Lumen Technologies Refocuses on Enterprise Growth After Major Divestiture

Following the sale of its Mass Markets Fiber-to-the-Home business, Lumen pivots toward enterprise solutions powered by AI and network modernization.

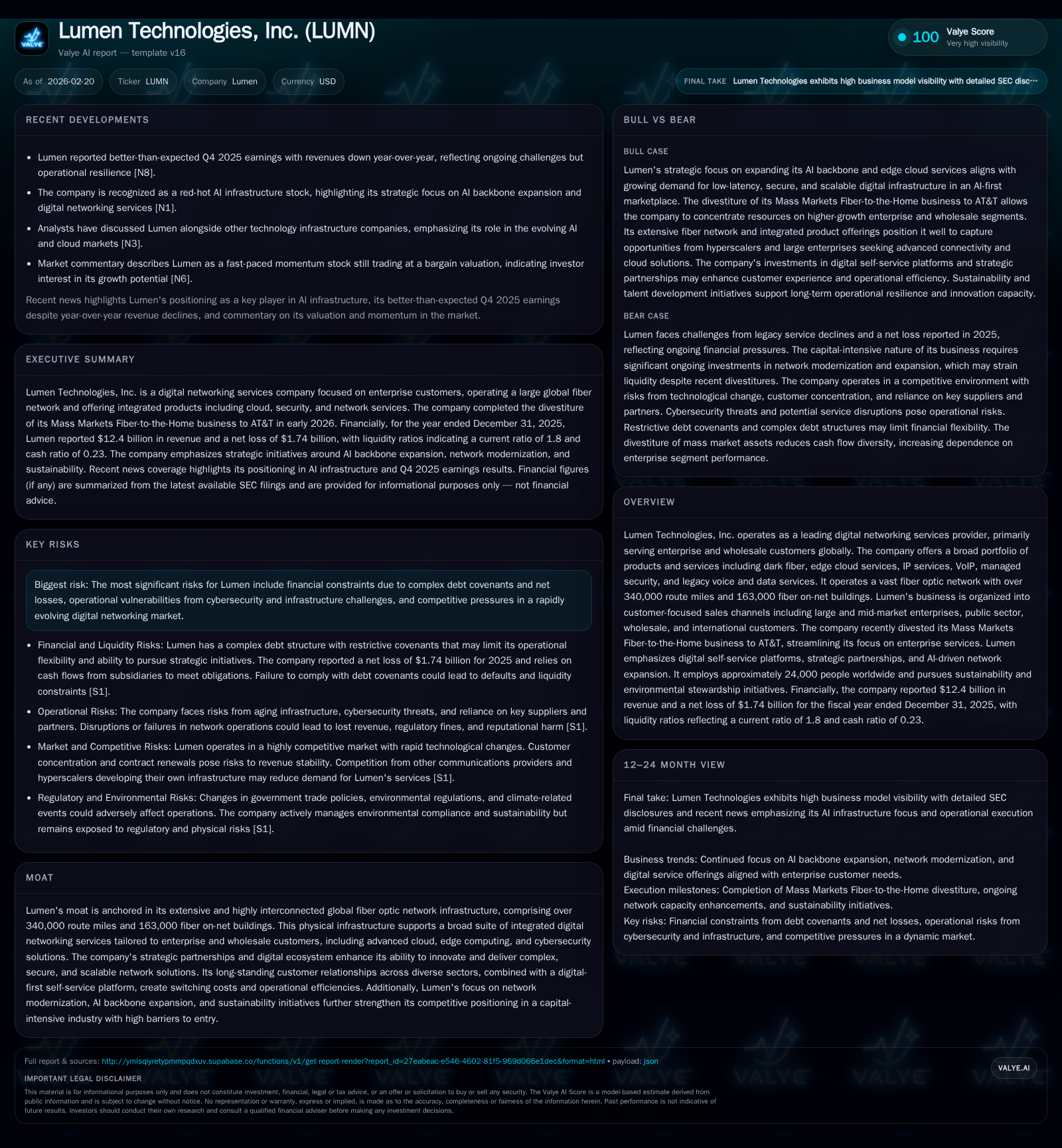

Lumen Technologies has sharply reoriented its business model after divesting its consumer fiber broadband segment to AT&T in early 2026. Historically marked by declining revenues and volatile profitability driven by legacy service erosion, the company aims to leverage its extensive fiber infrastructure and AI-driven network capabilities to regain growth in enterprise markets. Despite generating strong operating cash flow, Lumen faces financial stress evidenced by recurring net losses and a negative equity position, raising concerns about debt covenant compliance and capital allocation. Key milestones to watch include the ramp-up of its PCF solutions and edge cloud services amidst industry demand for high-bandwidth, low-latency networks.

Historical Performance: Revenue Declines and Mixed Profitability

Lumen Technologies’ financial trajectory over the last four fiscal years reveals pronounced revenue contraction alongside volatile operating results, symptomatic of its shifting industry dynamics.

Historical performance (annual)

| FY | Rev ($bn) | Net ($bn) | CFO ($bn) | OpInc ($bn) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 12.4 | -1.7 | 4.7 | -0.8 | -5.4% | -3061.8% |

| 2024 | 13.1 | -0.1 | 4.3 | 0.5 | -10.0% | +99.5% |

| 2023 | 14.6 | -10.3 | 2.2 | -9.6 | -16.7% | -565.2% |

| 2022 | 17.5 | -1.5 | 4.7 | 0.1 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Capex, FCF. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | ROE% |

|---|---|---|---|

| 2025 | 1 | 155.7 | |

| 2024 | 3 | 0 | -11.9 |

| 2023 | 11 | 0 | -2469.5 |

| 2022 | 780 | 200 | -14.8 |

Source: SEC companyfacts cache [F1].

Note: Capex annual data not fully available post-FY2013; approximate levels historically steady near $3B.

Over these years, revenues declined by approximately 29%, primarily due to systemic declines in legacy voice and data offerings compounded by competitive substitution effects typical within digital networking sectors[F1]. The operating income swings are stark—FY2023 suffered a massive loss linked to substantial non-cash impairment charges attributed to restructuring and divestiture activities including Latin American assets [S26]. Although there was some rebound in FY2024 with positive operating income, FY2025 again saw losses driven by ongoing transition costs.

Notwithstanding bottom-line headwinds, Lumen’s ability to generate operating cash flow remained resilient at $4.74 billion in FY2025[F1], underscoring the cash-generative nature of core fiber assets that underpin enterprise services while supporting significant capital expenditures.

Impact of Mass Markets Divestiture: Strategic Shift and Capital Influx

On February 2, 2026, Lumen completed the divestiture of its Mass Markets Fiber-to-the-Home business covering an 11-state territory to AT&T for gross proceeds of $5.75 billion[S6][N9]. This deal marks a critical pivot away from residential and small business broadband operations toward an exclusive focus on enterprise-grade digital networking services.

This transaction effectively eliminates Lumen’s Mass Markets segment as defined through FY2025 reporting periods[S4][S6], consolidating all continuing activities under the Business segment tailored around large enterprises, mid-market enterprises, public sector entities, wholesale partners, and international customers.

Strategically this improves agility by shedding lower-margin consumer-facing operations burdened with legacy copper infrastructure obligations while releasing substantial liquidity that can be redeployed into growth areas such as Platform Centric Fiber (PCF) deployments and AI-driven network upgrades[N9]. However, it also contracts the overall revenue base substantially given that mass market broadband represented a meaningful portion of prior topline[S6]. The divestiture frees up fiber assets previously used for residential reach which could now be optimized for higher-value enterprise connectivity projects.

Enterprise Segment Focus: Toward AI-Driven Network Solutions

Post-divestiture Lumen doubles down on digital networking products aimed at enterprises demanding complex integration with multi-cloud environments and emerging AI workloads[S8][S22]. Their flagship "Lumen" brand encapsulates this shift offering comprehensive service portfolios including:

- Dark Fiber & Conduit access enabling clients to construct private high-capacity optical networks with low latency suitable for AI training and inference connectivity.

- Edge Cloud Services designed to extend cloud capabilities closer to data sources reducing round-trip times critical for AI applications requiring real-time responsiveness.[S8]

- Managed Security Services operated via Black Lotus Labs that deliver DDoS mitigation and threat intelligence proactively guarding sensitive enterprise data flows.

- Network-as-a-Service (NaaS) provision facilitating flexible bandwidth scaling aligned with on-demand computing needs inherent in federated cloud models.

Lumen’s physical plant covers over 340,000 route miles of fiber globally connecting approximately 163,000 fiber on-net buildings[S8][F1] — an expansive footprint instrumental for delivering integrated PCF architectures that optimize cost efficiencies while managing latency constraints increasingly pivotal for performance-sensitive AI traffic flows.

The company’s forward narrative emphasizes expanding their "AI backbone" infrastructure incorporating digital self-service platforms supported by advanced automation enabling customers to configure network topologies dynamically[S6][N5]. This positions Lumen as a critical hybrid connectivity enabler bridging hyperscaler ecosystems with distributed enterprise sites.

Operating Challenges and Risks: Legacy Systems, Cybersecurity, and Competition

Transitioning from entrenched legacy copper-based networks toward fully integrated digital platforms imposes substantial execution risk involving system integration overheads across hardware-software boundaries[S1]. Modernizing master data management processes while retiring obsolete architectures continues as a gating factor for realizing operational efficiencies promised in strategic plans.

Cybersecurity threats remain acute given Lumen’s role as a conduit for sensitive enterprise data; technical gaps or breaches could incur regulatory penalties under evolving U.S., EU data privacy regimes plus customer contract liquidated damages exposure[S13][S14]. The firm acknowledges operational complexities stemming from the increasing use of AI internally—highlighting governance challenges over ethical algorithm deployment alongside heightened cyber vulnerabilities inherent in interconnected network fabrics[S14].

Financially onerous debt agreements impose strict covenants limiting discretionary capital actions including dividend distributions or asset sales[S7][S15]. The company faces potential covenant default risk if operating performance deteriorates or liquidity tightens unexpectedly prompting acceleration clauses across interlinked debt instruments which could exacerbate refinancing difficulties.

Competition intensifies as hyperscalers invest heavily in building proprietary fiber routes potentially bypassing incumbent providers like Lumen[S11]. Market commoditization pressures pricing even on next-gen products necessitating constant innovation pace lest erosion continue—an acute challenge given constrained capital capacity.

Capital Allocation Dynamics: Debt, Cash Flow, and Shareholder Returns

Despite severe headline net losses totaling approximately $1.7 billion in FY2025[F1], Lumen generated $4.74 billion in operating cash flow maintaining sector-relative robust liquidity levels including about $1 billion held in cash equivalents plus a current ratio near 1.8 suggesting short-term obligation coverage capacity[F1][S7].

Capital expenditures traditionally exceed $3 billion annually reflecting ongoing investments maintaining one of North America’s largest terrestrial fiber networks[F1] though recent exact figures post-FY2013 are unavailable publicly.

A notable feature is the precipitous decline in shareholders’ equity turning markedly negative at approximately -$1.12 billion by end-FY2025 driven by accumulated operating losses eroding retained earnings[F1]. This anomaly complicates conventional return on equity calculations which would misleadingly show excessively high magnitudes given negative denominator values—hence ROE is not meaningful here.

Dividends have been slashed dramatically from $780 million paid out in FY2022 to a token $1 million by FY2025 while share repurchases came to a halt after substantial buybacks ceased post-2022 campaign reflective of prudent capital stewardship amid financial stress conditions.[F1]

Overall capital allocation reflects prioritization of sustaining network buildout paired with stringent cash preservation while managing intricate debt portfolio collectively restraining return policies or aggressive shareholder distributions.

Outlook and Analytical Considerations: Growth Prospects and Key Milestones

Explicit forward guidance from Lumen remains conservative yet optimistic around the gradual ramp in demand for AI-centric connectivity services being a key growth vector fueling new PCF contract rollouts alongside associated edge cloud service expansion[N5][N7]. Monitoring successful execution milestones on delivering turnkey PCF builds within permissible capex envelopes will serve as leading indicators.

Liquidity management will remain pivotal given restrictive covenants embedded within multi-layered debt structures requiring diligent compliance reporting complemented by scenario modeling amid macroeconomic uncertainties impacting borrowing costs or refinancing conditions.

Competitive positioning will depend heavily on maintaining technological parity or superiority versus vertical-integrated hyperscalers plus responding nimbly to shifting customer preferences favoring bundled or managed service consumption models over raw connectivity sales.[N9][S22]

Supply chain continuity including sourcing critical optical components contributes additional operational considerations requiring robust vendor risk assessments.

Lastly regulatory developments encompassing data privacy regime tightening as well as environmental remediation related to legacy materials such as lead-sheathed cables may impose unplanned costs or operational restrictions warranting monitoring.[S13][S25]

Disclaimer: This report presents an analytical summary based exclusively on publicly disclosed information from SEC filings and reputable news sources without offering any investment advice or price targets.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments