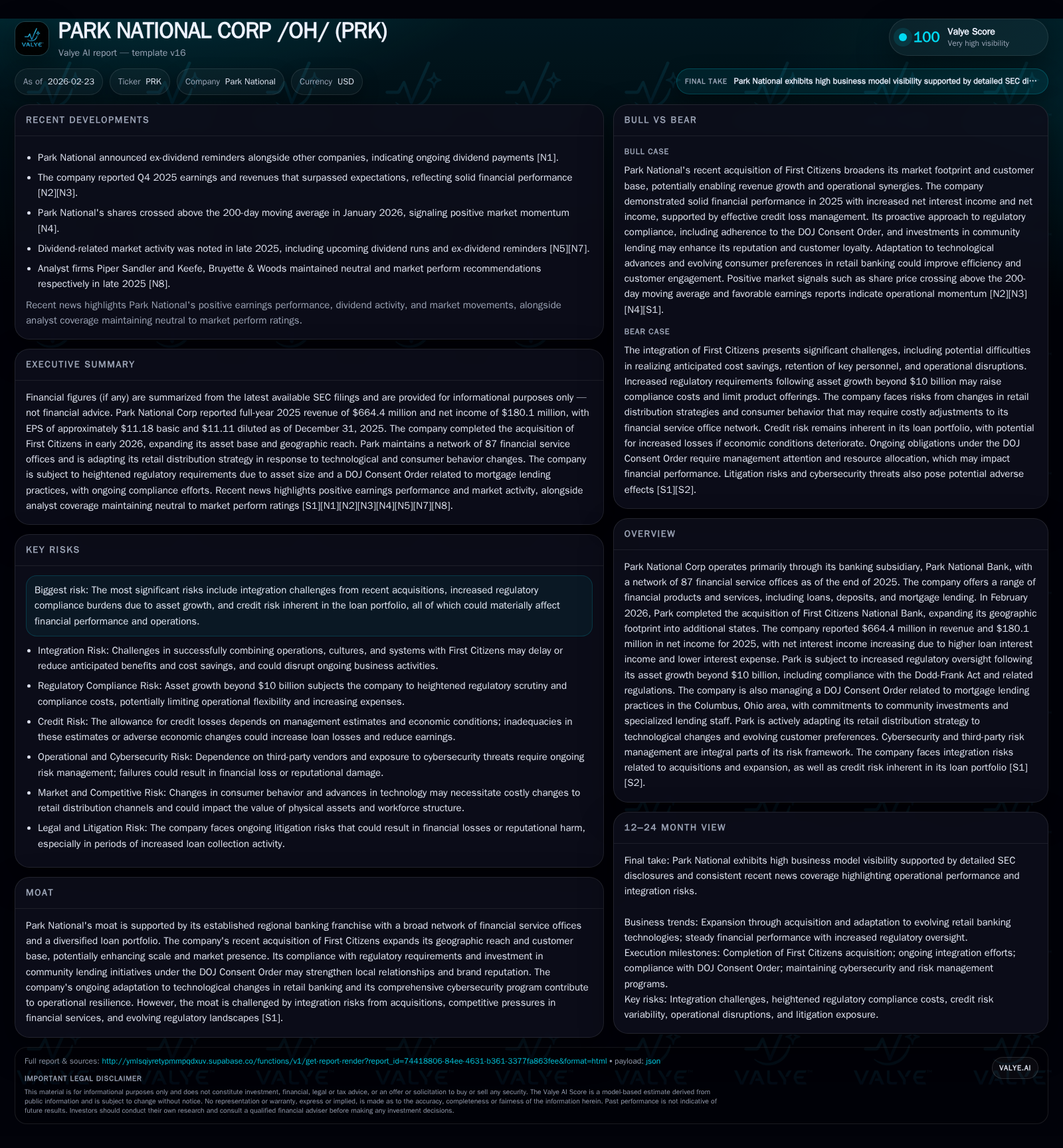

Park National Corp Strengthens Regional Reach Through Strategic Acquisition and Operational Resilience

The 2026 acquisition of First Citizens National Bank marked a pivotal expansion for Park National Corp, fueling notable revenue growth while intensifying regulatory and integration demands.

Park National Corp posted solid financial results in 2025, highlighted by increased revenues and an 18.9% net income growth driven by higher net interest income and disciplined expense management. The February 2026 acquisition of First Citizens National Bank expanded its geographic footprint beyond Ohio into several Southeastern states, enhancing its branch network to 87 offices but also bringing integration complexity. Park’s surpassing $10 billion in assets now subjects the company to intensified regulatory oversight, including compliance with Dodd-Frank frameworks and a DOJ Consent Order tied to mortgage lending. Looking ahead, the firm balances organic growth opportunities with acquisition risks under evolving competitive and regulatory landscapes. Capital deployment includes opportunistic share repurchases alongside steady free cash flow generation, reflecting prudent capital management amid scale expansion.

2025 Financial Performance: Revenue and Profit Growth Drivers

In fiscal year 2025, Park National Corp posted revenues of $664.4 million, marking a 2.9% increase from the prior year’s $645.6 million [F1]. This topline improvement was primarily driven by an uptick in net interest income attributable to a favorable shift in loan portfolio yields amid higher loan interest rates coupled with more efficient management of funding costs through reduced interest expense [N2][S1]. The company leveraged asset-liability management strategies amid fluctuating interest rate environments to bolster net interest margins without materially elevating risk exposure.

Net income surged by 18.9% year over year to $180.1 million in 2025 from $151.4 million in 2024 [F1]. The disproportionate increase relative to revenue reflects operational leverage realized through restrained overhead growth amidst moderate inflation-related pressures on noninterest expenses [S1]. Cost discipline combined with solid credit quality maintenance allowed Park to expand its profitability metrics despite a broader macroeconomic backdrop characterized by elevated inflation and tightening monetary policy.

Operating cash flow (CFO) similarly exhibited robust progress climbing nearly 11% YoY to $198.3 million [F1], underscoring effective conversion of accrual earnings into liquidity. Meanwhile, capital expenditures declined notably by over 30%, settling at $6.4 million for the year as investments in physical infrastructure were scaled back in favor of technology-driven channel enhancements reflective of evolving customer behaviors [F1][S23][S15].

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | Capex ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 664 | 180 | 198 | 6 | +2.9% | +18.9% |

| 2024 | 646 | 151 | 179 | 9 | +19.5% | |

| 2023 | 127 | 151 | 8 | -14.6% | ||

| 2022 | 148 | 135 | 8 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): OpInc, Div. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 20 | 192 | 13.3 |

| 2024 | 0 | 170 | 12.2 |

| 2023 | 23 | 143 | 11.1 |

| 2022 | 0 | 127 | 13.9 |

Source: SEC companyfacts cache [F1].

Note: Operating income data unavailable in provided tags.

Impact of First Citizens Acquisition on Geographic Footprint and Market Presence

February 1st, 2026 marked the completion of Park National’s acquisition of First Citizens National Bank [S1][N3], strategically extending its geographical footprint beyond its traditional Ohio base into four additional states: Kentucky, North Carolina, South Carolina, and Tennessee [S23]. This acquisition enlarges Park’s distribution network to encompass a total of approximately 87 financial service offices as of end-2025 plus the newly acquired branches.

While this geographic extension offers material upside potential through deeper market penetration and enhanced cross-selling opportunities—leveraging First Citizens’ established customer relationships—the transaction also presents classic regional banking merger integration complexities such as systems harmonization across different core banking platforms, aligning disparate operational policies, and mitigating attrition risk among key clients and personnel during transition phases [S2][S23]. Harmonizing technology stacks while maintaining seamless customer experience will be paramount given the competitive nature of retail deposit-taking and lending sectors where customer convenience correlates directly with retention.

Regulatory Environment and Compliance Commitments Shaping Operations

With total consolidated assets surpassing the critical $10 billion mark post-acquisition expected by December-end 2026 [S12][S15], Park National is subject to enhanced oversight governed mainly by the Dodd-Frank Act suite administered through agencies including the CFPB, OCC, Federal Reserve Board, and FDIC.

These regulations impose intensified requirements such as modified deposit insurance assessment methodologies that could inflate costs depending on performance scorecards, limits on debit card interchange fees impacting fee revenues, adherence to enhanced Volcker Rule restrictions limiting proprietary trading activities, and relinquishment of certain simplified capital rules like the Community Bank Leverage Ratio (CBLR) election previously available because of asset size thresholds [S15]. Compliance necessitates additional investment in personnel skilled at regulatory engagement plus expanded internal control mechanisms exerting pressure on operating efficiencies.

Moreover, Park remains committed to fulfilling its obligations under a U.S. Department of Justice Consent Order stemming from scrutiny over mortgage lending practices within the Columbus metropolitan area [S10][S21]. This five-year settlement mandates at least $7.75 million community investments directed toward increasing credit access in majority-black and Hispanic census tracts along with enhanced community development partnerships funded at minimum levels ($500K), consumer education budgets ($750K), plus support for dedicated physical infrastructure including one full-service branch and specialized mortgage lending personnel focused on responsible community outreach [S11]. While necessary for brand reputation rehabilitation and compliance restoration, these initiatives require ongoing allocation of management attention and financial resources that could impact near-term profitability.

Future Growth Prospects: Opportunities and Constraints in Expansion Strategy

Park’s pathway forward offers dual levers for growth: organic expansion via deepened penetration within existing markets supplemented by cross-selling into newly acquired territories post-First Citizens deal; alongside strategic M&A initiatives targeting additional institutions or assets consistent with management’s historical consolidation playbook [S1][N1].

Growth drivers include pipeline ramp-up from loan originations fueled by regional economic stability; however competitiveness from both similarly scaled regional banks as well as non-bank fintech entrants challenges pricing power on deposits under rising interest rate regimes [S18]. Enhanced digital offerings constitute a key differentiation vector—where seamless omnichannel delivery can drive wallet share gains but requires continuous tech investments aligned with shifting consumer behaviors documented industry-wide.

Constraints center around credit risk vigilance amidst evolving macroeconomic uncertainties such as inflationary impacts squeezing borrower repayment capacities plus sector geographic concentration risks crystallizing especially with expansion into new states bearing distinct demographic-economic profiles [S7]. Integration economies will be critical yet potentially elusive if cultural or systems consolidation delays emerge.

Financial Forecasts and Key Metrics to Monitor Post-Merger

Explicit forward-looking guidance is not disclosed; therefore stakeholders should track convergence indicators such as synergy capture timing against stated targets including cost savings from back-office consolidation as well as incremental revenue uplift from expanded product cross-selling capabilities post-acquisition integration [N1][N2][S3].

Of particular note will be movements in net interest margin metrics which reflect both yield curve evolutions and competitive pricing pressures on deposits versus loans—impacted further by fluctuations in cost of funds associated with deposit mix shifts or wholesale funding reliance [N2]. The allowance for credit losses calls for rigorous monitoring given CECL model sensitivities amid unpredictable economic clocks—provisions may vary with portfolio performance signaling underlying loan quality that could affect earnings volatility [S13][N13]. Expense ratio trends will reveal management discipline amid regulatory burden expansions.

Capital Allocation: Share Repurchases, Dividends, and Return on Equity Analysis

Return on equity approximated a commendable ~13.3% based on FY2025 reported net income against equity base ($180 million / $1.353 billion) evidencing efficient capital use typical among mid-tier regional banks balancing growth with stability [F1].

Free cash flow generation proved robust near $192 million (CFO less capex), enabling flexible capital deployment without excessive leverage build-up [F1]. Notably the resurgence of share repurchases manifested via $20 million repurchased in FY2025 after no buybacks recorded in FY2024 signals confidence in intrinsic valuation alongside sound liquidity standing [F1][N3]. Dividend disclosures are absent within filings suggesting either consistency at modest levels or withholding commentary; thus this remains an area for investor watchfulness.

This allocation mix underscores a strategy prioritizing shareholder returns balanced prudently against reinvestment needs especially considering pending integration costs plus looming incremental regulatory compliance expenditure loads.

Risks from Integration and Credit Portfolios: Managerial Responses

Integration risk is vital given the expanded scope presented by First Citizens’ assimilation where unexpected delays or synergistic shortfalls could curtail anticipated benefits or elevate expenses beyond forecasts—issues include cultural alignment complexities, technology platform mergers potentially disrupting client servicing workflows, plus risks related to key employee departures impacting organizational continuity [S1][S2][S23].

On credit fronts inflationary pressures coupled with rate volatility add layers of underwriting challenge prone to asset-liability mismatch risks where shifts in loan prepayment speeds or deposit re-pricing timing misalignments can compress net interest margins unexpectedly [S8][S22]. Prudential allowance for credit losses estimation under CECL remains subject to model risk particularly if economic forecasts prove inaccurate—a factor requiring layered scenario analyses overseen by risk committees [S13][S22].

Management emphasizes rigorous credit administration protocols including diversified exposure monitoring combined with conservative provisioning fortified by periodic CECL assumption recalibrations aiming at mitigating downside surprises [S4][S7][S13]. Cybersecurity vigilance complements this framework protecting operational integrity against emergent threats ensuring resilience across physical-digital banking channels [S11][S21].

Disclaimer: This analysis report is prepared solely for informational purposes based on publicly available documents including SEC filings and news sources as cited. It does not constitute investment advice or recommendations regarding any securities discussed herein.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments