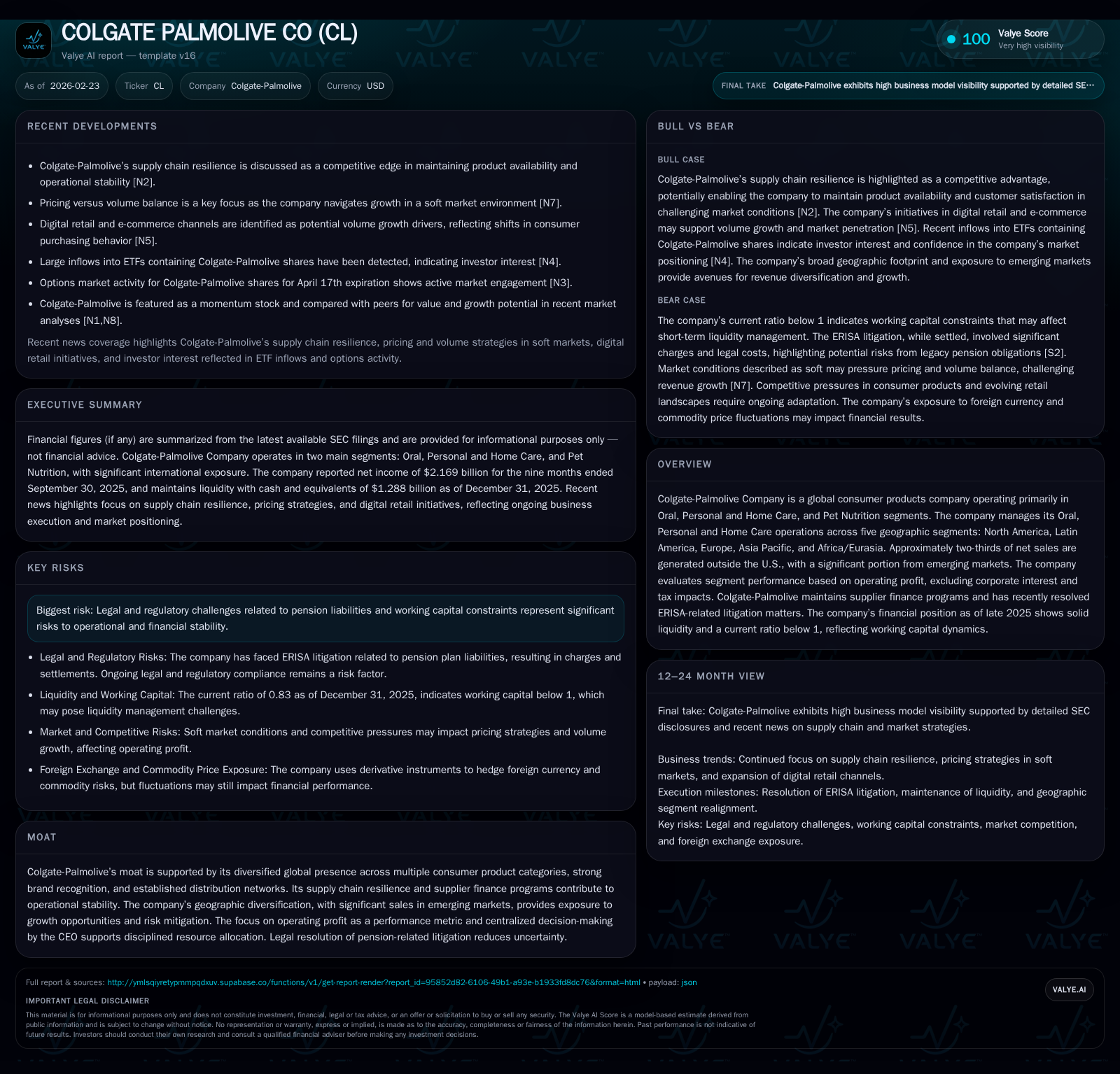

Colgate-Palmolive's Earnings Decline Amidst Supply and Pension Challenges

Analysis of how pension litigation and supply chain factors have influenced Colgate-Palmolive’s recent financial trends and growth outlook.

Colgate-Palmolive, a global leader in consumer products spanning Oral, Personal and Home Care, and Pet Nutrition, experienced a notable decline in operating and net income in FY2025 despite modest revenue growth. This earnings pressure aligns with charges related to protracted ERISA pension litigation and margin impact from supply chain dynamics. The company’s geographic diversification, especially in emerging markets contributing nearly two-thirds of sales, remains a key growth pillar. Meanwhile, disciplined capital allocation continues with robust operating cash flow supporting sizeable share repurchases. Close monitoring of legal settlement outcomes and emerging-market demand will be critical for assessing future performance trajectory.

Historical Financial Performance: Growth Trends and Operating Shifts

Colgate-Palmolive showcased moderate top-line expansion through FY2025 with revenues edging up by 1.7% year-over-year to around $40.3 billion [F1]. However, beneath the surface of revenue growth lay substantial margin pressure that led to operating income descending by 22.5% to $3.31 billion over the same period [F1]. Net income followed suit with a pronounced decline of 26.2%, falling to $2.13 billion [F1]. This divergence suggests that earnings were materially impacted by non-operating factors.

The primary driver behind this profitability squeeze was the accrual of expenses stemming from persistent ERISA-related pension litigation that escalated the company's pension plan liabilities significantly starting in early 2023 [S4][S7][S8]. The quarterly filings outline multiple discrete charges totaling over $330 million recognized against earnings as the courts upheld class action claims regarding residual annuities tied to a 2005 retirement plan amendment [S7]. Concurrently, input cost inflation and ongoing supply chain disruptions added incremental strain on operating margins requiring judicious cost management.

Meanwhile, cash flow generation remained resilient; operating cash flow rose slightly by 2.2% to approximately $4.2 billion [F1], underscoring underlying business cash strength despite profit volatility. Capital expenditure also increased sharply by nearly 23% year-over-year reflecting investments in productivity improvements and innovation projects designed to sustain competitive positioning [F1].

Historical performance (annual)

| FY | Net ($bn) | CFO ($bn) | OpInc ($bn) | Net YoY |

|---|---|---|---|---|

| 2025 | 2.1 | 4.2 | 3.3 | -26.2% |

| 2024 | 2.9 | 4.1 | 4.3 | +25.6% |

| 2023 | 2.3 | 3.7 | 4.0 | +28.9% |

| 2022 | 1.8 | 2.6 | 2.9 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Rev, Capex, Div, FCF. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | ROE% |

|---|---|---|

| 2025 | 1210 | 3948.1 |

| 2024 | 1739 | 1362.7 |

| 2023 | 1128 | 377.7 |

| 2022 | 1308 | 445.1 |

Source: SEC companyfacts cache [F1].

Note: Revenue figures beyond FY2018 not consistently tagged; capex data available only for recent years.

Global Segment Contributions and Geographic Diversification

Colgate-Palmolive organizes its consumer product portfolio primarily into two main segments: Oral, Personal and Home Care; and Pet Nutrition [S18]. Oral, Personal and Home Care is further managed across five geographic segments—North America, Latin America, Europe, Asia Pacific, and Africa/Eurasia—each evaluated principally on operating profit while excluding corporate interest and taxes [S16][S19][S24].

Approximately two-thirds of net sales arise outside the U.S., offering a sizeable footprint within high-growth emerging markets (~45%) that include Latin America, Asia excluding Japan, Africa/Eurasia, and Central Europe [S19]. This exposure provides a natural buffer against region-specific economic cycles and underpins potential revenue expansion driven by rising middle-class consumption patterns.

The geographic segmentation also implies varying margin profiles influenced by regional competitive intensity, currency fluctuations, tariff regimes, and distribution infrastructure effectiveness . For instance, emerging markets typically bear higher market penetration costs but allow for premiumization opportunities through pricing/mix optimization—a critical lever given overall market softness discussed later.

Pension Litigation Impact on Earnings and Risk Management

A defining operational challenge weighing heavily on Colgate-Palmolive’s financials has been the protracted Employee Retirement Income Security Act (ERISA) lawsuit initiated in June 2016 concerning alleged miscalculation of residual annuity payments tied to a Retirement Plan amendment from 2005 [S4][S7]. The case was ultimately certified as a class action with courts affirming plaintiff claims through several stages culminating in final judgments during early-to-mid-2024.

Following unfavorable appellate rulings through April 2025, the company accrued material pension plan liabilities totaling nearly $332 million across Q1 FY2023 ($267 million) and Q1 FY2025 ($65 million) quarters [S7]. These charges contributed directly to compressed net income margins observed for FY2024-FY2025.

In mid-2025, both parties agreed upon a settlement to resolve outstanding controversies subject to court approval [S8][S18], which represented an effort to eliminate further legal uncertainty albeit potentially carrying immaterial incremental cash funding demands based on current funded status analysis.

Importantly, management continues actively monitoring contingent liabilities post-settlement as residual uncertainties around actuarial assumptions remain embedded within disclosures; these risks underscore ongoing pension expense volatility within comprehensive income statements rather than recurring operating profit bases [S8].

Supply Chain Resilience as a Competitive Differentiator

Despite external pressures stemming from global logistics network constraints witnessed industry-wide over recent years, Colgate-Palmolive has leveraged supplier finance programs strategically to maintain working capital agility and enhance supply chain durability [N4][S17]. These programs enable suppliers voluntary pre-financing options via designated financiers without altering contract payment schedules or obligations for Colgate-Palmolive itself.

This structural flexibility permits improved inventory management across diverse markets accommodating local demand fluctuations while mitigating margin erosion linked to freight surcharges or component scarcity . Consequently, operational stability juxtaposes industry-specific headwinds observed among many fast-moving consumer goods peers forced into pass-through inflationing cost models.

Notwithstanding this resilience asset deployment approach aiding short-term margin protection efforts during volatile input cost periods noted earlier aligns recognition that absolute gross margins experienced contraction due to inflationary pressures compressing unit economics albeit partially offset through price/mix enhancements elsewhere.

Future Growth Drivers: Emerging Markets and Product Mix

With approximately two-thirds of net revenues sourced internationally—of which roughly 45% are from emergent economies—Colgate-Palmolive is positioned favorably to benefit from secular consumption upgrades driven by population growth dynamics alongside rapid urbanization trends across Latin America, Africa/Eurasia and parts of Asia Pacific regions [N7][N14].

Within these heterogeneous markets pricing versus volume tradeoffs constitute critical management focus areas amid evolving consumer preferences contra elasticity constraints amid macro softness [N7]. Pricing/mix shifts favor premium SKUs bolstered by innovation in oral care formats or sustainability-themed personal hygiene products carrying higher average selling prices support margin recovery potential if effectively communicated through brand equity channels.

Emerging digital retail platforms likewise present nascent distribution accelerants facilitating faster go-to-market cadence for differentiated offerings targeting younger demographics less reliant on traditional brick-and-mortar footprints . However competitive diversifications may cap rapid expansion given formidable incumbents entrenched locally necessitating calibrated investment prioritizations.

Capital Allocation Strategy: Share Repurchases, Dividends, and Cash Flow Generation

Colgate-Palmolive maintains a balanced but proactive capital return approach fuelled largely by consistent free cash flow generation amounting approximatively $3.5 billion annually (operating cash flow near $4.2B offset by capex about $700M in FY2025) [F1]. During FY2025 alone the company executed share repurchases totaling around $1.21 billion marking continued shareholder value repatriation despite narrower earnings base relative to previous years [F1][S12][S13].

Dividend payout specifics remain undisclosed within tagged filings but historical quarterly dividend continuity complements total yield strategies common among Global Consumer staples leaders ensuring stable income streams relative to equity ownership shares . Equity book values held notably low near $54 million at FY-end signal nominal net asset holdings overshadowed substantially by retiree benefit obligations inflating balance sheet provisions prompting caution interpreting headline ROE calculations that reported elevated excessive percentage levels >3900% annually due primarily to denominator compression rather than true economic leverage Falkenstein phenomenon-like anomaly [F1].

What to Watch: Upcoming Milestones and Market Dynamics

Looking forward stakeholders should monitor judicial progress surrounding the formal court approval of the ERISA settlement agreement which will extinguish major legal contingencies now exposed distinctly during FY2023-25 earnings cycles; any adverse rulings or renegotiations may trigger renewed expense recognition affecting near-term profitability metrics [N2][S14][S18].

Simultaneously tracking shifting consumption volumes versus pricing strategy effectiveness within key emerging markets will be essential particularly against backdrop of macroeconomic discretionary spending softness coupled with inflation variability that could constrain unit growth potential even amidst steady revenues driven by mix uplift campaigns as per latest sector discussions involving peers like Procter & Gamble referencing similar thematic challenges ([N1],[N7]).

Capex deployment trajectories look poised for continuation focused on manufacturing efficiencies alongside product pipeline innovation investments aligned with sustainability commitments observed throughout consumer-packaged goods industries aiming for long-term organic growth stability.

Overall vigilance toward raw material input cost trends balancing supplier finance program efficacy will also serve as important barometers of operational leverage recovery capabilities at an aggregate company level.

Disclaimer: This analysis is based solely on publicly available information as referenced without any proprietary insights or confidential data access. It aims to provide an objective overview without offering investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments