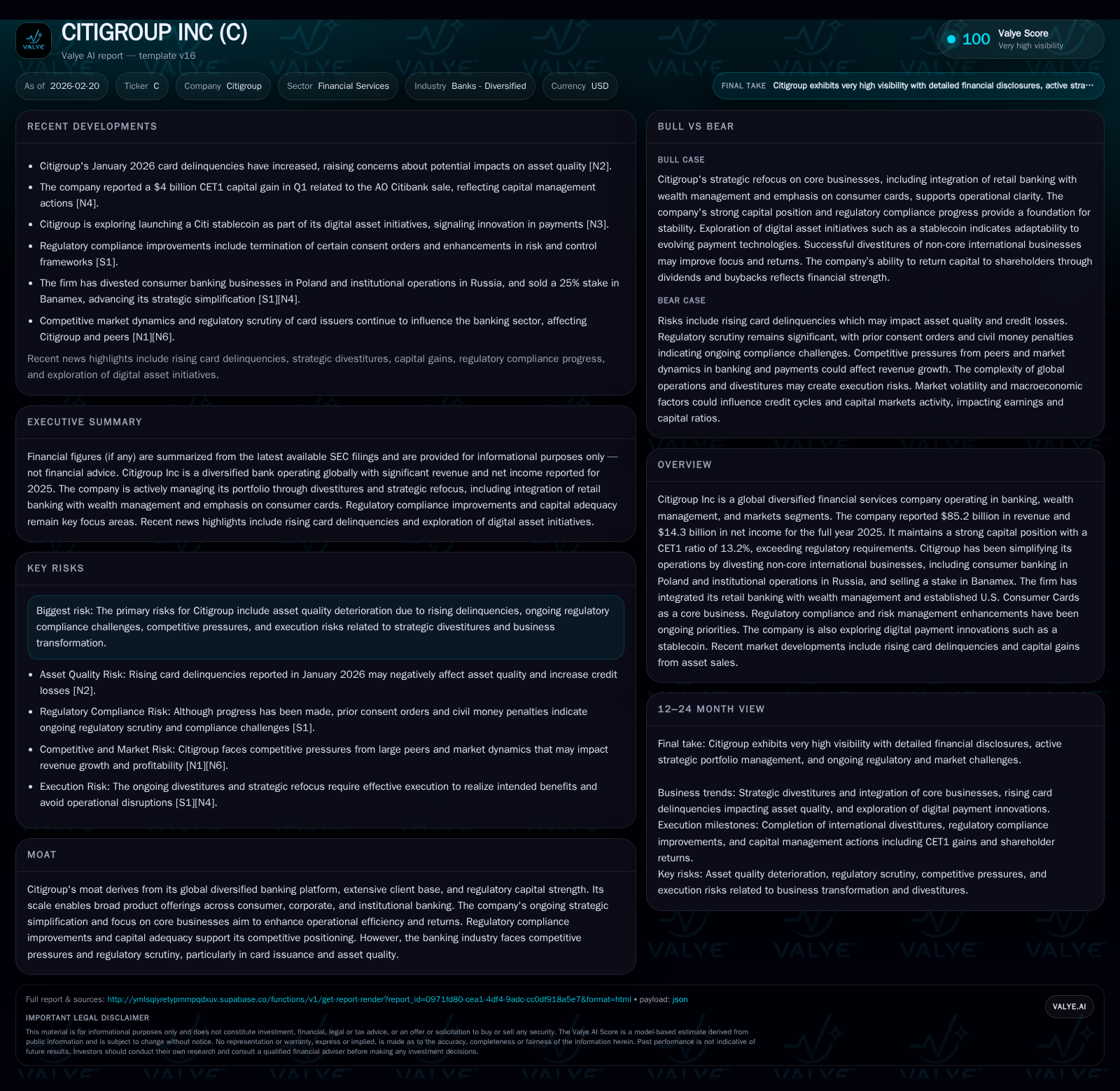

Citigroup’s Strategic Simplification and Capital Discipline Drive 2025 Results

Citigroup’s 2025 performance reflects focused divestitures, capital buffers, and cautious navigation of rising credit risks.

In 2025, Citigroup delivered steady revenue growth alongside a marked improvement in net income, supported by strategic simplification efforts including divesting non-core international assets. The bank maintained robust regulatory capital levels with a CET1 ratio well above thresholds, enhancing its risk resilience amid rising card delinquencies. Innovation efforts, notably exploring a dollar-pegged stablecoin, signal a forward-looking approach to digital payments. Substantial share repurchases and consistent dividends underscore a disciplined capital return strategy, despite negative free cash flow reflecting operational cash outflows and investments.

Historical Financial Performance and Revenue Drivers Through 2025

Over the past three fiscal years, Citigroup has exhibited consistent top-line growth underpinned by its diversified financial platform. Revenues rose steadily from $75.3 billion in FY2022 to $78.5 billion in FY2023 (+4.1%) and further to $81.1 billion in FY2024 (+3.4%), culminating at $85.2 billion in FY2025—a solid approximate compound annual growth rate near 5% over this period [F1]. Net income fluctuated more distinctly: after declining from $14.8 billion in FY2022 to $9.2 billion in FY2023 amidst operational challenges and restructuring costs, it rebounded strongly to $12.7 billion in FY2024 (+37.6%) and accelerated further by nearly 12.8% to $14.3 billion in FY2025 [F1]. This rebound reflects improved profitability linked to strategic focus on higher-return core segments.

Operating income was not provided in available filings; however, the upward net income trajectory aligns with ongoing measures to enhance efficiency and concentrate resources on mainstay businesses [S1]. Divestitures contributed to easing operational complexity but also temporarily impacted some earnings components.

Historical performance (annual)

| FY | Rev ($bn) | Net ($bn) | CFO ($bn) | Capex ($bn) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 85.2 | 14.3 | -67.6 | 6.5 | +5.0% | +12.8% |

| 2024 | 81.1 | 12.7 | -19.7 | 6.5 | +3.4% | +37.4% |

| 2023 | 78.5 | 9.2 | -73.4 | 6.6 | +4.1% | -37.8% |

| 2022 | 75.3 | 14.8 | 25.1 | 5.6 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): OpInc. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($bn) | Buybacks ($bn) | FCF ($bn) |

|---|---|---|---|

| 2025 | 5.4 | 13.3 | -74.2 |

| 2024 | 5.2 | 2.5 | -26.2 |

| 2023 | 5.2 | 2.0 | -80.0 |

| 2022 | 5.0 | 3.3 | 19.4 |

Source: SEC companyfacts cache [F1].

*Note: ROE calculated as Net Income / Equity for FY2025; operating income data not disclosed [F1],[S1]. Operating CFO shows significant volatility, turning deeply negative in recent years.

Operational Simplification: Divestitures and Business Realignment

Citigroup’s drive toward operational simplification has been pivotal for the improved outcomes witnessed in 2025 [N7],[S1]. Noteworthy among these moves were the divestitures of non-core international units—specifically consumer banking operations in Poland, institutional banking businesses in Russia, and the sale of a significant stake in Mexico's Banamex franchise [S1][N7]. These steps aimed at shedding lower-margin or higher-risk exposures while reallocating capital toward core U.S.-centric franchises.

In parallel, Citigroup advanced integration efforts by merging its retail banking capabilities with wealth management initiatives targeting affluent clients domestically; this synergy supports cross-selling opportunities within the U.S Consumer Cards business line that has been elevated as a strategic core offering [S1],[N7]. From a sector perspective, this sharpening of focus aligns with trends where diversified banks prune 'non-core' assets to maximize return on equity and streamline regulatory compliance requirements.

The strategic realignment highlights deliberate concentration on areas with better scalability and fee-generation potential while reducing geopolitical risk exposure inherent in some emerging markets segments.

Regulatory Capital Strength and Risk Management Enhancements

Citigroup maintained a robust Common Equity Tier 1 (CET1) capital ratio of approximately 13.2% as of year-end 2025, surpassing minimum regulatory capital thresholds comfortably [F1],[S1],[N10]. This CET1 buffer provides critical solvency protection amid uncertain macroeconomic conditions and regulatory scrutiny across banking jurisdictions.

Further reinforcing its capital profile was a reported one-time CET1 gain of roughly $4 billion linked to the sale of Asian operations (AO Citibank disposal), boosting tier-one capital reserves early in Q1 of calendar year '26 [N10]. Such actions underscore prudent balance sheet optimization aimed at both reinforcing resilience against credit losses and freeing up capital for prioritized allocation.

Risk management upgrades have run concurrently with these financial enhancements; particularly enhancement of credit risk frameworks addressing emerging asset quality pressures including tightened monitoring of credit card portfolios and provisioning policies reflective of evolving delinquency patterns [S1],[N10]. Underlying stress testing practices now incorporate more conservative assumptions given macro signals.

Emerging Credit Risks: Impact of Rising Card Delinquencies

Recent market intelligence indicates a notable rise in card delinquency rates reported for January months pre-2026—a development that raises caution flags over potential deterioration in asset quality for consumer credit exposures at Citigroup [N9],[S1]. Card delinquencies are borrower payments overdue beyond contractual terms; increased rates may signal consumer financial strain amid inflationary pressures and interest rate elevations.

Consequently, Citigroup has adjusted loan loss provisions accordingly within its provisioning framework while proactively strengthening internal controls around collections methodologies and credit underwriting standards to mitigate prospective charge-offs [S1],[N9]. Although these headwinds could limit margin expansion or pressure profitability short term, the previously discussed CET1 capital cushion offers mitigation levers.

Credit card portfolios remain strategically important due to their volume scalability but require vigilant oversight as part of the bank's asset quality governance amid competitive issuance environments where reward program economics influence borrower behavior.

Innovations in Digital Payments: Exploring Citi Stablecoin

Looking ahead, CEO Jane Fraser publicly disclosed Citigroup’s initiative exploring the issuance of a proprietary dollar-pegged stablecoin—branded as Citi stablecoin—intended to tap into the evolving payments landscape dominated progressively by digital currencies [N1],[S1].

This innovation pursuit aims to modernize retail transaction processing leveraging blockchain technology to enable faster settlement times while maintaining stability associated with fiat currency peg structures.[N1] Broad adoption would afford Citi differentiation versus traditional payment rails dominated by Visa/Mastercard networks offering incremental fee revenue pathways.

Strategically, this move positions Citigroup among early-adopters within established banks seeking regulated cryptographic currencies' benefits without volatility typical of unbacked tokens—potentially reshaping client engagement models particularly within wealth management and consumer cards sectors where speed/personalization drive usage patterns.

Capital Allocation: Dividends, Buybacks, and Return on Equity

Citigroup sustained shareholder distributions consistent with recent years by paying approximately $5.4 billion in dividends during fiscal year ending December ‘25 [F1],[S9],[S17]. More striking was the significant escalation of share repurchase activity; buybacks surged to an estimated $13.25 billion versus only about $2.5 billion executed in FY24 [F1],[S17],[S25]. Such aggressive repurchase cadence signals confidence by management aiming to lift per-share earnings metrics amidst measured reinvestment levels.

Approximated return on equity based on reported net income against average shareholders’ equity stood near a modest yet recovering ~6.7% range for FY25—a metric influenced partly by elevated equity bases reflective of regulatory capital mandates rather than solely operational performance leverage [F1].

Operating cash flow dynamics present complexity: CFO swung deeply negative at about -$67 billion reflecting working capital needs or mark-to-market influences typical for diversified banks balancing extensive trading portfolios alongside loan commitments; combined with steady capex around $6.5 billion annually results in sharply negative free cash flow approximating -$74 billion last fiscal year [F1]. This gap evidences tradeoffs between aggressive shareholder returns via buybacks against internal cash generation shortfalls possibly compounded by portfolio restructuring timing.

Investors should note that such negative free cash flow is not unusual for large global banks engaged simultaneously in legacy transformation programs plus technology investments underpinning future growth strategies.

Outlook and Strategic Milestones to Watch in 2026

Looking ahead into calendar year '26, key milestones include:

- Progress on Citi stablecoin development and potential launch timelines remain critical innovation markers impacting payments strategy [N1],[S1].

- Monitoring evolving credit quality trends amid rising card delinquencies will be vital for assessing asset risk exposure and provisioning adequacy [N9],[S1].

- Final effects from ongoing divestitures such as Polish consumer banking exit and Russian institutional wind-down will clarify residual revenue impacts versus cost savings [N7],[S1].

- Continued adherence to tightening regulatory compliance standards including liquidity coverage ratios will shape operational flexibility across jurisdictions [S1].[N10]

- Capital allocation discipline balancing aggressive share repurchases against liquidity needs under uncertain macroeconomic conditions will be an ongoing board-level focus [S17].[N10]

In sum, Citigroup's trajectory exhibits cautious optimism anchored by strategic simplification initiatives paired with innovation pursuits while managing emerging credit risks within a robust capital framework.

This report compiles analysis exclusively from publicly available SEC filings and credible news sources without reliance on speculative forecasts or investment advice directives.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments