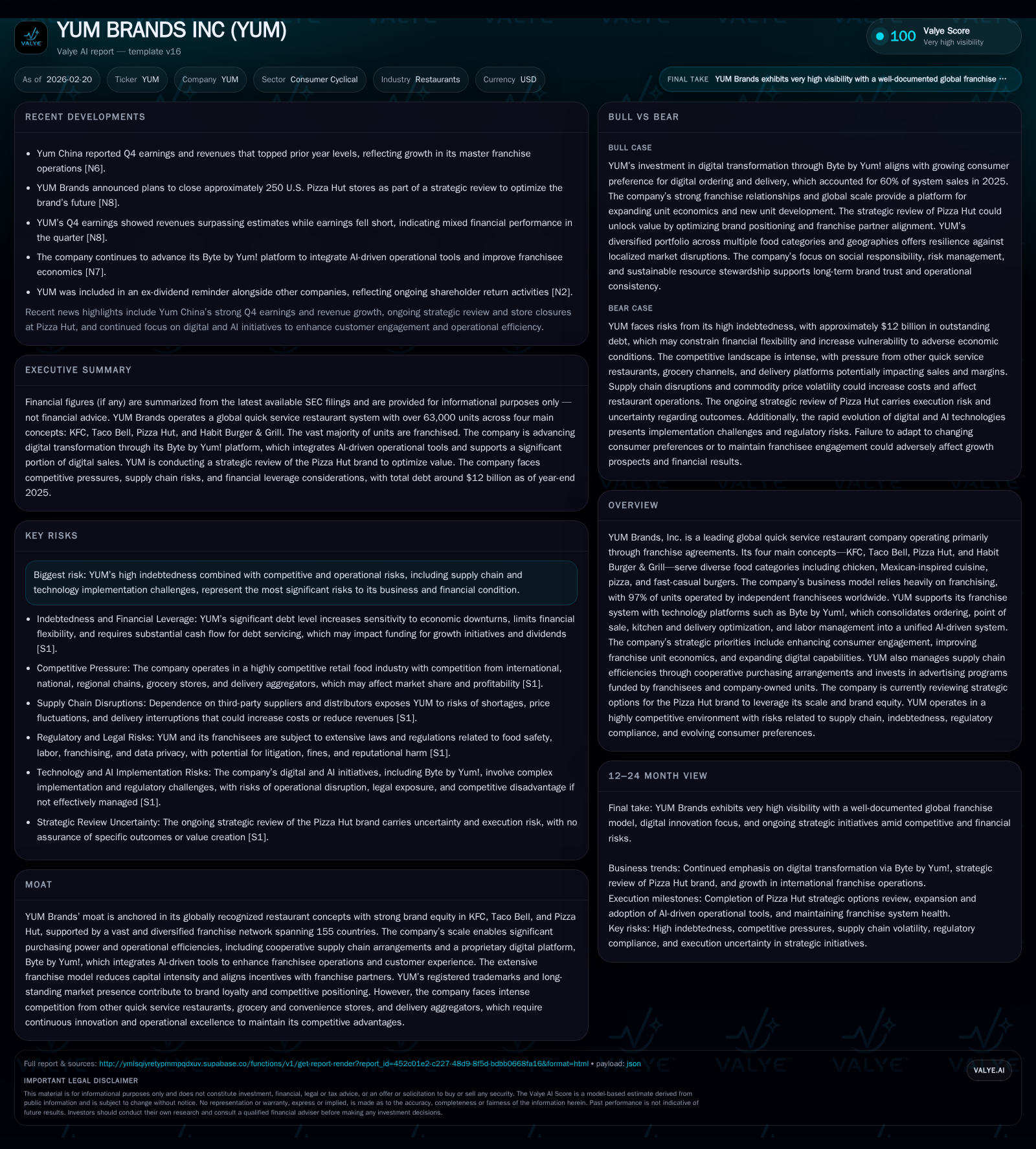

YUM Brands Balances Franchise Growth with Technology-Driven Unit Economics Amid Pizza Hut Strategic Review

YUM Brands integrates AI-powered operations and international franchising with a focused strategy to enhance unit economics and brand performance.

YUM Brands, a global leader in quick service restaurants with iconic brands like KFC, Taco Bell, Pizza Hut, and Habit Burger & Grill, continues its growth trajectory supported by a dominant franchise model and technology integration. Revenue and operating income expanded nearly 9% and 7% year-over-year respectively in 2025, underpinned by digital sales approaching 60%. The company is undertaking a strategic review of Pizza Hut to optimize brand value, while investing heavily in its proprietary Byte by Yum! platform to drive operational efficiencies and franchisee profitability. Despite facing risks from high indebtedness, supply chain volatility, and intense competitive pressures, YUM maintains robust cash flows that fund dividends and buybacks, albeit with a negative book equity position affecting ROE calculations.

Company Overview and Historical Performance

YUM Brands Inc. (ticker: YUM) stands as a foremost quick service restaurant (QSR) operator globally, primarily leveraging an extensive franchised restaurant model that encompasses four leading concepts: KFC (chicken), Taco Bell (Mexican-inspired cuisine), Pizza Hut (pizza), and Habit Burger & Grill (fast-casual burgers). As of December 31, 2025, YUM’s system comprised over 63,000 restaurants spanning 155 countries with franchisees operating roughly 97% of units worldwide [S1]. This scale confers significant purchasing leverage and operational advantages.

Financially, YUM has demonstrated consistent top-line growth over recent years driven mainly by unit growth in emerging markets coupled with comparable sales gains in digital channels. Revenues expanded from $6.84 billion in FY22 to $8.21 billion in FY25, representing a compound annual growth rate (CAGR) of about 6.6%. Operating income grew steadily by just over 17% between FY22 and FY25 to reach $2.57 billion in the latest reported fiscal year [F1]. Net income rose from approximately $1.33 billion in FY22 to about $1.56 billion in FY25.

Historical performance (annual)

| FY | Rev ($bn) | Net ($mm) | CFO ($bn) | OpInc ($bn) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 8.2 | 1559 | 2.0 | 2.6 | +8.8% | +4.9% |

| 2024 | 7.5 | 1486 | 1.7 | 2.4 | +6.7% | -7.0% |

| 2023 | 7.1 | 1597 | 1.6 | 2.3 | +3.4% | +20.5% |

| 2022 | 6.8 | 1325 | 1.4 | 2.2 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Capex. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | FCF ($mm) |

|---|---|---|---|

| 2025 | 789 | 552 | 1639 |

| 2024 | 752 | 441 | 1432 |

| 2023 | 678 | 50 | 1318 |

| 2022 | 649 | 1200 | 1148 |

Source: SEC companyfacts cache [F1].

Note: Net YoY for FY24 reflects post-pandemic margin normalization effects before resuming growth.

Operating cash flow improvement outpaced revenue gains demonstrating effective working capital management alongside disciplined capital spending focused on digital upgrades and system enhancements [F1]. Capital expenditures jumped notably (+44%) in FY25 primarily due to technology investments such as Byte by Yum!. The company continues steady commitments to dividends and share repurchases supporting total shareholder return.

Franchise Model Strengths and Brand Moat

YUM’s business model is anchored on licensing its brands predominantly via franchise agreements with local operators who pay continuing fees based on restaurant sales coupled with mandatory advertising contributions managed through cooperatives [S9,S24]. This structure provides recurring revenue streams with limited operating risk or capital intensity.

Brand equity remains formidable: KFC leads global chicken QSR segments internationally; Taco Bell is dominant among Mexican-inspired competitors; Pizza Hut retains substantial scale despite challenges; Habit Burger & Grill targets the growing fast-casual segment albeit still comprising under 1% of overall footprint [S1]. These diverse offerings mitigate exposure to any single cuisine trend or geographic market volatility.

The company's moat extends beyond branding into operational efficiency benefits realized through centralized cooperative purchasing arrangements such as Restaurant Supply Chain Solutions LLC that combine buying power of franchisees across regions lowering input costs [S12]. The proprietary Byte by Yum! platform represents a critical digital asset aiming to unify ordering systems, point-of-sale terminals, kitchen workflows, labor scheduling optimization, and delivery logistics into an AI-driven ecosystem enhancing both consumer experience and franchisee margins [S9,S17]. Its rollout symbolizes YUM’s commitment to digital transformation differentiating it from peers reliant on fragmented third-party technologies.

Key Growth Catalysts and Strategic Priorities

Looking forward into its Recipe for Good Growth strategy advanced through the Raising the B.A.R framework, YUM emphasizes three interconnected priorities:

- Battle for the Future Consumer: Deepening engagement by anticipating evolving tastes and consumption patterns;

- Accelerate Unit Economics: Empowering franchise partners to optimize restaurant-level profitability fueling reinvestment;

- Reach Full Potential of Byte by Yum!: Scaling this platform globally to drive smarter data-driven operations unlocking incremental sales and cost efficiencies [S17].

Notably, the ongoing review of strategic options for the Pizza Hut brand signals potential restructuring or renewed franchising models aiming to revitalize this legacy pizza concept facing intensified competition from delivery-focused chains and grocery-prepared meals [S1,S14]. Outcomes remain uncertain but will materially shape YUM’s future footprint composition.

Further catalyst areas include geographic expansion particularly outside the U.S., targeted unit growth among high-margin/digital-savvy outlets, menu innovation aligned with health/wellness trends despite consumer complexity around nutrition perceptions, enhanced supply chain resilience amid inflationary pressures, and continuing automation/adoption of AI tools to stay ahead operationally versus other QSR rivals who are also accelerating tech investments [S6,S7,S8,S9,N12].

Risks Constraining Growth Potential

Several factors impose constraints or downside risks threatening YUM's growth outlook:

- Leverage & Financial Structure: The company carries elevated indebtedness which exposes it to refinancing risk amid volatile capital markets; equity remains substantially negative reflecting aggressive prior buybacks limiting ROE clarity (-20% approx.) despite positive net earnings [F1,S21];

- Food Safety Concerns: Historical instances of food-borne pathogens or supply issues could damage brand trust catastrophically considering reliance on third-party suppliers plus expanding role of delivery aggregators amplifying risk vectors; regulatory scrutiny around packaging substances adds complexity [S1,S16];

- Competitive Forces: Beyond entrenched rivals like McDonald’s or Wendy’s ([N3]), emergent digital native brands plus grocery meal solutions have fragmented consumer spend further raising marketing spend needs; maintaining distinct brand relevancy will require ongoing innovation at considerable cost [S6,S22];

- Regulatory & Legal Exposure: Complex multinational compliance burdens including evolving data privacy laws such as GDPR/U.S.-state statutes impose rising compliance costs coupled with litigation risks across trade secrets/IP infringement/franchise disputes; labor classification laws may disrupt operational models if joint employer definitions broaden again [S4,S18,S23];

- Macroeconomic & Supply Chain Pressures: Inflationary costs for raw materials particularly proteins challenge passing price increases fully onto customers due to price sensitivity; labor shortages constrain unit capacity; geopolitical instability impacts currency exposure especially RMB convertibility issues affecting royalty remittances from China master franchisee Yum China Holdings [S20,S22];

- Changing Consumer Preferences: Heightened nutritional awareness fueled by studies on ultra-processed foods combined with popular weight-loss treatments could depress demand for traditional fast food items necessitating menu adaptations potentially reducing margins [S8].

Capital Allocation and Returns Analysis

Despite financial headwinds related to leverage-induced negative book equity metrics (~-$7.5 billion end-Q3/25), YUM delivers strong cash conversion returns benefiting from light asset ownership due to franchising focus.

Operating cash flow increased almost +19% from $1.69 billion in FY24 to $2 billion in FY25 supporting capex levels which climbed sharply due primarily to digitization projects totaling $371 million last year representing close to a fivefold increase relative to ten years prior rates cited historically . After deducting capex from CFO yield strong free cash flow exceeding $1.6 billion enabling sizable dividend distributions ($789 million in FY25) alongside substantial share repurchases totaling over half a billion dollars annually since FY24 after near pauses earlier this decade consistent with the firm’s policy emphasizing balanced return of capital while investing digitally for longer-term unit economics improvement [F1].

Return on equity approximates negative territory given large accumulated deficit but does not reflect underlying cash generating ability or intrinsic brand equity sustained through franchising economics typical for asset-light restaurant operators bearing largely operating lease obligations off balance sheet rather than property ownership.

Industry Context: Digital Ordering & AI Integration Critical for Future Relevance

Analysis: The quick service restaurant sector has witnessed rapid digitization driven by consumer preference shifts post-pandemic toward convenience and contactless ordering systems often facilitated via mobile apps or kiosks - trends that account for a majority portion of system sales at YUM (nearly $40 billion digital sales corresponding to ~60% of overall system revenues in FY25). Competitors are accelerating use of AI not only in front-end customer engagement but also back-end labor optimization scheduling software leveraging predictive analytics—Byte by Yum! exemplifies this sector-native approach crucial for sustaining margins amid tight labor markets and rising wage floors.

Consequently, success increasingly depends on owning proprietary technology platforms integrating multiple operational facets rather than relying solely on standalone third party vendors thereby creating sustainable competitive differentiation within mature QSR categories flooded with copycat menu items but fewer tech incumbents able to drive system-wide improvements effectively.

Conclusion

YUM Brands remains well-positioned as a global quick service powerhouse blending extensive franchising scale with targeted investment in innovative technology platforms like Byte by Yum!. Its broad portfolio spanning several large-category segments provides diversification not often seen at this magnitude though risks tied to legacy brands such as Pizza Hut require strategic clarity pending outcomes expected later this year.

The company’s disciplined capital allocation balancing shareholder returns against necessary digital transformation spending reflects prudent stewardship underpinned by growing operating cash flows notwithstanding underlying leverage constraints impeding equity-based profitability metrics.

Operational agility addressing cost inflation headwinds while navigating complex regulatory landscapes worldwide combined with continuous enhancement of franchisee unit economics will likely determine how successfully YUM can maintain its moat amid intensifying competitive disruptions within evolving consumer dining preferences.

This report is prepared solely for informational purposes based on publicly available data including SEC filings ([S#]) and news sources ([N#]). It does not constitute investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments