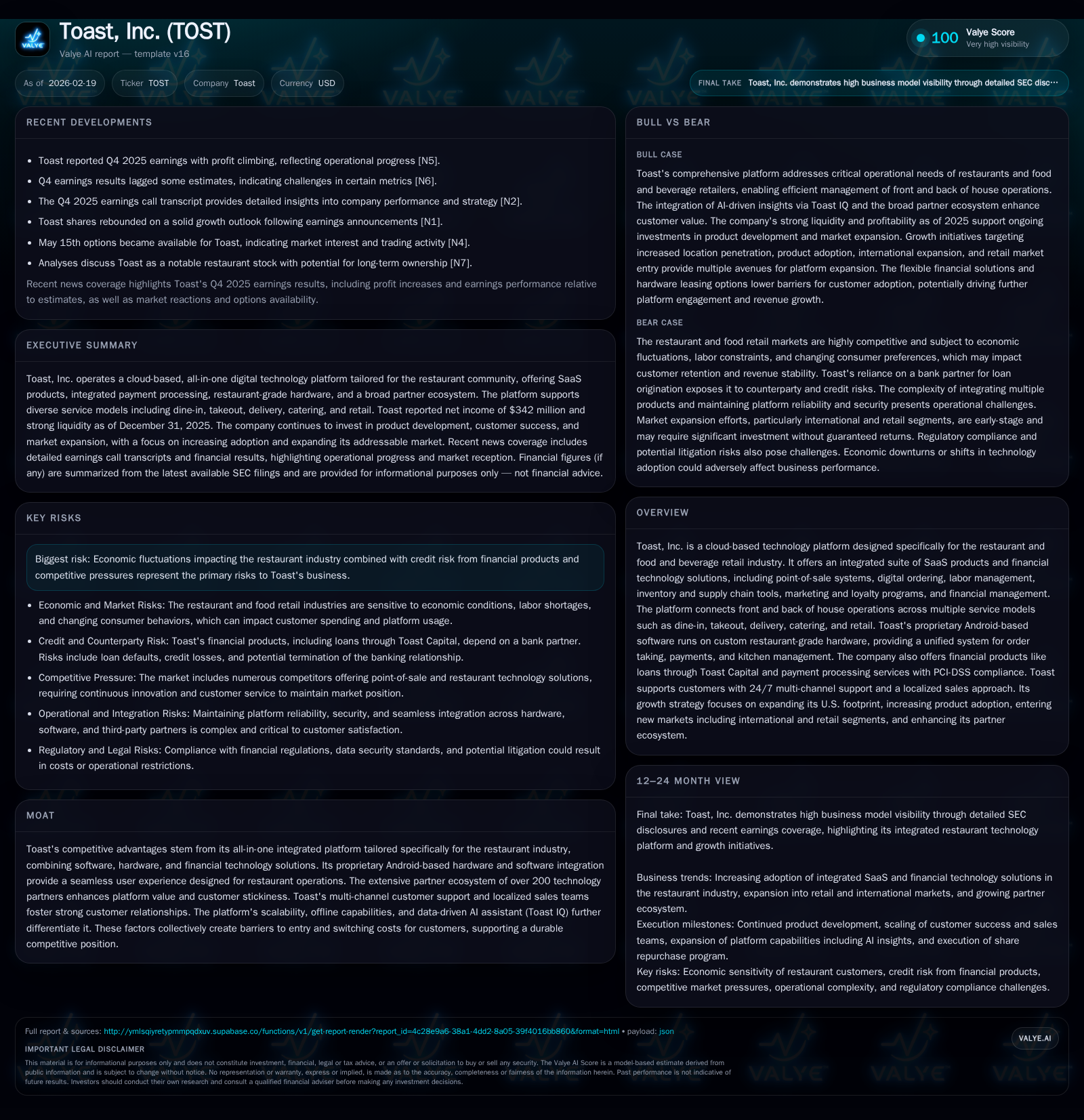

Toast, Inc. Surges to Profitability with Integrated Restaurant Tech Platform

Toast’s dramatic financial turnaround reflects its integrated SaaS, hardware, and fintech platform tailored to the restaurant industry.

Toast, Inc. has transitioned from several years of substantial operating losses to delivering strong profitability by fiscal year 2025, driven by growth in its integrated restaurant technology platform. The company’s proprietary Android-based software combined with custom restaurant-grade hardware and a broad fintech ecosystem has accelerated adoption across U.S. restaurant segments, now covering around 20% of the market. Despite promising growth prospects stemming from expanding platform adoption and new verticals, near-term risks include the cyclicality of the restaurant sector and credit exposure from financial products. Monitoring location footprint growth and cross-selling remains crucial for assessing the sustainability of this momentum.

Toast’s Profitability Turnaround: Historical Financial Performance

Toast’s financial trajectory over the past four fiscal years highlights a stark pivot from sizable losses to robust profitability. Operating income plummeted with losses of -$384 million in FY2022 but surged to a positive $292 million by FY2025 — a remarkable increase exceeding 1700% year-over-year between FY2024 and FY2025 alone [F1]. Net income followed suit, flipping from a loss of -$275 million in FY2022 to an earnings gain of $342 million in FY2025. Equally impressive is operating cash flow which saw an increase from a negative -$156 million in FY2022 to a robust $661 million in FY2025.

Capital expenditures remained modest relative to cash flows; reported capex was approximately $16 million as of FY2022 with no explicit data available for subsequent years [F1]. Meanwhile, stockholders' equity expanded significantly from about $1.1 billion in FY2022 to over $2.1 billion by FY2025, supporting operational scale-up. Return on equity (ROE), calculated as net income divided by equity for FY2025, stands at approximately 16.1%, indicating efficient use of capital alongside profitable operations.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Net YoY |

|---|---|---|---|---|

| 2025 | 342 | 661 | 292 | +1700.0% |

| 2024 | 19 | 360 | 16 | +107.7% |

| 2023 | -246 | 135 | -287 | +10.5% |

| 2022 | -275 | -156 | -384 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Rev, Capex, Div, FCF. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | ROE% |

|---|---|---|

| 2025 | 107 | 16.1 |

| 2024 | 56 | 1.2 |

| 2023 | -20.6 | |

| 2022 | -25.0 |

Source: SEC companyfacts cache [F1].

Note: Revenue figures are not available within provided tags; capex data post-2022 is not explicitly disclosed.

Key Drivers Behind Growth: Platform Integration and Market Penetration

Central to Toast’s turnaround is its holistic platform that integrates vertically through proprietary Android-based POS software paired with custom-built restaurant-grade hardware. This combination delivers more than simple ordering capabilities – it connects front-of-house activities like order taking with back-of-house processes such as kitchen management seamlessly on a unified stack [S5][S6][S8].

The technology suite spans payment processing compliant with PCI-DSS standards, digital ordering portals, labor management tools, inventory controls enhanced by predictive analytics via the AI-powered Toast IQ assistant, and marketing automation featuring guest loyalty programs [S11][S13]. This breadth creates high switching costs due to deep operational embedding.

Toast also maintains an ecosystem exceeding 200 technology partners across various domains including payroll, vendor management, reservations systems, security tools, and marketing platforms [S7][S19]. This external network supplements Toast’s native capabilities enhancing platform stickiness through cross-selling opportunities.

Sales teams emphasize localized knowledge—a critical advantage given food service's community-oriented purchasing patterns—facilitating penetration especially among SMB operators while steadily growing mid-market and enterprise accounts. Management estimates current U.S. market coverage approximates one-fifth of all restaurant locations served by Toast-powered systems [N8][S6].

Emerging Opportunities and Growth Constraints in Restaurant Tech

The addressable market remains expansive given many establishments still rely on legacy or disparate technologies ill-suited for today’s omnichannel commerce environment encompassing takeout, delivery partnerships, catering services, and direct retail extensions [S5][S8]. Long-term growth drivers include:

- Increasing adoption of digital ordering solutions as consumer expectations for seamless online experiences intensify.

- Upselling additional products within existing customer bases enabled by an integrated single-platform approach.

- Expansion into adjacent food and beverage retail verticals leveraging unified POS for hybrid operations merging restaurant services with retail sales.

- Selective international expansion initiatives remain early stage but represent substantial greenfield potential given limited current geographic footprint beyond the U.S. [S18][S21].

Challenges tempering opportunity size include:

- The highly cyclical nature of restaurants exposes revenues to macroeconomic shocks such as inflation-driven input costs and labor scarcity which may depress adoption or increase churn rates [S9][S10].

- Competitive pressures from other cloud POS providers specializing either solely in payments or specific operational silos might fragment wallet share.

- Credit risk arises primarily from Toast Capital’s working capital loans issued via banking partners; regulatory scrutiny or partner withdrawal could impair financing availability or terms [S24][S25].

Forward-Looking Insights: Earnings Outlook and Strategic Milestones

Public guidance remains limited but management expressed optimism during the Q4 earnings call regarding continued location footprint expansion and penetration into new verticals beyond traditional restaurants [N1][N8]. Analysts highlight key metrics including:

- Growth rates in customer count segmented by SMB versus enterprise levels.

- Cross-sell penetration indicated by average products adopted per customer.

- Progress against international market entry pilots.

- Platform uptime reliability underpinning customer satisfaction amidst scaling efforts [N14].

These indicators will be pivotal for validating sustainable momentum beyond fiscal year-end results.

Capital Allocation Strategy: Cash Flows, Buybacks, and Return on Equity

Cash flow generation underpins Toast’s strategic flexibility. Operating cash flow rose approximately 84% year-over-year to $661 million in FY2025 while capital expenditures remained moderate relative to scale—enabling free cash flow estimated near $645 million (operating cash flow minus capex) based on available data [F1][S4].

Toast currently does not pay dividends; however, share repurchases have increased substantially—from $56 million in FY2024 to $107 million in FY2025—reflecting confidence in returning value through buybacks rather than dividend payouts [F1]. The approximate return on equity at 16.1% suggests effective shareholder value creation alongside reinvestment into growth.

Product Innovation and Customer Success as Moat Builders

Toast maintains ongoing investment in research & development structured around full-stack cross-functional teams encompassing product management, engineering, design, data science, and analytics—ensuring rapid iteration closely aligned with operator needs [S4][S6]. Customer onboarding offers scalable options including on-site support supplemented by remote and self-guided implementations boosting retention likelihoods [S7].

Technological differentiators include offline POS continuity allowing order processing during internet outages via cellular backup embedded in handheld devices and routers—a critical reliability feature for busy venues facing connectivity challenges [S6]. These enhancements elevate user experience consistency further entrenching clients within the Toast ecosystem.

Risks Lurking in Toast’s Path: Industry Cyclicality and Credit Exposure

The restaurant industry’s inherent volatility—characterized by thin margins susceptible to inflationary pressures along supply chains and labor markets—accentuates business risk concentration for platform providers like Toast dependent on persistent operator viability [S9][S10]. Economic downturns often suppress discretionary spending impacting subscription renewals or product expansion cadence.

Financial product offerings expose Toast additionally to credit risks linked to loan performance under their Toast Capital program sourced through banking partners whose withdrawal or regulatory clampdown could rapidly curtail access [S24][S25]. Legal complexities related to lending statutes impose compliance burdens potentially leading to litigation or penalties if mismanaged. Competitive intensity from specialized SaaS vendors may compress pricing power or delay feature adoption cycles challenging revenue scalability further.

What Investors Should Watch Next

Qualitatively monitoring sustained new customer acquisition rates with an increasing mix towards higher-value mid-market/enterprise customers—who generally provide stickier revenue streams—is essential. Quantitative signals such as rising average module usage per location reflect deeper platform integration beyond basic POS provisioning. Tracking quarterly product updates spotlighting functional innovations or expanded partner integrations will provide insight into competitive positioning. Finally, disclosures hinting at international rollout timelines or partnership expansions beyond current ecosystems would mark significant strategic catalysts worth close attention.

This analysis relies exclusively on publicly available financial data and regulatory filings without extrapolation beyond provided facts or issuing investment advice. Readers should conduct independent due diligence before making financial decisions related to Toast, Inc.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments