Orchid Island Capital's Rebound Fueled by Strategic RMBS Portfolio Management

A sharp turnaround in net income underscores Orchid Island's focused Agency RMBS investment approach and disciplined capital management in 2025.

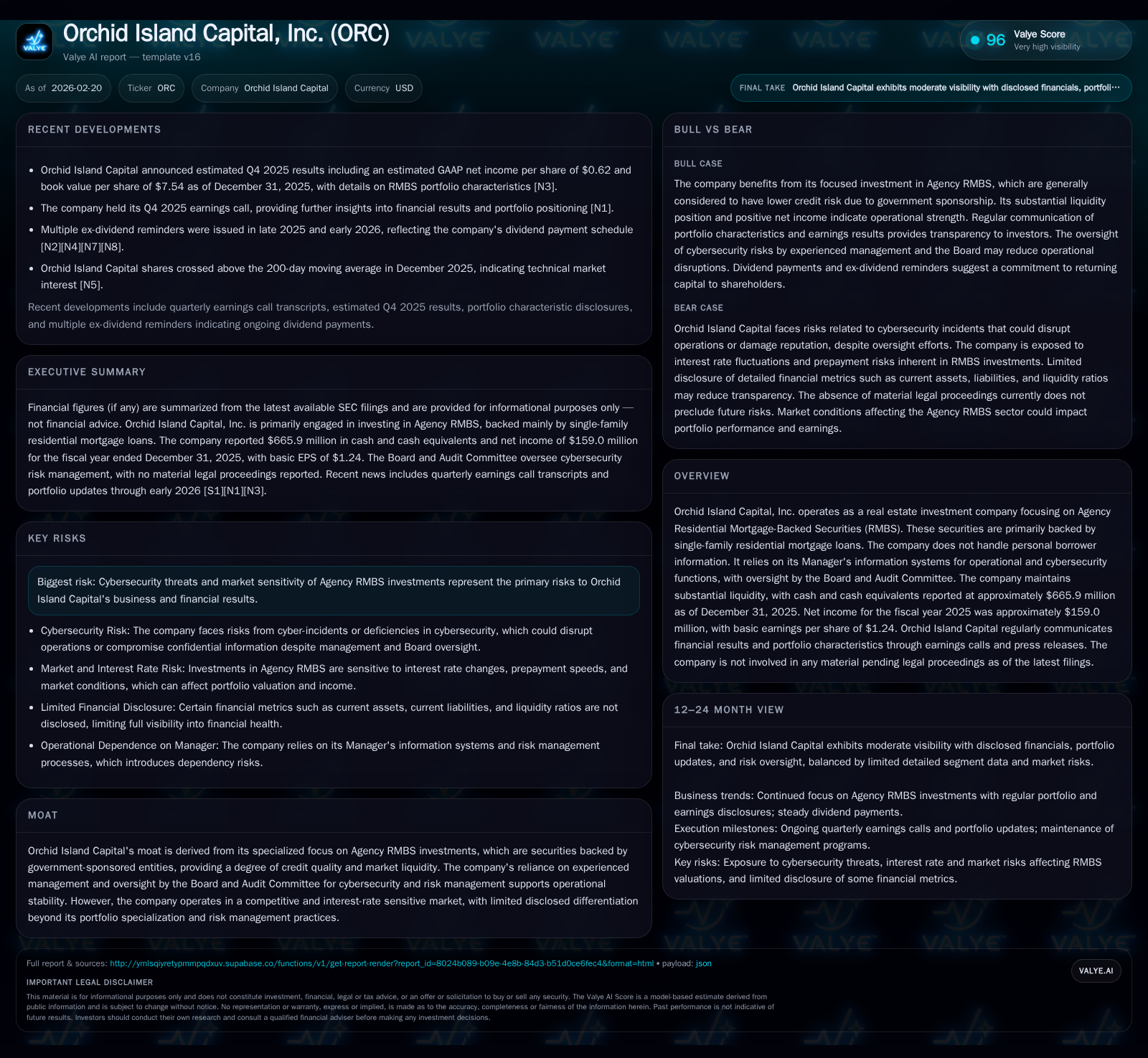

Orchid Island Capital, Inc. delivered a notable financial resurgence in 2025, recording a net income of $159 million after several years of losses, driven primarily by its concentrated investment strategy in Agency Residential Mortgage-Backed Securities (RMBS). The company strengthened its balance sheet with equity doubling year-over-year and improved operating cash flows by nearly 80%. Robust liquidity of $665.9 million as of year-end, alongside consistent dividend payments and measured share repurchases, illustrate strong capital discipline. Orchid Island’s specialized focus on government-sponsored entities' RMBS provides both credit quality and liquidity advantages but maintains sensitivity to interest rate fluctuations and cybersecurity risks.

Financial Resurgence: Historical Performance Overview

Orchid Island Capital executed an impressive turnaround in fiscal year 2025 after enduring steep losses in the preceding three years. The company recorded a net income of approximately $159 million for 2025—a powerful recovery compared to a net loss of $39.2 million in 2023 and an even larger loss of $258.4 million in 2022 [F1]. This represents over a 322% year-over-year increase from 2024’s modest positive net income of $37.7 million.

Operating cash flow also demonstrated significant improvement, surging roughly 80% from $67 million in 2024 to $120.4 million in 2025 [F1]. Such cash flow growth supports not only operational sustainability but also enhances Orchid Island’s ability to deploy capital tactically.

The firm’s equity base expanded substantially from $668.5 million at the end of 2024 to about $1.37 billion at December 31, 2025—more than doubling within one year [F1]. This restoration of book value aligns with the strong earnings trajectory.

Despite prior challenges, Orchid Island maintained steady shareholder distributions throughout this period. Dividends paid increased sharply to nearly $179 million in 2025 compared to $92.5 million in the prior year; meanwhile, share repurchases remained conservative at $7.4 million during the year versus higher amounts earlier in the recovery phase [F1]. The return on equity for 2025 is approximately 11.6%, calculated using reported net income over stockholders’ equity [F1], indicating solid profitability for a mortgage REIT niche play.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | Net YoY |

|---|---|---|---|

| 2025 | 159 | 120 | +322.3% |

| 2024 | 38 | 67 | +196.0% |

| 2023 | -39 | 8 | +84.8% |

| 2022 | -258 | 289 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Rev, OpInc, Capex, FCF. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | ROE% |

|---|---|---|---|

| 2025 | 179 | 7 | 11.6 |

| 2024 | 93 | 3 | 5.6 |

| 2023 | 81 | 10 | -8.3 |

| 2022 | 93 | 25 | -58.9 |

Source: SEC companyfacts cache [F1].

Note: Revenue, Operating Income, Capex, and detailed segment breakdowns are not available from provided tags.

Agency RMBS Investment Strategy and Market Position

At its core, Orchid Island Capital specializes exclusively in Agency Residential Mortgage-Backed Securities (RMBS), which consist mainly of single-family mortgage loans guaranteed or issued by U.S government-sponsored entities such as Fannie Mae or Freddie Mac [S1][N2]. This specialization imbues the portfolio with substantial credit quality due to federal backing while enhancing market liquidity relative to non-agency or private-label securitized products.

This concentrated niche constitutes a defensible moat centered around predictable cash flows tied to government-related credit support structures and liquidity dynamics prevailing for Agency instruments [N2]. However, such focus concurrently exposes Orchid Island to interest rate sensitivity common within fixed-income securitizations—the principal challenge lies in managing duration risk amid fluctuating macroeconomic environments.

Experienced management teams are actively engaged in tactical portfolio adjustments informed by hedging strategies and rate outlooks shared during recent earnings calls [N1] reinforcing their operational expertise aligned with prudent risk governance frameworks overseen by the Board.

Liquidity and Capital Structure Analysis

As of December 31, 2025, Orchid Island reported cash and cash equivalents totaling approximately $665.9 million—a robust liquidity buffer enabling operational flexibility amid unpredictable Agency RMBS market movements [F1].

The firm employs conservative leverage consistent with sector norms for RMBS-focused entities, avoiding excessive debt loads that could amplify volatility or impair balance sheet resilience during interest rate shifts [S10][S13]. This prudent capital structure supports both routine operations and strategic maneuvering opportunities such as potential opportunistic reinvestments or navigating transient dislocations within mortgage-backed securities markets.

Reported disclosures indicate no material debt covenant concerns or impending refinancing risks ahead; liquidity remains well-positioned for anticipated funding needs through at least near-to-medium term horizons based on periodic SEC filings and supplemental investor communications [S14][S19].

Capital Allocation: Dividends, Buybacks, and Shareholder Returns

Orchid Island demonstrates disciplined capital deployment emphasizing shareholder returns balanced against maintaining ample capital for growth potential.

Dividends distributed reached approximately $178.9 million in FY2025—nearly double the preceding year—highlighting management’s commitment to returning excess earnings amidst profitability restoration [F1][S8][S18]. Monthly dividend declarations around $0.12 per share have been consistently announced since late-2025 into early-2026 per public filings [N3][S28].

Conversely, share repurchase activity has been restrained compared to dividends; repurchases amounted to just $7.38 million last year versus historical peaks exceeding $24 million in earlier years [F1], possibly reflecting conservative re-entry given market valuations or regulatory considerations attached to stock buybacks within mortgage REIT structures.

Overall payout ratios remain reasonable considering improved earnings visibility while signaling prudent preservation of equity cushion amid prevailing interest-rate sensitivity endemic to the Agency RMBS space [S21].

Cybersecurity Governance and Operational Risk Management

Operational risk oversight incorporates cybersecurity as a key element given the firm’s dependence on robust information systems without direct handling of borrower personal data—consistent with its investment-only business model focused on Agency RMBS securities portfolios [S1][S6].

The full Board alongside its Audit Committee regularly oversees cybersecurity risk management programs conducted by the company’s Manager plus third-party security audits ensuring continuous threat monitoring and incident response capabilities.

Senior executives Robert Cauley (CEO) and colleague Haas jointly lead cybersecurity risk initiatives backed by over two decades’ experience managing similar risks across related entities [S1][S20]. The absence of any material pending legal proceedings related to cyber incidents further reflects effective governance protocols currently enforced within daily operational frameworks.

Outlook: Growth Prospects and Key Market Constraints

Looking ahead, Orchid Island's growth largely pivots on favorable executions within the Agency RMBS market characterized by government backing providing baseline stability alongside attractive yield curves when properly hedged [N1][N2]. Opportunities exist via tactical repositioning amidst shifting interest rates or prepayment speed variances impacting portfolio returns.

Still, vulnerabilities persist from inherent interest rate risk affecting fair value marks of fixed income holdings plus evolving cybersecurity threat landscapes which may disrupt operations if not diligently managed according to disclosed Board-level oversight procedures [S4][S20]. The lack of direct forward guidance mandates close market surveillance especially concerning Federal Reserve policy decisions influencing mortgage rates.

Investors should keenly observe fluctuations in prepayment speeds, funding costs tied to balance sheet leverage strategies underpinned by Agency paper liquidity conditions along with quarterly performance updates issued by management during earnings calls for clearer directional signals going forward.

Milestones to Watch: Earnings Drivers and Risk Factors

Critical near-term markers include scheduled quarterly earnings presentations where management typically reports updated net income figures inclusive of realized/unrealized gains on RMBS portfolios along with book value metrics reaffirmed or revised as warranted by market conditions shown recently for Q4-2025 results disclosed end-January [N1][N2].

Corresponding dividend declarations remain pivotal events; recent monthly payouts (~$0.12/share) set expectations around steady income streams for shareholders while signaling confidence from strong operating results reported so far into FY25-Q4.

Regulatory shifts affecting GSE frameworks or mortgage-backed securities accounting treatments could alter investment landscapes requiring investors be alert for any regulatory updates hinted in SEC filings or Company press releases relevant for material impact assessments on ORC’s core agency exposure profiles.

In summary: continuous monitoring of interest rates environment impacts on portfolio valuation dynamics coupled with cyber incident vigilance enforced via Board audit mechanisms constitutes key focal points shaping ORC's medium-term investment narrative.

This analysis is based solely on information publicly disclosed through company filings (Form 10-Ks/10-Qs), archived press releases, earnings call transcripts, and recent news sources as cited herein through February 20, 2026, without projection beyond offered statements or intrinsic data points. Readers should consider this as an informational review rather than investment advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments