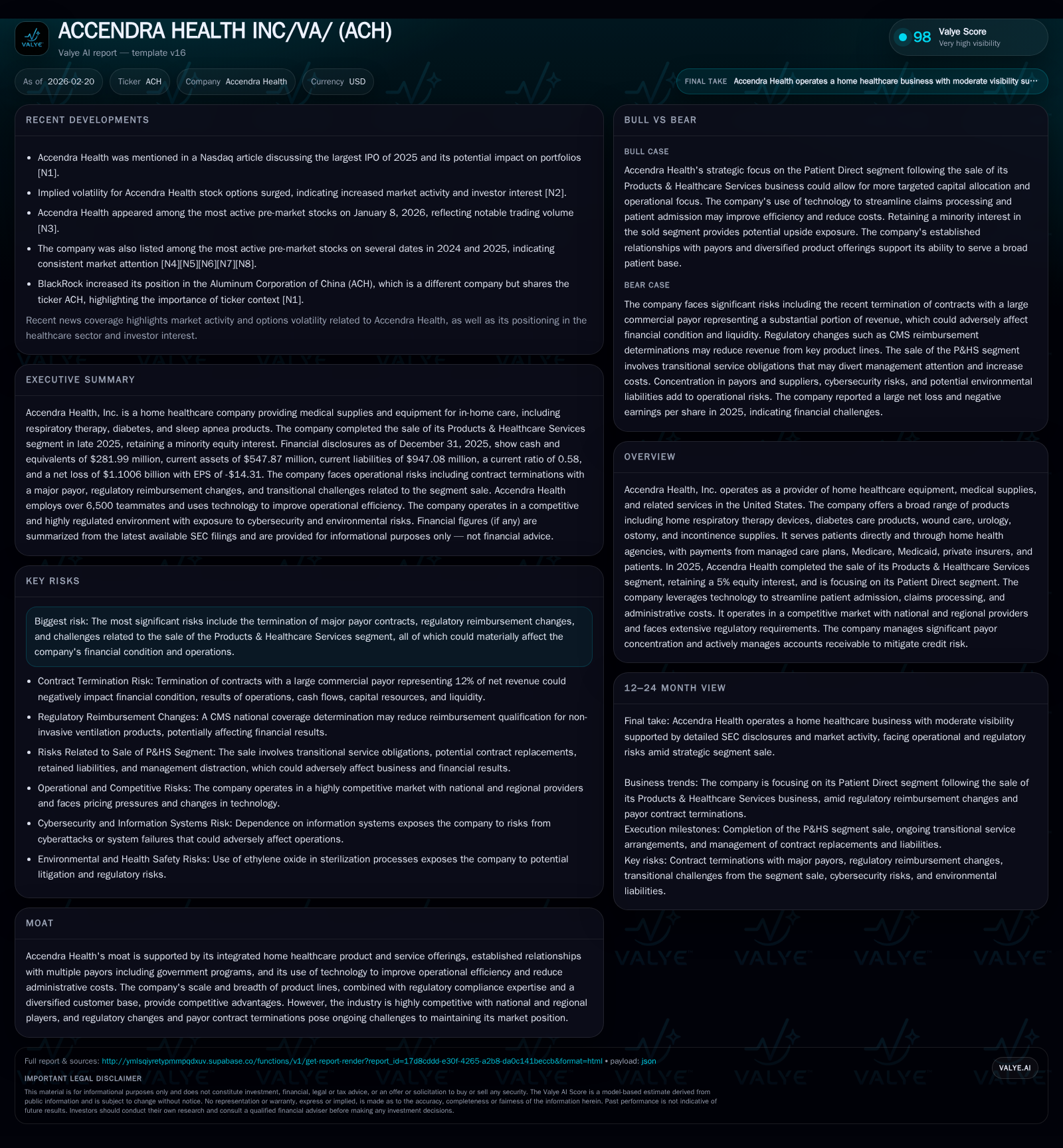

Accendra Health’s Revenue Pressure and Regulatory Risks Impact Profitability and Equity

The company faces substantial earnings volatility amid payor contract losses and a strategic focus shift following a divisional sale.

Accendra Health, a U.S. home healthcare equipment and supply provider, recently divested its Products & Healthcare Services segment while concentrating on its Patient Direct segment. Despite operating income recovering in 2025 after prior losses, the company reported a significant net loss driven by heavy impairment charges and operational challenges. Key risks include termination of sizeable payor contracts, evolving reimbursement frameworks, and regulatory compliance complexities. Capital allocation remains cautious with modest share repurchases but no dividends, while liquidity metrics show strain due to high current liabilities relative to assets. Investors should monitor payor contract renewals and margin pressures as key near-term milestones.

Historical Financial Performance

Accendra Health experienced significant fluctuations in profitability over the last four fiscal years ending December 31, culminating in the recent fiscal year with a dramatic turnaround in operating results followed by an even more severe net loss.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -1101 | 27 | 191 | -203.5% | |

| 2024 | -363 | 161 | -208 | 211 | -778.2% |

| 2023 | -41 | 741 | 105 | 191 | -284.5% |

| 2022 | 22 | 325 | 143 | 158 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Rev, Buybacks. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 238.8 | ||

| 2024 | -49 | -64.2 | |

| 2023 | 0 | 550 | -4.5 |

| 2022 | 0 | 167 | 2.4 |

Source: SEC companyfacts cache [F1].

Note: Revenue data is not available from provided tags; CFO for FY2025 is not fully tagged.[F1]

The positive swing in operating income in FY2025 versus FY2024 was mainly due to the sale of the Products & Healthcare Services (P&HS) segment completed during the year, wherein Accendra retained a minority equity stake but shifted focus onto its Patient Direct segment [S1][N1]. However, this restructuring yielded large goodwill impairments and sizeable one-time costs leading to a record net loss exceeding $1 billion despite positive operating profit.

Operating cash flows reversed to negative territory after several years of strong generation, while capital expenditures remained elevated reflecting ongoing investments in property, plant and equipment relevant to Patient Direct operations or technological integration efforts [F1][S9].

Strategic Positioning and Industry Context

Accendra Health operates as a major U.S.-based provider of home healthcare equipment spanning respiratory therapy devices, diabetes care products, wound care supplies, urology/ostomy/incontinence aids among others. These products are often rented or sold directly to patients or through home health agencies reimbursed by a mix of government programs (Medicare/Medicaid), private insurers, managed care plans and occasionally patients themselves [S9].

The company’s moat rests on its integrated product-service offering combined with scale benefits that support negotiating power with both suppliers and payors alongside compliance expertise navigating complex federal/state regulations that govern all layers of home healthcare supply chains .[N9]

Digital transformations such as web portals for electronic ordering, automated claims processing systems, and electronic funds transfers drive operational efficiency improvements intended to reduce administrative overhead cost structures — a critical factor given industry margin pressures [S9].

Yet the landscape remains intensely competitive featuring numerous national players plus regional specialists vying for dominant positions via contract wins with payors and referrals from hospitals / physicians connected to patient discharge flows [S9].

Future Growth Prospects: Drivers & Constraints

Accendra's future growth potential hinges on successfully expanding its Patient Direct segment post-P&HS sale while mitigating risks from payor contract terminations.

Growth Drivers:

- Leveraging proprietary technology platforms to streamline patient acquisition and claims adjudication may enable higher volumes at lower cost.

- Broadening product mix tailored to chronic disease management trends will be favorable as aging demographics increase demand for home healthcare supplies.

- Building deeper contracting relationships with managed care organizations could provide more stable revenue streams despite changes in reimbursement paradigms.

Potential Constraints:

- The termination by a large commercial payor of contracts accounting for approximately $322 million or ~12% of revenue signals material risk exposure which may suppress top-line if new agreements are delayed or less favorable [S2][S22].

- Regulatory changes impacting Medicare/Medicaid reimbursement rates under Competitive Bidding Programs (CBP) can introduce persistent pressure on margins and volumes [S19].

- Supplier concentration presents operational vulnerability especially if alternative sources cannot match quality or pricing leading to fulfillment delays or cost inflation [S11].

- Ongoing compliance requirements under fraud & abuse statutes (Anti-Kickback, Stark Law), plus intensive FDA licensing/regulatory standards raise operational complexity with potential financial penalties for infractions [S4–S7][S20].

Forecasts and Milestones to Watch

Although explicit forward guidance was not provided in disclosed filings or news reports up to early 2026[N#], several milestones bear close monitoring:

- Payor Contract Renewals: Outcome of negotiations particularly related to large commercial payors who recently terminated agreements but continue service transitions into mid-2026 constitutes a critical performance indicator affecting revenue stability[S2].

- Integration Progress: Efficiency gains from technology investments targeting faster patient onboarding combined with claims process improvements represent key vectors toward restoring cash flow generation[S9].

- Regulatory Audits/ Investigations: Given government scrutiny levels exemplified by Apria-related settlements embedded within Accendra’s history, ongoing audit results or corporate integrity agreement developments will significantly impact operating risks[S6][S7].

- Competitive Bidding Program Outcomes: Re-bidding cycles affect Medicare reimbursements intermittently influencing contract profitability profiles[S19].

Returns and Capital Allocation Trends

Return on Equity (ROE) for FY2025 appears anomalously negative due primarily to net loss coupled with negative shareholders’ equity at about -$461 million compared to positive equity in prior years[F1], reflecting write-downs associated with divestiture impairments.

Free Cash Flow (CFO minus Capex) swung negative by nearly $29 million suggesting operational cash challenges that may constrain discretionary spending[CFO-$162M caps minus CAPEX-$191M caps].[F1]

Dividend distributions have ceased since before FY2023 aligning with conservative capital management amid restructuring[S25], but share repurchase programs restarted modestly in early-to-mid 2025 totaling approximately $10 million thus far indicative of selective return of capital while maintaining balance sheet flexibility[S25].

Liquidity indicators require attention: current assets at $548 million versus current liabilities near ~$947 million denote a sub-one current ratio (0.58), amplifying short-term solvency concerns absent near-term working capital improvements[F1].[S17]

Regulatory Environment & Legal Risks

Accendra operates within an intensely regulated environment involving multiple overlapping federal/state statutes:

- Compliance with Anti-Kickback Statutes and Stark Law limits referral-related revenues requiring stringent internal controls[S4–S6][S18],[S26]; noncompliance risks costly penalties including exclusion from government programs.

- Data privacy governed by HIPAA alongside emergent state consumer data protection laws such as CCPA/CPRA exposes the company to fines or reputational damage from breaches or procedural lapses[S20],[S23].

- Manufacturing facilities subject to FDA cGMP regulations face ongoing surveillance risks; failures can force recalls or production halts impacting supply reliability[S8],[S16].

- Litigation exposure linked historically to improper billing settlements adds further cost uncertainty despite corporate integrity agreements now nearing closure[S6].

- Environmental laws increasingly mandate robust processes especially around sterilization chemicals used posing litigation risks if incidents occur[S14],[S25]. These factors collectively amplify operating complexity requiring significant resource allocation.

Supply Chain Dependency & Operational Considerations

A notable concentration exists where top three suppliers collectively contributed roughly 40% of purchase volume—this aggregation poses vulnerability especially if disruptions akin to past product recalls recur forcing last-minute sourcing alternatives potentially at higher cost[S11].

Operationally reliance on continuous IT systems functioning remains critical given their role in order processing and billing; cyberattack events could materially disrupt operations given digital platform centrality[S11],.

Conclusion

Accendra Health has embarked on a pronounced business transition post-P&HS divestiture focusing on patient direct services leveraging technology-driven efficiencies. While this represents a strategic adaptation aligned with broader healthcare trends favoring outpatient home-based care, near-term financial health is challenged by large payor contract loss exposures, substantial goodwill impairments weighted on net income/ROE metrics, and pressured liquidity ratios.

Going forward, the capability to replace lost revenue streams through new contracting wins alongside disciplined cost management will dictate whether positive operating momentum converts into sustainable profit recovery and improved cash flow generation essential for long-term value creation.

Monitoring regulatory compliance pathways amidst evolving reimbursement frameworks also remains essential given potentially high penalty costs from violations affecting financial performance.

Disclaimer: This report is for informational purposes only without investment advice or recommendations regarding Accendra Health Inc./VA/. All factual information has been drawn exclusively from cited SEC filings and publicly available news sources as of February 20, 2026.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments