Implications

Legal investigations tied primarily to Ohio HB6 present the most prominent risk factor impacting FirstEnergy's financial stability [S14][S22][S27]. These risks translate into uncertain liabilities including potential penalty payments or mandated remedial programs which carry both direct costs and reputational repercussions potentially constraining future rate case negotiations.

Utility sector experience indicates that extended compliance regimes often elevate administrative overheads disproportionately relative to revenues—thus compressing margins intermittently while increasing cost of capital demands among investors skeptical of regulatory settlements completeness.

Ongoing vigilance is warranted regarding updates on litigation outcomes alongside enforcement actions embedded within DPAs as their failure or delay could trigger renewed scrutiny increasing volatility.[S14]

Complementary risks stem from macroeconomic shifts—including inflationary cost pressures on fuel supply chains—and climatic event exposures heightening restoration expense unpredictability.[S22] These combined factors necessitate proactive risk mitigation embedded within strategic planning frameworks aimed at safeguarding financial resilience despite known uncertainties.

This report synthesizes FirstEnergy Corp’s publicly available disclosures as of February 18, 2026 without providing investment advice or price targets—intended solely for informational purposes grounded in official filings and reported news sources.[F1],[N1],[N3],

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments