Evolution Metals & Technologies Builds U.S. Critical Materials Hub Despite Early Losses

EM&T is scaling a vertically integrated rare earth recycling and magnet manufacturing platform to address supply constraints.

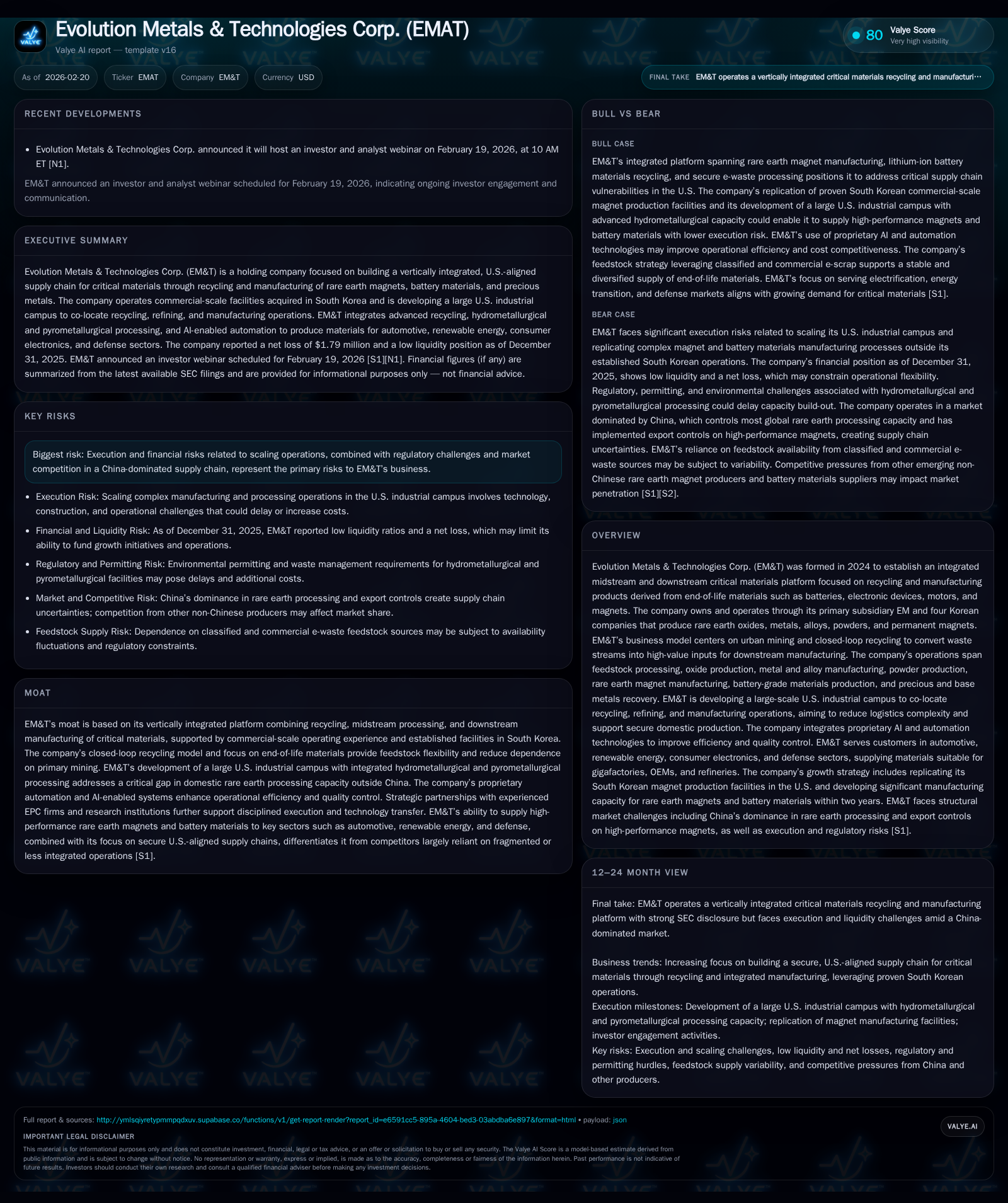

Formed in 2024, Evolution Metals & Technologies Corp. (EM&T) operates an integrated critical materials recycling and manufacturing business with core assets in South Korea and plans a large-scale U.S. industrial campus for midstream and downstream production of rare earth magnets and battery materials. Despite operating losses totaling nearly $2.0 million in 2025 and continued negative cash flows, EM&T’s vertically integrated closed-loop business model aims to reduce U.S. dependency on Chinese processing capabilities. Key growth drivers include replicating proven Korean facilities stateside and leveraging proprietary AI automation technologies. Execution risks remain high given capital intensity, liquidity constraints, and competitive pressures in a China-dominated industry.

Company Overview and Business Model

Evolution Metals & Technologies Corp. (EM&T) was formed in February 2024 as a platform focused on creating an integrated midstream and downstream critical materials supply chain through recycling end-of-life products such as batteries, magnets, electronic devices, and motors into rare earth elements (REEs), battery-grade intermediates, alloys, powders, and finished magnets [S1]. The company became publicly listed following its January 2026 merger with Welsbach Technology Metals Acquisition Corp., serving as a holding company for operating subsidiaries primarily based in South Korea with established commercial-scale manufacturing expertise.

EM&T's vertically integrated operations cover feedstock intake from classified government scrap and commercial e-waste; oxide production; metal and alloy fabrication; powder formation; bonded and sintered magnet manufacturing; battery-grade precursor synthesis; as well as precious and base metals recovery [S19]. This closed-loop 'urban mining' approach enables feedstock flexibility independent of primary mining sources [S19].

Industry Context: Rare Earths Supply Chain Constraints

Global rare earth hydrometallurgical processing capacity is heavily concentrated in China—estimated to control approximately 85-90% of global refining capacity [S10][S22]. This dominance extends to key heavy rare earth elements like dysprosium (Dy) and terbium (Tb), critical for high-performance magnets used across EV motors, robotics, wind turbines, data centers, semiconductor equipment, and defense technologies [S22][S23]. China's export controls significantly restrict availability of these materials outside the country.

Non-Chinese producers have announced roughly 30k tonnes per year of planned rare earth magnet capacity—about 15% of projected non-China demand—with much not expected online until 2028-2030 due to permitting delays and capital intensity [S10]. EM&T aims to address these bottlenecks by replicating its proven Korean operations within the U.S., accelerating capacity deployment while mitigating technology risks [S25].

Historical Financial Performance

Financial disclosures reflect EM&T's recent formation and capital-intensive growth phase without reported revenues yet available. Operating income deteriorated from -$1.58 million in FY2024 to -$2.04 million in FY2025 (a worsening of approximately 28.9%) [F1]. Net losses widened substantially from -$899k in FY2024 to -$1.79 million in FY2025 [F1]. Operating cash flows remain negative but showed slight improvement from -$1.46 million to -$1.33 million year-over-year [F1].

Liquidity is severely constrained with cash & equivalents at just $4k against current liabilities exceeding $9.5 million at fiscal year-end 2025 (current ratio approximately 0.02) [F1]. Shareholders’ equity was deeply negative at about -$12 million reflecting accumulated losses [F1]. No dividend payments were disclosed.

Historical performance (annual)

| FY | Net ($mm) | CFO ($) | OpInc ($mm) | Net YoY |

|---|---|---|---|---|

| 2025 | -2 | -1328287 | -2 | -98.8% |

| 2024 | -1 | -1459263 | -2 | |

| 2022 | -2 | -976306 | -3384.8% | |

| 2021 | 0 | -260825 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Rev, Capex, Div, Buybacks, FCF. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | ROE% |

|---|---|

| 2025 | 14.9 |

| 2024 | 8.3 |

| 2022 | 40.3 |

| 2021 | 5.6 |

Source: SEC companyfacts cache [F1].

Note: Revenue and capital expenditure data are not available from the provided disclosures.

Capital Structure and Liquidity

To support its growth despite limited working capital—evidenced by near depletion of cash reserves—EM&T secured an unsecured bridge loan totaling $80 million at a fixed annual interest rate of 6%, payable quarterly starting March 31, 2026 [S4][S12]. This loan matures shortly after closing but can be prepaid without penalty offering financial flexibility during expansion.

Lock-up agreements restrict share transfers by Korean equity holders post-merger for up to three years enhancing governance stability [S21][S27]. Additionally, indemnification agreements exist for key executives aligning interests during the scale-up phase [S4].

Growth Strategy and Outlook

U.S.-Based Integrated Industrial Campus Development

Central to EM&T’s strategy is constructing a large-scale industrial campus in the United States that consolidates recycling; hydrometallurgical/pyrometallurgical refining; oxide/metal/alloy production; magnet manufacturing; battery intermediate synthesis including sulfates/carbonates/pCAMs; plus precious/base metals recovery operations [S14][S16][S25]. This facility aims to reduce logistical complexities inherent in multi-site or offshore processing while enabling tight process control supported by proprietary AI-enabled automation technologies spanning robotics-driven material handling through quality inspection systems [S7][S24]. The campus targets versatility by processing magnets, lithium-ion batteries, classified government scrap e-waste streams ensuring feedstock diversification [S5][S16].

Capacity Targets Within Two Years:

- Approximately 55,000 tonnes per annum (tpa) rare earth magnet manufacturing capacity producing high-performance magnets containing Dy/Tb sourced entirely from domestically recycled feedstocks without reliance on Chinese inputs.

- Approximately 78,000 tpa battery-grade carbonates/sulfates/pCAMs aligned with U.S.-based gigafactory supply chains.

- Near-zero waste closed-loop secondary metals recovery supporting environmental compliance typical for hydrometallurgical facilities [S25].

Competitive Advantages

EM&T benefits from over 18 years of operational experience via Korean subsidiaries supplying major global OEMs including Ford, Hyundai/LG/Samsung among others [S16][S24]. Replicating these proven processes stateside alongside partnerships with experienced EPC contractors TAEIL Engineering (Korea), Stockwell Engineers (U.S.), research institutions KIGAM and KITECH reduces greenfield risk typically associated with new entrants [S17][S18]. Proprietary AI-enabled smart machinery enhances productivity uncommon among competitors focused on isolated value chain segments [S26].

The company’s tri-segment platform integrates rare earth magnet manufacturing; lithium-ion battery recycling/refining intermediates production; plus secure government/commercial e-waste non-ferrous precious/base metals recovery enabling dynamic capital allocation across streams enhancing margin stability against commodity price volatility typical among single-stream processors [S6][S11][S13][S15].

Risks & Challenges

Execution risks remain significant given the capital intensity of hydrometallurgical facility scale-up compounded by permitting delays related to waste/tailings management alongside consistent access to regulated classified feedstock streams critical for sustained operation at scale [S9][S26]. Liquidity metrics indicate dependence on external financing until positive operating cash flow is achieved while integration complexity of diverse downstream outputs into OEM/gigafactory supply chains remains unproven domestically [F1].

Geopolitical risks persist due to China’s dominant position controlling most rare earth exports underpinning market volatility though also justifying urgent domestic capacity build-out favoring EM&T’s positioning [S22][S23]. Specialized labor shortages specific to hydrometallurgy engineering may constrain timeline acceleration despite the current team size of approximately 42 engineers including PhDs needing further scale-up concurrently [S24][S26].

What To Watch Next: Milestones & Catalysts

- Progress updates on U.S. industrial campus construction milestones including permitting achievements and targeted completion dates.

- Demonstration of first commercial tonnage output from replicated magnet plants within the United States.

- Contract announcements or letters of intent securing off-take agreements with major OEMs or gigafactories indicating market acceptance.

- Development status regarding AI automation integration impacting unit cost structure guiding scalability.

- Additional financing rounds or indications of deleveraging as revenue generation ramps.

- Continuity of feedstock acquisition pipeline especially classified government e-waste crucial for closed-loop economics.

Summary

Evolution Metals & Technologies Corp.’s emergence as an integrated recycler and producer across critical materials addresses strategic supply deficits outside China amidst escalating demand driven by electrification, AI-driven industries, defense modernization, and energy transition sectors.

Despite early-stage financial losses reflecting investment-heavy growth phases — evidenced by a net loss nearing $1.8 million alongside negligible liquidity reserves at fiscal year-end 2025 — management leverages over two decades’ Korean operational pedigree combined with advanced automation technologies mitigating typical greenfield risks.

The company’s development of a comprehensive U.S.-based processing hub scaled for both rare earth magnet production (55k tpa) and battery-material precursors (78k tpa), coupled with diversified end-of-life feedstock sourcing provides a pathway toward resilient domestic supply chains anchored on circular economy principles.

Execution merits close monitoring given complex permitting requirements for hydrometallurgy facilities alongside stiff competition amid China’s dominant market position; however EM&T asserts competitive moats combining vertical integration precision control capabilities plus government-aligned secure feedstock strategies potentially carving differentiated positioning aligned with evolving national security priorities for critical minerals independence.

Disclaimer: This report is based solely on publicly available data as of February 20, 2026 ([F1], [N1], [S#]). It does not constitute investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments