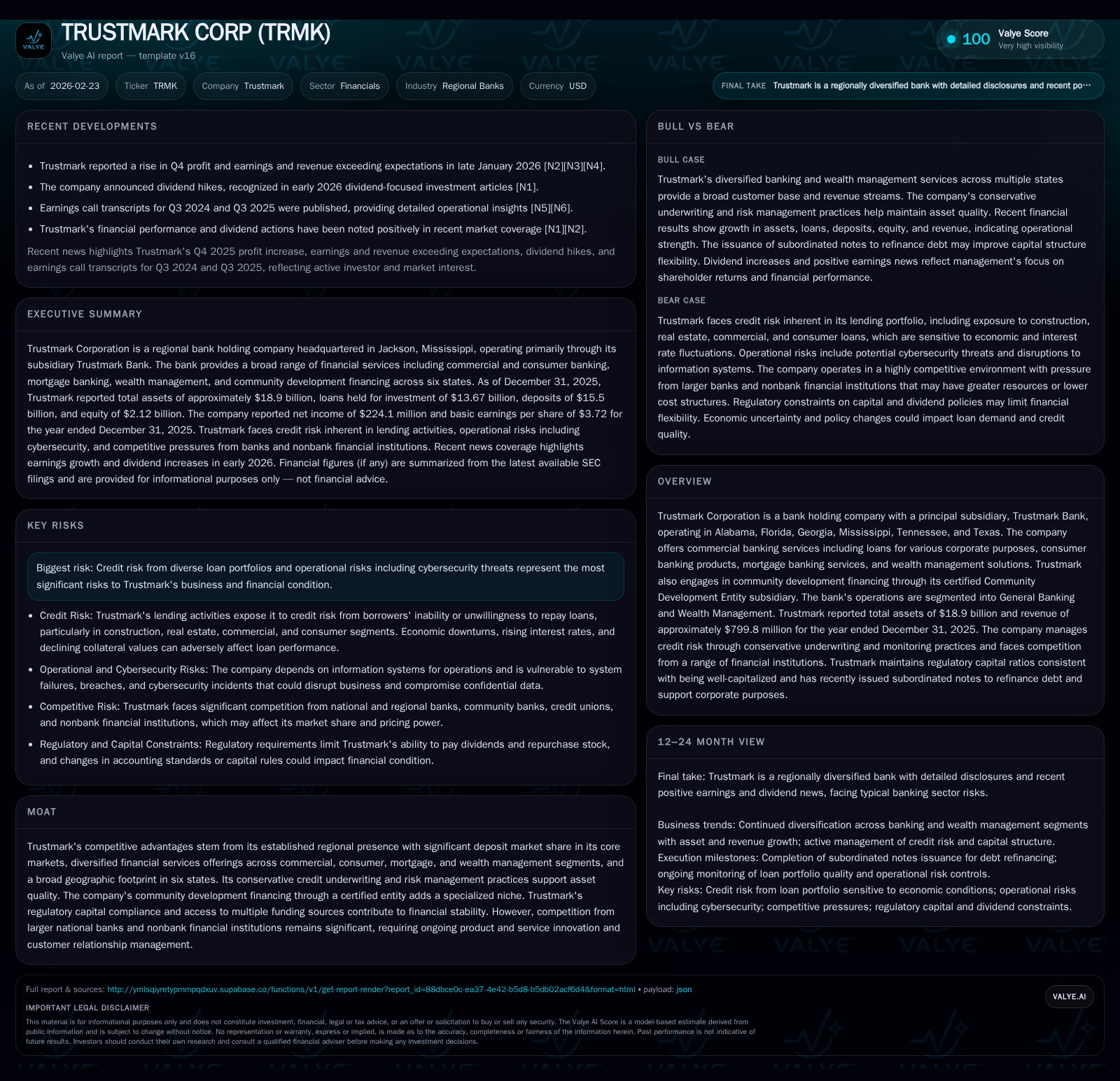

Trustmark Corp Scales Regional Banking with Diversified Services and Robust Capital Discipline

Trustmark’s multi-state presence and conservative credit approach sustain steady profit growth amid competitive pressures.

Trustmark Corporation, operating primarily in six Southern states, has underpinned steady net income growth through a diversified service mix spanning commercial banking, consumer lending, mortgage services, and wealth management. Conservative underwriting and active capital management have supported an approximate 10.6% return on equity despite macroeconomic uncertainties and stiff regional competition. With a strong deposit franchise especially in Mississippi and Alabama, Trustmark balances earnings stability with measured investments in technology and community development financing. Key near-term focus areas include margin trends, deposit gathering efficiency, and maintaining asset quality amid evolving economic conditions.

Historical Growth Trajectory: Earnings Momentum and Segment Contributions

Trustmark Corporation’s financial trajectory from fiscal years 2022 through 2025 illustrates a pattern of consistent profitability improvements. Net income advanced from approximately $71.9 million in 2022 to $224.1 million by year-end 2025, representing roughly a threefold increase over four years but reflecting only about a 0.5% increase between FY2024 ($223.0 million) and FY2025 ($224.1 million) [F1]. This latest plateau underscores stable earnings generation amid moderate growth expectations.

This earnings momentum stems largely from Trustmark's diversified banking model comprising two primary operating segments: General Banking — consolidating commercial loan products, consumer lending, mortgage banking, and deposit services — and Wealth Management offering fiduciary, trust administration, brokerage services, and retirement plan management [S1],[S20]. Commercial banking loans cover a range of corporate financing needs including real estate projects and industrial operations that have historically driven interest income stability.

The bank's strategic regional presence across Alabama, Florida’s Panhandle, Georgia’s Atlanta metro area, Mississippi (its home state), Tennessee (notably Memphis), and Houston in Texas broadens its revenue base with diverse economic drivers [S1],[S10]. This geographic mix helps buffer segmental performance fluctuations derived from localized economic cycles.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|

| 2025 | 224 | 244 | 12 | +0.5% |

| 2024 | 223 | 117 | 23 | +34.8% |

| 2023 | 165 | 197 | 40 | +130.2% |

| 2022 | 72 | 297 | 27 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Rev, OpInc. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | FCF ($mm) |

|---|---|---|---|

| 2025 | 58 | 80 | 232 |

| 2024 | 57 | 7 | 93 |

| 2023 | 57 | 0 | 157 |

| 2022 | 57 | 25 | 270 |

Source: SEC companyfacts cache [F1].

Note: Revenue and operating income data unavailable; table derived from filings [F1].

Portfolio Mix and Underwriting Rigor: Navigating Credit Risk in Diverse Loan Categories

Trustmark maintains conservative underwriting practices across various loan portfolios including commercial industrial loans, owner-occupied real estate financing, land development construction loans, residential mortgages, and consumer installment loans [S1],[S25]. Construction loans carry elevated risk due to collateral incompletion risk; hence stringent credit evaluation is applied alongside ongoing portfolio surveillance.

Nonperforming assets remain low relative to book value aided by early recognition protocols under ASC Topic 326 requiring expected credit losses estimation over loan lifetimes [S17],[S25]. The allowance for credit losses adjusts dynamically based on macroeconomic forecasts that incorporate risks such as tariffs impact and inflationary pressures potentially affecting borrower repayment capacity [S16],[S26]. Charge-offs have been contained evidencing effective risk mitigation strategies.

Consumer loan exposure is managed carefully given unsecured components like credit cards pose higher collection risks versus secured real estate loans [S19]. Technology-enabled monitoring supports early delinquency identification.

Geographic Penetration and Market Share Dynamics Across Core Regions

Trustmark leverages deep-rooted community ties particularly in Mississippi where it enjoys dominant deposit market share exceeding 12%, with consistent top-three rankings across more than half of counties served [S5],[S11]. This franchise provides a reliable funding source critical for supporting loan growth.

Presence in other states such as Alabama (1.87%) and Tennessee (0.30%) complements commercial lending reach notably in metropolitan hubs like Atlanta and Houston [S10]. The bank’s geographic segmentation focuses on trade areas rather than strict state boundaries optimizing customer accessibility while controlling costs.

Competitive pressures arise from larger regional banks and fintech challengers; Trustmark invests in digital channels to enhance convenience while maintaining personalized client engagement valued within community banking contexts [S13].

Capital Allocation Strategy: Dividends, Buybacks, and Return on Equity Analysis

Trustmark demonstrates disciplined capital management balancing shareholder returns with regulatory capital adequacy [F1],[N6],[N7]. Dividends totaled approximately $58 million for FY2025 consistent with prior years despite net income fluctuations indicating commitment to returning cash while preserving capital buffers.

Stock repurchases increased sharply to roughly $80 million in FY2025 compared to minimal activity previously reflecting confidence supported by comfortable regulatory capital ratios above mandated thresholds [F1],[S17],[S23]. Estimated ROE for FY2025 approximates a stable figure near 10.6%, indicating efficient equity utilization aligned with measured growth ambitions.

Wealth Management Segment: Competitive Landscape and Cross-Selling Synergies

The Wealth Management segment contributes meaningful fiduciary services including trust administration, investment advisory mandates, brokerage operations, and retirement plan servicing targeting individual clients as well as institutional customers such as foundations requiring custodial solutions [S20].

Competition includes national banks with integrated wealth platforms alongside boutique advisory firms creating both challenges and opportunities for deeper client wallet share through comprehensive relationship integration [S11]. Trustmark leverages local market knowledge combined with personalized service delivery while upgrading technology infrastructure to enhance client experience.

Liquidity Positioning and Funding Sources Amid Macro Uncertainties

To mitigate liquidity risks heightened by market disruptions or idiosyncratic credit events impacting funding availability, Trustmark maintains secured borrowing capacity via lines of credit from Federal Reserve Bank Atlanta (FRBA) and Federal Home Loan Bank Dallas (FHLB) collateralized by loans held for investment and securities portfolios .

Liquidity risk assessments incorporate scenario modeling of systemic stress alongside institution-specific events quantifying impacts on wholesale funding capacity enabling tactical balance sheet management amidst dynamic interest rate environments.

Financial Statement Trends: Operating Cash Flows and Capital Expenditures Insights

Operating cash flows rebounded strongly in FY2025 reaching approximately $244 million—more than doubling prior year levels—highlighting enhanced cash conversion efficiency from core operations [F1]. Capital expenditures declined nearly by half compared to earlier periods possibly reflecting optimized maintenance spending alongside strategic technology investments or footprint rationalization.

Free cash flow approximates $232 million for FY2025 underpinning internal liquidity supporting debt servicing flexibility plus capacity for shareholder returns or opportunistic acquisitions aligned with strategy.

Risks from Economic Volatility and Cybersecurity: Mitigation Measures and Outlook

Key risks include economic fluctuations influencing loan demand/performance metrics such as potential increases in nonperforming assets or charge-offs triggered by labor market softness or inflation eroding borrower repayment ability [S1,S12,S21,S26]. Geopolitical uncertainties add complexity to forecasting assumptions.

Cybersecurity threats present growing operational risks necessitating investments into intrusion detection systems, multi-factor authentication protocols, comprehensive employee training programs aimed at fraud/data breach mitigation alongside compliance requirements under evolving consumer protection laws increasing operational complexity [S12,S27].

Near-Term Outlook: What Investors Should Monitor From Recent Earnings Calls

Recent earnings calls emphasize monitoring net interest margin trends affected by Federal Reserve policy shifts impacting asset yields/funding costs; deposit acquisition efficiency amid competitive digital alternatives; credit quality indicators including provisioning levels serving as barometers of emerging problem credits requiring agile management response; plus incremental disclosures on wealth management initiatives or mortgage volumes providing insight into diversification benefits enhancing revenue resilience [N3,N4,N7].

This analysis uses information available as of February 23, 2026; developments after this date are not included. It is provided solely for informational purposes without investment advice or recommendation.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments