Regal Rexnord’s Growth Accelerates Post-Divestiture Despite Supply Chain and Tariff Pressures

Following its 2024 industrial motors divestiture, Regal Rexnord reported robust 2025 results driven by data center demand and operational efficiency.

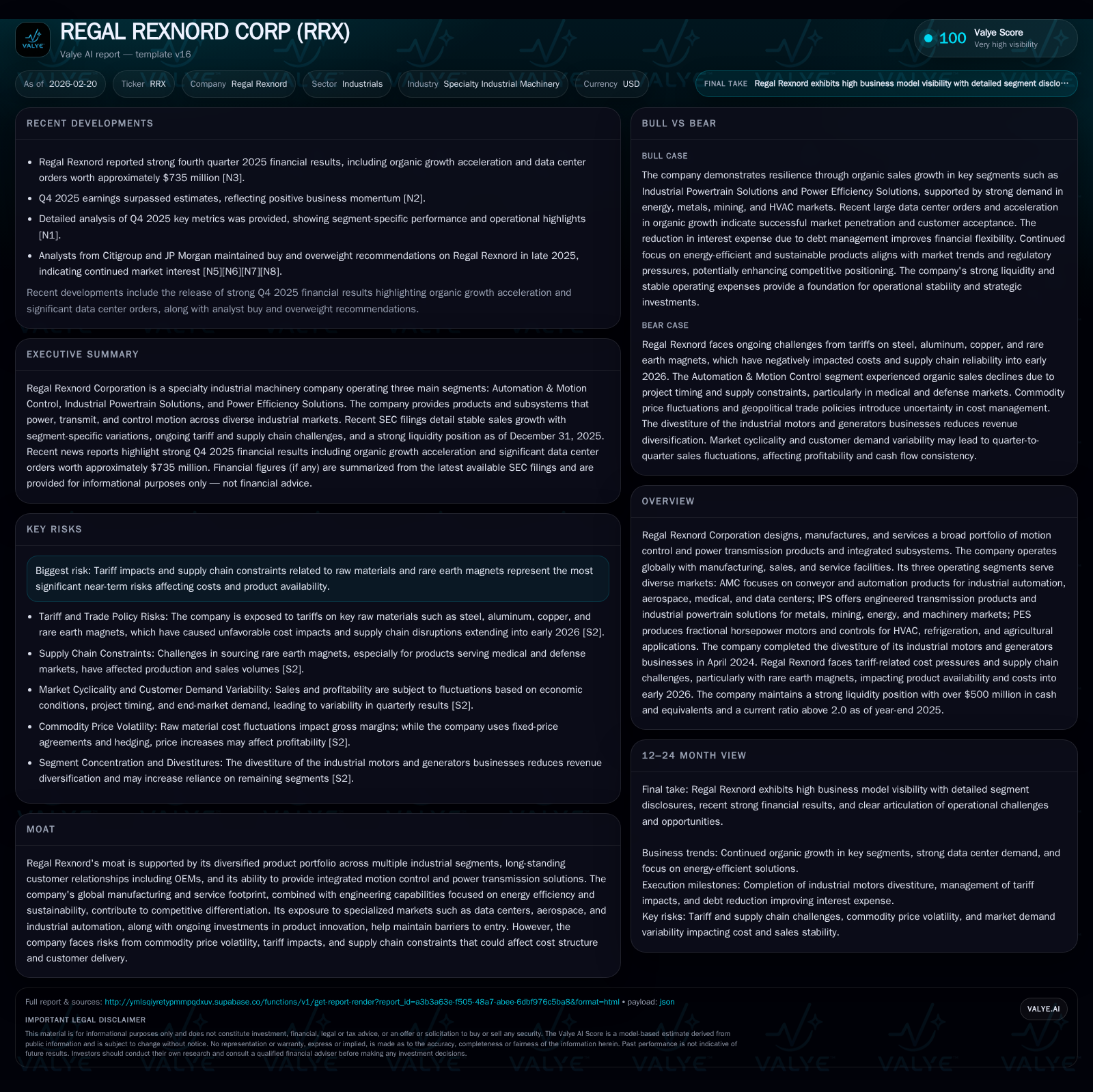

Regal Rexnord Corporation (RRX) has demonstrated strong financial performance in fiscal 2025, marked by an 8.1% operating income growth and a significant rebound in net income after prior-year setbacks. The company’s strategic divestiture of its industrial motors and generators business in April 2024 has sharpened its focus on three key segments—Automation & Motion Control, Industrial Powertrain Solutions, and Power Efficiency Solutions—which cater to diverse end markets including data centers, aerospace, and HVAC. While supply chain constraints—especially for rare earth magnets—and tariffs continue to apply cost pressures, organic growth drivers such as substantial data center orders (~$735 million) and ongoing innovation sustain promising revenue prospects. Capital allocation favors conservative buyback activity post-divestiture alongside robust free cash flow generation.

Company Overview and Industry Positioning

Regal Rexnord Corporation (RRX) operates as a global specialty industrial machinery player with a broad portfolio centered on motion control and power transmission products alongside integrated subsystems. Headquartered in Milwaukee, Wisconsin, the company’s operations span manufacturing, sales, and service worldwide across three core segments: Automation & Motion Control (AMC), Industrial Powertrain Solutions (IPS), and Power Efficiency Solutions (PES) [S1][S2]. These segments cover a wide range of industries—from aerospace precision components to data centers' conveyor automation systems—and end markets such as HVAC and agricultural applications.

The company’s moat arises from longstanding OEM relationships, diversified industrial exposures, technical engineering capabilities emphasizing energy-efficient solutions, and a footprint that supports global reach paired with tailored customer service . This multifaceted positioning helps shield it against entry threats but positions it exposed to external raw material volatility—including rare earth magnet shortages—and tariff-related cost risks that can compress margins or delay deliveries [S4][S5].

Historical Financial Performance

Regal Rexnord has experienced notable financial evolution over the past several years through strategic portfolio changes and market trends impact. A pivotal moment came with the September 2023 announcement and April 2024 completion of selling its industrial motors and generators businesses—previously the majority of the Industrial Systems segment—allowing sharper focus on higher-margin segments [S1].

Below is a summary of key annual financial metrics illustrating the trajectory through the divestiture period up to fiscal year-end December 31, 2025:

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 280 | 991 | 681 | 98 | +42.5% |

| 2024 | 196 | 609 | 630 | 110 | +441.8% |

| 2023 | -57 | 715 | 377 | 119 | -111.7% |

| 2022 | 489 | 436 | 690 | 84 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Rev, Div. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 0 | 893 | 4.1 |

| 2024 | 50 | 500 | 3.1 |

| 2023 | 0 | 596 | -0.9 |

| 2022 | 239 | 352 | 7.7 |

Source: SEC companyfacts cache [F1].

Note: Revenue figures are not fully available for recent years due to segment reclassification after divestiture; operating income trends better capture profitability shifts.

The company saw operating income fluctuate significantly through restructuring phases—from $690 million in FY22 down sharply then recovering—with an encouraging return to over $680 million in FY25 signaling improved operational leverage and cost control amid challenging macro conditions [F1][N1]. Net income mirrored this volatility but rebounded strongly in FY25 after multiple years hurt by integration costs and market cyclicality.

Operating cash flow improved markedly (+62.6% YoY) reaching nearly $1 billion in FY25 while capital expenditures contracted slightly (-10.8%), indicative of disciplined spending balanced between sustaining investments and avoiding overcapacity during uncertain cycles [F1][S6]. The lack of buybacks in FY25 contrasts with moderate repurchases before divestiture closure reflecting prudence amid repositioning efforts [F1][S7].

Business Segment Dynamics

Automation & Motion Control (AMC): This segment is central to Regal Rexnord’s strategy addressing conveyor systems automation—critical to data centers, industrial robotics, aerospace components, medical devices, among others [S2]. Recent earnings disclosures highlighted acceleration here due partly to robust orders from data centers (~$735 million worth) underscoring strong secular tailwinds for digital infrastructure investment [N1]. The demand-driven expansion is critical given AMC's higher margin profile within the broader portfolio.

Industrial Powertrain Solutions (IPS): IPS encompasses engineered transmission solutions serving metals/mining industries plus energy sectors often tied to cyclical capex patterns [S2]. While sizable historically, IPS margins are sensitive to commodity prices and tariff fluctuations impacting component costs including bearings, gearboxes, and industrial powertrain assemblies.

Power Efficiency Solutions (PES): The PES segment focuses on fractional horsepower motors catering primarily HVAC/refrigeration/agriculture markets where energy efficiency regulations increasingly drive incremental demand for variable speed motor controls and integrated subsystems [S2]. Despite mature end-markets, regulatory shifts toward electrification provide steady growth support.

Forward-Looking Growth Prospects

Looking ahead into early fiscal years post-2025 reporting:

- Data centers remain a major catalyst given sustained investment cycles driving automation upgrades requiring conveyor and power transmission subsystems integral to AMC growth [N1].

- Engineering innovation focused on energy efficiency, particularly within PES fractional horsepower motors addressing tighter HVAC standards globally could boost organic volume over medium term.

- Constraints from supply chain disruptions, especially around rare earth magnets vital for precision servo motors within AMC create pricing pressure risks alongside potential module shipment delays affecting customer acceptance timelines [S5].

- Tariff implications, especially against imported commodities or intermediate components require ongoing mitigation through sourcing strategy adjustments or potential price pass-throughs.

- Absence of explicit revenue guidance currently suggests market participants should monitor order book development closely as an indicator of sustained momentum or deceleration risk .

Capital Allocation and Returns Profile

Free cash flow generation remains a strength with FY25 producing approximately $893 million after deducting capex from operating cash flows—reflecting enhanced profitability combined with lean spend programs [F1]. However:

- Share repurchases paused completely in FY25 contrasting with prior activity; dividend policy details are not explicitly stated suggesting possibly retained earnings channeled toward deleveraging or reinvestment amidst corporate restructuring [F1][S7].

- Return on equity stands modest at ~4.1% despite net income growth owing mainly to elevated equity base post-divestiture adjustments; this implies scope for improved capital efficiency if operational leverage sustains or share buybacks recommence [F1].

- Liquidity remains healthy supported by cash equivalents exceeding $520 million versus current liabilities around $1.26 billion yielding a current ratio above two—a comfort factor during periods of supply chain unpredictability [F1][S8].

Industry Contextual Factors (Analysis)

Specialty industrial machinery firms like Regal Rexnord operate within complex global supply chains incorporating commodity-sensitive materials such as rare earth elements crucial for high-performance magnets used in servo motors and drives integral to automation/productivity solutions across industries . The recent years have been marked by tightening supply/demand balance for these inputs exacerbated by geopolitical trade frictions leading to elevated tariffs adding cost layers. Moreover, industrial automation growth is being driven by megatrends such as digital transformation initiatives across manufacturing floors, increasing use of robotics and factory automation systems—areas where Regal Rexnord’s AMC segment is well-positioned but will require continuous innovation investment to stay differentiated amid growing competition from large diversified industrial suppliers. The gradual tightening of energy-efficiency standards globally is another structural growth enabler particularly for PES fractional horsepower variable frequency drives targeting HVAC markets transforming toward smart building solutions.

Conclusion

Regal Rexnord's fiscal year ending December 2025 reflects successful navigation through a transitional period marked by strategic divestitures narrowing its portfolio toward higher-growth motion control applications while improving profitability metrics notably operating income (+8%) and net income (+42%). Key growth drivers include accelerated data center automation demand contributing close to three-quarters billion dollars worth of orders last quarter alone. Nonetheless, persistent supply chain challenges tied to rare earth magnet availability alongside tariff-induced cost pressures pose tangible risks that may cap margin expansion or delay shipments intermittently. From a capital perspective, the business produces substantial free cash flow underpinning liquidity strength although modest ROE indicates potential under-leverage relative to equity base which could improve if capital returns scale up beyond current conservative levels. Stakeholders should monitor order intake trends especially within AMC as well as management's actions related to supply chain risk mitigation measures—both will be critical milestones signaling whether current momentum translates into sustainable medium-term growth.

Disclaimer: This document provides an analytical overview based exclusively on publicly available information including SEC filings ([S#]), corporate news releases ([N#]), and validated financial data ([F1]). It contains no investment advice nor recommendation.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments