Portillo's Growth Strategy Adjusts After Expansion Challenges and Inflation Pressures

Portillo's Inc. recalibrates its expansion pace following Texas market setbacks while managing margin pressures due to inflation and labor costs.

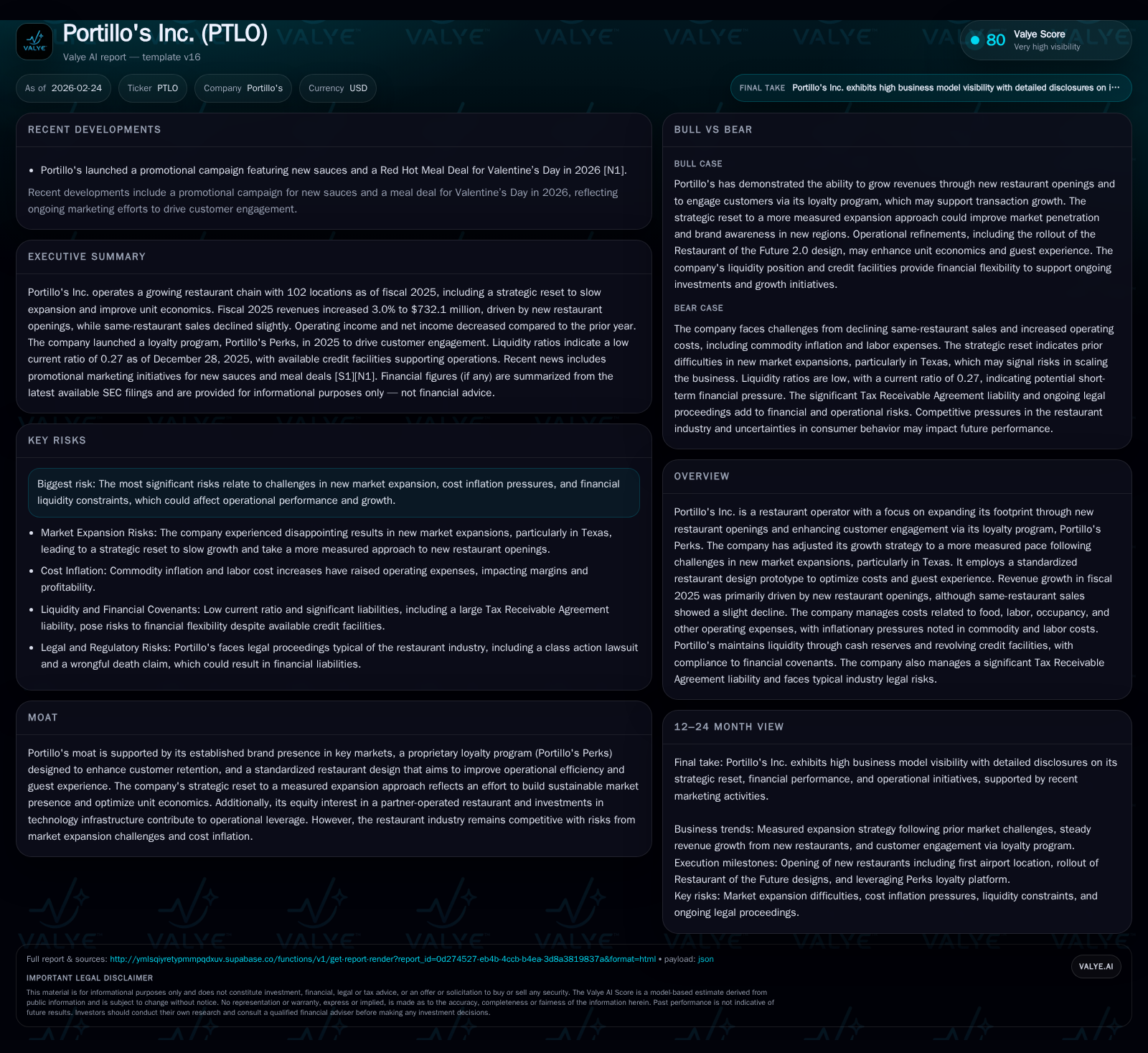

Portillo's Inc., a restaurant operator known for its distinctive brand and loyalty program, reported modest revenue growth in fiscal 2025 driven by new store openings but faced a slight decline in same-restaurant sales. The company has reset its expansion strategy to be more measured after disappointing returns in high-profile Texan markets, opting for greater spacing between new locations. Inflationary headwinds in commodities and labor have pressured margins, reflected in a drop of operating income and net income year-over-year. Capital allocation remains focused on growth through new restaurant development, with significant investments maintaining a negative free cash flow profile despite strong operational cash generation.

Company Overview

Portillo's Inc., a restaurant operator with a distinctive Midwestern brand presence, focuses on expanding its footprint through opening new venues and enhancing consumer loyalty via its proprietary Portillo's Perks program [S1]. In fiscal year 2025, the company opened eight restaurants across five states, including entry into Georgia with an inaugural Kennesaw location [S1]. Most new stores launched adhered to the company's "Restaurant of the Future (RoTF) 1.0" prototype, designed as a roughly 6,250 square foot efficient format emphasizing cost control and guest experience optimization [S1]. A further upgrade to this prototype (RoTF 2.0) is slated for launch in 2027.

Historical Performance and Growth Drivers

Revenue grew modestly by approximately 3% in fiscal year 2025 compared with fiscal 2024, increasing from roughly $710.6 million to $732.1 million [S20][F1]. This growth was attributed mainly to new restaurant openings rather than organic demand improvements since same-restaurant sales declined slightly by 0.5%, reflecting a traffic decline more than offset by average check increases [S1][S20]. The traffic dip of about 2.5% pressured overall comparable sales despite menu price realizations.

Operating income experienced a notable contraction of nearly one-quarter (24.7%) down to approximately $43.7 million, primarily driven by margin compression from inflationary impacts on commodities and labor costs as well as deleverage effects from recent restaurant openings [F1][S20]. Net income similarly saw a more acute decline of some 34.5%, settling at $19.3 million [F1]. These results underscore challenges faced in sustaining unit-level economics during expansion phases.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 19 | 72 | 44 | 90 | -34.5% |

| 2024 | 30 | 98 | 58 | 88 | +60.2% |

| 2023 | 18 | 71 | 55 | 88 | +69.8% |

| 2022 | 11 | 57 | 41 | 47 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Rev, Div. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | -19 | 4.1 | |

| 2024 | 10 | 7.4 | |

| 2023 | 57 | -17 | 5.7 |

| 2022 | 57 | 10 | 4.2 |

Source: SEC companyfacts cache [F1].

Note: Revenue data for FY22-23 are not available from provided tags.

Operating cash flow decreased by approximately 26.7% year-over-year to $71.9 million due primarily to reduced profitability and working capital changes [F1]. Capital expenditures remained elevated at approximately $90 million as investments continued into new restaurant openings and technology enhancements [F1][S9][S24]. The resulting free cash flow was negative at about $18.5 million for FY25, reflecting the capital intensity of growth initiatives.

Strategic Reset and Forward-Looking Expectations

In September 2025, Portillo’s announced a strategic reset following disappointing results from aggressive expansion efforts particularly within Texas markets such as Dallas-Fort Worth and Houston [S1]. The revised approach favors gradual market entry with greater spacing between new locations both temporally and geographically to build brand awareness organically before further rollout [S1]. This strategy is exemplified by opening only one restaurant in Georgia during late fiscal year 2025 and delaying additional openings there until at least fiscal year 2027.

The company also plans refinement of its Restaurant of the Future prototype with RoTF 2.0 expected in fiscal year 2027 aimed at improving unit economics while enhancing guest experience based on learnings from earlier versions [S1].

Management priorities for fiscal year 2026 include driving transaction growth leveraging the Portillo’s Perks loyalty platform, focusing on operational excellence, and investing in team members—all supporting commitments toward positive free cash flow generation over time [S1].

Operating Cost Dynamics

Commodity inflation moderated slightly to about 3.9% in fiscal year 2025 from approximately 4.2% the prior year, yet food, beverage and packaging costs increased by roughly $10 million or over four percent reflecting both inflationary pressures and volume growth related to new units [S1][S21]. Labor expenses rose nearly six percent driven by wage inflation, increased benefit costs, lower transaction volumes, and deleverage effects from newer restaurants not yet achieving mature productivity levels [S1][S20][S21]. Occupancy expenses also increased commensurately with expanded real estate footprint [S20].

The company employs diverse supplier pricing strategies including fixed-price contracts alongside commodity-indexed programs aimed at mitigating volatility though exposure remains given scale relative to larger multi-concept peers.

Capital Structure and Liquidity Profile

As of December end-2025, total debt stood at approximately $334 million consisting of a term loan balance near $247 million and revolving credit borrowings around $90 million [F1][S12][S13][S14]. The company refinanced its credit facilities effective January 27, 2025 extending maturities through January 2030 while reducing interest rates from mid-7% range down closer to about 6.7% currently [S4][S22][F1]. Letters of credit totaled approximately $4.4 million within revolver usage leaving roughly $55+ million available capacity.

Cash balances approximated $20 million while current liabilities significantly exceeded current assets yielding a current ratio near a low of ~0.27; however management reported compliance with all financial covenants throughout reporting periods without defaults or breaches noted [F1][S7][S12].

There were no dividends paid during the latest periods per available data; historical share repurchases occurred pre-IPO or early post-IPO phases but have not recurred meaningfully recently consistent with capital reinvestment focus [F1][S23].

Returns & Capital Allocation Summary

Estimated return on equity for fiscal year ended December 28, 2025 approximates just over four percent reflecting subdued profitability amidst margin pressures despite steady revenue growth trends [F1]. Capital allocation remains heavily weighted toward reinvestment into property plant & equipment with capital expenditures consistently outpacing operating cash flows resulting in negative free cash flow positions over recent years.

Risk Considerations

Key risks include execution uncertainties associated with the newly adopted measured expansion cadence which may delay fully capturing latent demand outside established core markets amid intensifying competition within casual dining sectors regionally [N2][S10]. Inflationary pressures impacting wages due to regional minimum wage legislation increases coupled with commodity price volatility pose ongoing margin risks potentially necessitating menu price adjustments that could influence customer retention dynamics [S10]. Financial leverage requires vigilant liquidity management ensuring covenant compliance amid unanticipated macroeconomic shifts potentially affecting operational results or borrowing access.

Summary

Portillo's Inc.’s fiscal year ended December 28, 2025 demonstrated modest top-line growth principally driven by incremental unit count increases but hindered at the same-store level due to traffic softness compounded by inflationary cost pressures impacting food and labor expenses which compressed earnings relative to prior years. The strategic shift toward cautious geographic rollout pacing aims for sustainable brand penetration balancing measured growth against rapid saturation attempts evidenced previously especially during Texas market expansions. Capital investments remain robust underpinning growth ambitions including critical technology upgrades though free cash flow remains negative reflecting inherent capital intensity within restaurant industry economics. Balance sheet strength benefits from successful refinancing improving credit terms albeit substantial leverage persists requiring close monitoring amidst evolving market conditions. Long-term value creation will depend heavily on successful execution of loyalty engagement initiatives coupled with operational efficiencies balancing cost inflation impacts against competitive positioning across targeted markets.

This analysis is intended solely for informational purposes without providing investment advice or recommendations regarding securities mentioned herein.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments