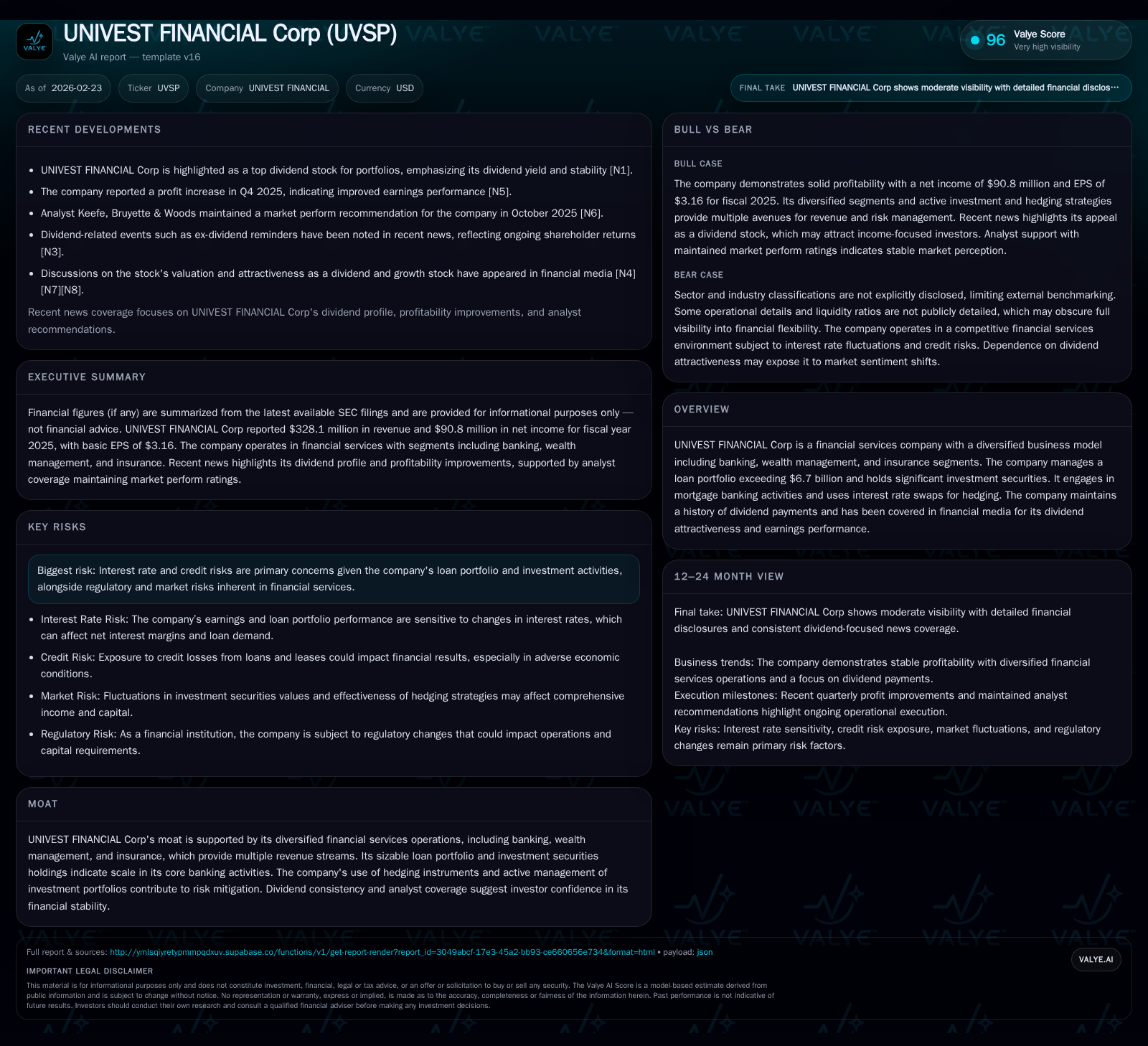

UVSP’s Dividend Appeal and Earnings Growth Define Its Market Position

Univest Financial leverages its diversified financial segments to drive solid earnings growth while sustaining consistent dividends, balancing risk through hedging and capital allocation.

In 2025, Univest Financial Corp (UVSP) posted strong revenue and net income gains underpinned by its diversified operations encompassing banking, wealth management, and insurance. The company’s approximately $6.7 billion loan portfolio, combined with active mortgage banking and hedging strategies using interest rate swaps, supports resilient earnings amid interest rate and credit risks. UVSP has maintained a steady dividend payout coupled with escalating share repurchases, reflecting disciplined capital deployment fueled by improving free cash flow and a roughly 9.6% return on equity. Looking ahead, the company’s multi-franchise model provides growth avenues, but margin pressures and regulatory factors warrant close monitoring.

Revenue and Profit Growth Drivers Through 2025

Univest Financial Corp (UVSP) demonstrated robust top-line momentum in fiscal year 2025, posting revenues of approximately $328.1 million—a healthy increase of 9.6% over the prior year’s $299.2 million figure as reported in their latest filings [F1]. This revenue growth was well accompanied by an almost 20% rise in net income to $90.8 million from $75.9 million in FY2024 [F1]. The surge reflects the effective scaling of multiple revenue streams stemming from its core loan portfolio expansion alongside enhanced mortgage banking activities that contributed meaningful fee income.

This upward earnings trajectory benefits from not only volume growth but also from prudent mix management within its banking services and ancillary offerings such as wealth management and insurance segments. While precise operating income numbers were absent from available filings, net operating cash flow improved markedly by approximately 35%, reaching over $101 million in FY2025 compared with roughly $75 million in the prior year period—underscoring strong underlying cash generation amidst evolving financial market conditions [F1].

Diversified Business Segments Powering UVSP’s Stability

UVSP operates across three primary segments: community banking, wealth management, and insurance services—a structural diversification serving as a moat against single-market shocks [S1]. Its banking segment manages a loan portfolio exceeding $6.7 billion comprising residential mortgages, commercial real estate loans including construction loans, consumer loans including home equity lines, and agricultural financing as outlined across their extensive branch footprint spanning Pennsylvania, New Jersey, Maryland, and Florida [S1]. Residential loans dominate the book but there is significant exposure to commercial financial assets that typically carry higher yields but also varying credit risk profiles.

Mortgage banking contributes additional noninterest income through mortgage origination pipelines supported by forward loan commitments with interest rate locks—a reflection of active balance sheet risk management aimed at preserving fee flow stability despite fluctuating housing market conditions [S2], [S5].

The wealth management segment caters to fiduciary responsibilities including trust assets from retail clients primarily along the Northeast corridor with leased office presences in Allentown PA and Florida [S1]. Insurance operations provide underwriting revenue that supplements recurring earnings though it remains a smaller proportion of total revenue.

Regionally focused branches largely own or lease physical properties with investments also aimed at optimizing land leases for customer convenience while controlling fixed costs—a key consideration given branch profitability pressures pervasive across community banks nationally [S1].

Risk Management via Hedging and Portfolio Mix

Interest rate risk represents a significant factor for UVSP given the typical mismatch between fixed-rate assets such as mortgages versus floating-rate liabilities like deposits. Management employs interest rate swaps designated as cash flow hedges notably on their fixed-to-floating subordinated notes issued in November 2025 with continued reofferings reflected in recent SEC filings—mitigating exposure to rising rates inducing net interest margin compression ([S3],[S4]).

Credit risk is mitigated via conservative underwriting standards with low nonaccrual loan ratios observed as per quarterly disclosures; however geographic concentration presents potential vulnerability should local economic conditions falter especially in commercial real estate sectors which often lead credit cycles [S7],[S17]. Mortgage pipeline exposures to interest rate fluctuations are partially offset through forward commitments and lock mechanisms balanced prudently against market volatility risks.

These hedging frameworks exemplify disciplined enterprise risk management extending beyond traditional deposit betas or NIM guardrails frequently cited by peers in community finance sectors—indicating sophistication appropriate for a bank leveraging multiple franchise businesses.

Dividend Strategy and Shareholder Value Creation

One of UVSP's distinguishing characteristics is its long-standing commitment to steady dividends making it a favored pick among dividend-focused investors highlighted in recent financial media coverage emphasizing yield stability amid industry volatility ([N2],[N5]). Annual dividend payments have hovered near the $25 million mark for several consecutive years despite net income uplifts—reflecting a conservatively managed payout ratio well aligned with cash flow generation capacity seen in operating cash flow surpassing capex needs by over $96 million in FY2025 [F1].

ROE for FY2025 calculated approximately at 9.6% indicates moderate profitability relative to equity base totaling nearly $943 million at year-end — sufficient to sustain dividends without compromising reinvestment opportunities or balance sheet strength [F1]. This provides a nexus for balancing shareholder returns via dividends complemented by opportunistic share repurchases.

Capital Structure Evolution and Share Repurchases

Capital deployment strategies indicate increasing emphasis on share repurchases as evidenced by the near doubling of buybacks from about $18.9 million in FY2024 to an elevated level of $34.6 million in FY2025 while maintaining consistent dividend disbursements simultaneously [F1]. The trend underscores confidence in intrinsic valuation levels while optimizing equity base efficiency.

While detailed maturity schedules or repricing actions relating to indebtedness are sparsely disclosed recently ([S4],[S6]), ongoing exchange offers for subordinated notes during early 2026 suggest proactive interventions stabilizing long-term debt costs. Core deposit balances remain solid forming stable liability funding sources without aggressive reliance on wholesale borrowings.

This capital structure approach enables UVSP to prudently navigate regulatory capital requirements while preserving tactical flexibility—a valuable position compared to peers more constrained by tighter CET1 ratios or aggressive growth mandates.

Emerging Opportunities and Operating Constraints to Monitor

Looking beyond immediate results, UVSP’s prospects hinge on the sustained growth of its diversified franchises—particularly organic loan book expansion feeding into net interest income ramp-up alongside asset-based fees from wealth management client asset appreciation ([N4],[N6]). However, sector dynamics impose some headwinds: margin compression from heightened deposit competition; moderation of mortgage volumes amid fluctuating housing affordability; evolving regulatory scrutiny impacting expense structures; all represent potential operational cost drags or revenue caps.

Analysis also points toward the cautious monitoring of loan credit quality trends particularly within commercial real estate segments sensitive to local economic shifts and rising interest expense environments restricting borrower capacity.

Emerging fintech disruptions could pressure traditional small-to-mid sized regional banks like UVSP regarding operational efficiency and customer acquisition costs though diversification into insurance acts as partial mitigation.

Performance Metrics Table: 2022–2025 Snapshot

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | Capex ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 328 | 91 | 102 | 5 | +9.6% | +19.5% |

| 2024 | 299 | 76 | 75 | 3 | +6.8% | |

| 2023 | 71 | 90 | 7 | -9.0% | ||

| 2022 | 78 | 109 | 5 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): OpInc. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | FCF ($mm) |

|---|---|---|---|

| 2025 | 25 | 35 | 97 |

| 2024 | 25 | 19 | 72 |

| 2023 | 25 | 0 | 83 |

| 2022 | 25 | 11 | 104 |

Source: SEC companyfacts cache [F1].

Note: Revenue formal data unavailable prior to FY2024; all amounts rounded; N/A indicates missing tag data.

Forward-Looking Considerations for Investors

While Univest Financial has not provided explicit numeric guidance recently nor definitive milestones outside routine reporting cycles,[N#]/[S#] neither suggest major near-term inflections beyond execution on existing business lines. Key variables to watch include lending trends responsive to macroeconomic conditions influencing credit demand and quality; mortgage originations affected by consumer housing market activity; further deployment of capital through buybacks or potential strategic investments; sustainability of dividend payouts aligned with cash flows amid evolving earnings profiles.

Given current industry headwinds—such as competitive margin pressure from deposit pricing wars and ongoing regulatory cost burdens—the company’s ability to balance diversification benefits against these constraints will define its medium-term trajectory. Interest rate fluctuations remain a double-edged sword influencing NIM but well-mitigated here through hedging strategies.

In summary, UVSP’s multi-segment platform coupled with disciplined capital allocation frames a steady financial services franchise appealing for income-seeking shareholders while maintaining operational flexibility amidst uncertain macroeconomic conditions.

Disclaimer: This analysis does not constitute investment advice or recommendations; it synthesizes publicly available information up-to the date stated referencing cited sources strictly for informational purposes only.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments