Fulcrum Therapeutics’ Growth Ambitions Constrained by Clinical Setbacks and Capital Intensity

Clinical stage biotech Fulcrum Therapeutics advances rare disease drug pociredir while managing significant losses and operational risks.

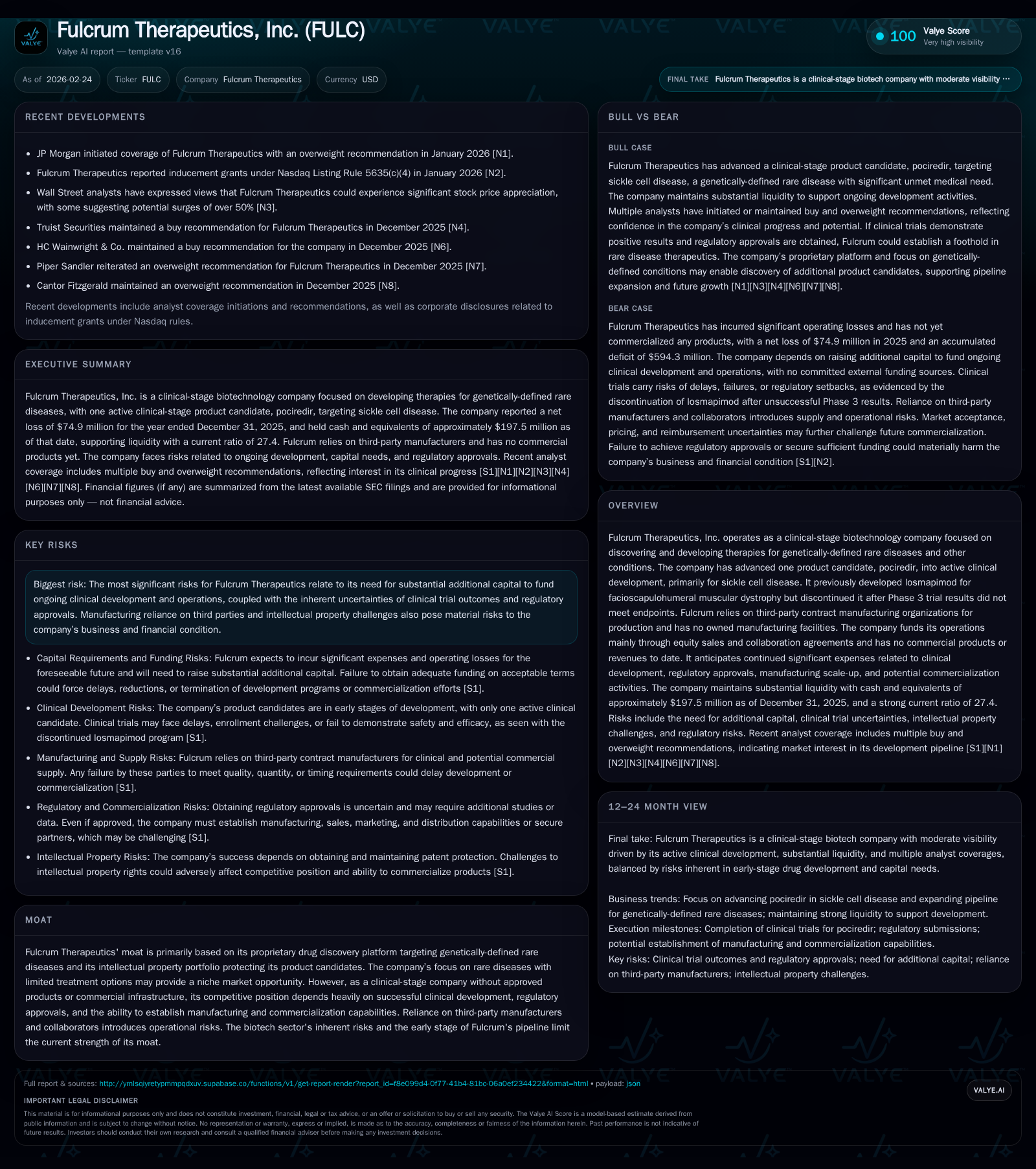

Fulcrum Therapeutics operates as a clinical-stage biotechnology company focusing on genetically-defined rare diseases, with its lead candidate pociredir targeting sickle cell disease. Historically, the company has experienced significant operating losses driven by clinical development expenses and lacks any commercial products or revenue. Future growth hinges on successful clinical trial outcomes and regulatory approvals amid ongoing capital needs and operational risks linked to outsourcing manufacturing. The absence of revenue generation and reliance on equity financing underscore challenges in path to profitability.

Company Overview and Historical Performance

Fulcrum Therapeutics is a clinical-stage biotechnology company dedicated to discovering and developing therapies for genetically-defined rare diseases. Its portfolio is heavily concentrated on product candidates derived from its proprietary discovery platform tailored to niche conditions with limited treatment options. As of early 2026, the company’s flagship asset is pociredir, which is currently undergoing active clinical trials targeting sickle cell disease — a serious genetic blood disorder.

Historically, the company faced a setback with its prior development candidate losmapimod for facioscapulohumeral muscular dystrophy (FSHD). The Phase 3 trial failed to meet primary endpoints, resulting in discontinuation of the program. This event underscores biotech development risk inherent in the rare disease segment where patient populations are small and clinical endpoints challenging to achieve.

Financially, Fulcrum operates without any commercial products or revenues to date. The company’s historical operating results demonstrate sustained negative earnings augmented by sizable investments into R&D activities (including clinical trials) and supporting infrastructure expansion required to advance pipeline candidates. Over the last four fiscal years the operating income trends were as follows (all figures in USD):

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -75 | -60 | -85 | 314000 | -670.0% |

| 2024 | -10 | -2 | -22 | 278000 | +90.0% |

| 2023 | -97 | -91 | -111 | 508000 | +11.4% |

| 2022 | -110 | -97 | -113 | 1963000 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Rev, Div, Buybacks. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -60 | -21.5 |

| 2024 | -2 | -4.0 |

| 2023 | -91 | -41.4 |

| 2022 | -99 | -55.2 |

Source: SEC companyfacts cache [F1].

(Amounts rounded; source: [F1])

Operating losses intensified sharply in FY 2025 after a temporary improvement in FY 2024, reflecting stepped-up spending likely due to clinical program acceleration for pociredir and related pipeline activities [S1]. Net income followed a similar trajectory with widening losses (-$74.9 million in FY25 vs -$9.7 million FY24). Operating cash flow remained negative throughout these years consistent with the company's pre-revenue status and development-stage model.

Capital expenditures have been minimal relative to total expenses — below $2 million annually — corroborating Fulcrum’s strategy of outsourcing manufacturing rather than investing in owned production facilities [S1][F1]. Moreover, the balance sheet shows robust liquidity with $197.5 million cash equivalents alongside current assets totaling $357 million against only $13 million current liabilities at the end of FY2025 yielding a current ratio of approximately 27:1 (a notably high figure indicative of strong short-term financial cushion) [F1]. This cash buffer supports ongoing clinical trials but is not expected to obviate future fundraising requirements given projected expenses.

Pipeline Development and Future Growth Prospects

The centerpiece of Fulcrum's pipeline is pociredir, undergoing evaluation primarily as a treatment for sickle cell disease — a rare genetic condition with high unmet medical need due to chronic pain crises, anemia, organ damage, and reduced life expectancy.

Success in this indication would validate the company's drug discovery platform focused on rare genetic disorders and could unlock considerable value through exclusivity provisions typical in orphan drug designations [N1][S1]. Furthermore, Fulcrum continues early-stage research into identifying next-generation targets and molecules for additional genetically-defined rare diseases as part of its long-term growth strategy.

However, the company’s recent experience with losmapimod reveals key limitations; failure to meet Phase 3 endpoints triggered program cessation highlighting risks that may cap growth if pociredir or future candidates do not clear critical regulatory hurdles [S1]. Compounding this risk are industry-wide challenges including stringent evidence requirements by regulatory agencies (FDA/EMA), complex trial designs needed for rare diseases often involving small patient cohorts, and reimbursement uncertainties under evolving healthcare policies [S4][S17][S24].

Financial Guidance and Milestones

Fulcrum has not publicly disclosed formal financial or operational guidance beyond reporting quarterly results [N2][S3]. Investors should closely monitor upcoming clinical readouts from ongoing trials of pociredir as pivotal milestones affecting the company's valuation trajectory.

Analysts highlight that significant upside potential exists contingent upon positive trial data validating efficacy/safety profiles; conversely, negative or inconclusive findings could severely impair capital raising ability given precedence from past trial failures [N1]. Milestones such as submission of New Drug Applications (NDAs), orphan drug designations expansion, strategic partnerships or licensing deals will also be critical value inflection points amidst steady cash burn from development activities.

Given no revenue streams or near-term commercialization plans announced explicitly yet, centralized tracking of expenses related to scale-up manufacturing processes via third parties and advancements in regulatory filings remains essential as leading indicators [S1].

Capital Allocation and Returns

As expected for a clinical-stage biotech without marketed products, Fulcrum generates no profits nor dividends; instead it reports recurring net losses funded primarily through equity issuances and collaboration agreements [S1][F1]. The lack of any dividend payments or share repurchases aligns with an aggressive reinvestment model focused entirely on R&D expenditure.

Return metrics such as ROE are negative (-21.5% approx based on FY25 net loss & shareholders’ equity) reflecting developmental-stage investment rather than operational profitability [F1]. Free cash flow (operating cash flow minus capex) remains deeply negative at approximately -$60 million for FY25 underscoring continuous need for capital infusion ([F1]). Liquidity remains healthy but positioning depends heavily on able execution of pipeline milestones to justify recurrent financing rounds.

Investors should consider that failure to deliver positive data could impair access to further funding sources potentially requiring dilution or partnership agreements dilutive to existing shareholders [S29]. Conversely successful commercialization down the line could transition capital structure priorities towards scaling production capacities or marketing infrastructure investments depending on out-licensing status.

Risk Considerations

Fulcrum Therapeutics faces numerous risks predominantly aligned around:

- Extensive capital requirements paired with absence of revenues creating dependency on equity markets for funding continuing operations.

- Manufacturing risks stemming from reliance exclusively on third-party contract manufacturing organizations (CMOs) potentially sensitive to capacity constraints or compliance issues [S1][S27].

- Regulatory uncertainties including potential delays in approvals or demands for costly post-marketing studies common in FDA/EMA oversight regimes plus impacts from changing healthcare laws restricting pricing/reimbursement such as Inflation Reduction Act implications [S4][S17][S23].

- Intellectual property risks from challenges either defending patent portfolios or avoiding infringement claims which can impose litigation costs and strategic setbacks affecting market exclusivity windows [S12][S16][S22].

- Compliance exposures related to healthcare fraud/abuse statutes globally plus evolving data privacy controls under GDPR and similar statutes adding administrative burdens and potential penalties [S4][S15].

- Operational risks associated with employee or vendor misconduct including data breaches or inaccurate reporting damaging reputation or inviting sanctions especially given sensitive nature of genomic research fields [S11][S19].

- Market pressures leading to downward pricing trends affecting commercial viability once products launch especially considering increasing governmental attempts at cost control worldwide [S24]

- A noted liability risk typical in clinical testing phases encompassing patient injury claims which could lead to litigation costs exceeding current coverage limits further straining finances [S27].

These factors collectively temper expectations about timeline certainty and profitability horizons typical of early-phase biotech enterprises but underline the importance of milestone achievements for de-risking investor outlook.

Industry Context Analysis

The biotechnology sector confronting genetically defined rare diseases carries unique characteristics including:

- Limited patient populations necessitating tailored trial designs often leveraging surrogate endpoints due to scarcity of natural history data.

- High development costs per patient treated driving substantial upfront investment before commercial returns surface.

- Strong reliance on orphan drug incentives granting extended exclusivity periods yet attracting increasing competitor activity pressured by growing biosimilar markets.

- Contract manufacturing dependency prevalent given specialized biologic production requirements involving cell culture technologies necessitating rigorous cGMP compliance.

- Pricing dynamics shaped by evolving payer frameworks incorporating value-based assessments increasingly influenced by pharmacoeconomic evaluations thus impacting net realized revenues even post approval. Fulcrum exemplifies many traits common among peers navigating these dynamics but faces magnified execution challenges reflecting mid-clinic phase status without near commercial fallback options.

Conclusion

Fulcrum Therapeutics stands at a pivotal juncture balancing promising pipeline ambitions against inherent developmental uncertainties characteristic of biotech firms targeting genetically defined rare diseases. Its concentrated dependence on pociredir’s successful advancement predicates future growth prospects while its financial discipline reveals prudent liquidity management albeit underpinned by persistent quarterly net losses necessitating ongoing capital raises. The discontinuation of losmapimod following Phase 3 setbacks highlights execution risk whereas outsourcing manufacturing limits capital intensity but introduces operational dependencies warranting careful supply chain oversight. In sum, Fulcrum will remain reliant on achieving scientific breakthroughs validated through forthcoming clinical milestones alongside securing sufficient funding through public markets or partnerships—key variables determining if it transitions successfully into a commercial-stage enterprise capable of generating sustainable shareholder returns.

This analysis is based solely on publicly available information as cited within sources below and does not constitute investment advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments