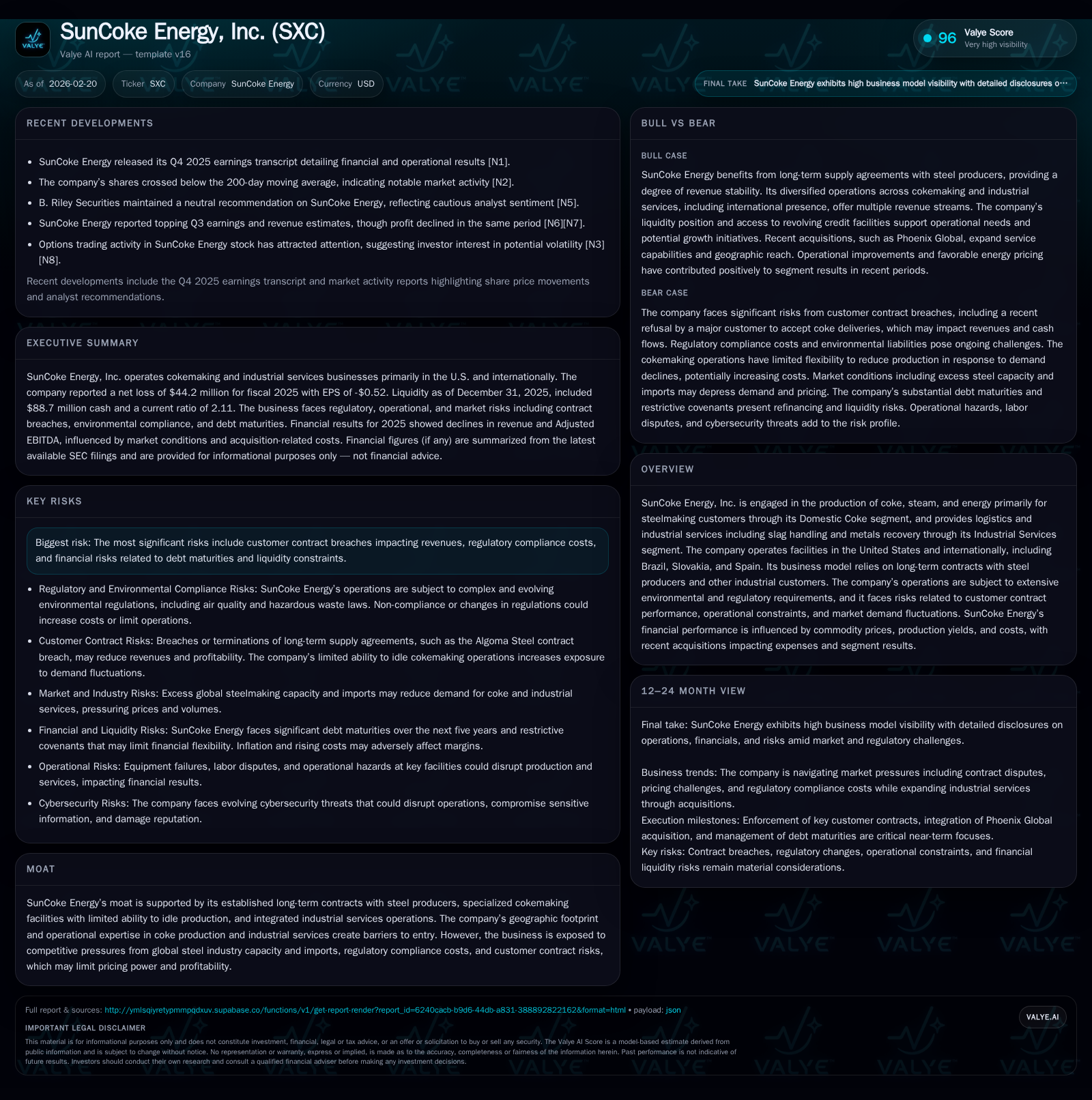

SunCoke Energy’s Contract Reliance and Environmental Costs Weigh on 2025 Profitability

SunCoke Energy’s financial results for 2025 reflect operational challenges, regulatory pressures, and risks tied to long-term customer contracts.

SunCoke Energy, Inc. experienced a pronounced decline in earnings in 2025 driven by contract disruptions, higher operating expenses, and tightening environmental regulations impacting its cokemaking and industrial services segments. Despite stable revenues supported by long-term contracts and geographic diversification including international operations, rising costs and operational constraints contributed to an operating loss and net income decline. The company’s robust cash flow generation has softened the impact somewhat, but significant debt maturities and regulatory compliance headwinds pose ongoing risks to financial flexibility. Looking ahead, growth hinges on contract renewals, operational efficiency gains, and managing increasing environmental compliance requirements.

Company Overview and Business Model

SunCoke Energy, Inc. operates primarily in the cokemaking sector supplying coke, steam, and energy critical for steelmaking customers through its Domestic Coke segment. Complementing this is its Industrial Services segment that focuses on logistics including slag handling and metals recovery. The firm maintains facilities not only in the United States but also internationally—Brazil, Slovakia, and Spain—which extends its footprint and exposes it to varying regulatory landscapes [S1][S16][S17]. Its business hinges heavily on long-term agreements with steel producers who rely on coke as an essential raw material.

The company's moat is derived from these longstanding contracts combined with highly specialized cokemaking facilities that cannot be idled without substantial cost or technical difficulty. Its integrated service offerings create additional barriers for competitors but also expose SunCoke to demand fluctuations in global steel markets as well as stringent environmental oversight .

Historical Financial Performance (2016–2025)

From 2016 through 2019, SunCoke’s revenues grew steadily reflecting solid demand for metallurgical coke aligned with steel industry trends:[F1]

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -44 | 109 | -44 | 67 | -146.1% |

| 2024 | 96 | 169 | 152 | 73 | +66.8% |

| 2023 | 58 | 249 | 125 | 109 | -42.9% |

| 2022 | 101 | 209 | 154 | 76 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Rev, Buybacks. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 41 | 42 | -7.4 |

| 2024 | 38 | 96 | 14.1 |

| 2023 | 31 | 140 | 9.4 |

| 2022 | 24 | 133 | 17.2 |

Source: SEC companyfacts cache [F1].

Data limitations prevent a complete view prior to recent years; however:[F1]

- Revenues reached approximately $1.6 billion by end-2019.

- From 2022 onward detailed profitability data is available showing volatile but positive operating income ($125M–$153M range through 2024) until a sharp fall in 2025.

For the most recent period ending December 31, 2025:[F1]

- Revenue data for the full year beyond FY2019 is unavailable; the latest fiscal snapshot shows revenue around $1.6 billion at latest complete point.

- Operating Income swung from +$152 million in FY2024 to a negative $44 million loss in FY2025 — a year-over-year decline exceeding 129%.

- Similarly, Net Income collapsed from a profit of $96 million in FY2024 to a loss of $44 million in FY2025 (-146%).

- Operating Cash Flow declined roughly 35% YoY to $109 million in FY2025.

- Capital expenditures were trimmed moderately by over 8% to approximately $67 million reflecting prudence amid profitability pressures.

- Dividends paid increased slightly to $41 million.

The deterioration in profitability aligns with reported operational challenges including contract disputes and higher costs [N1][S2][S3].

Drivers Behind Recent Performance

Several key factors contributed materially to the compression of earnings during the recent period:

Contractual Disruptions

Algoma Steel's refusal late in Q3-Q4 of 2025 to accept additional coke deliveries under a binding supply contract has introduced financial losses linked to unutilized capacity and billing disputes [S2]. This not only reduces revenue visibility but raises legal uncertainties given ongoing enforcement efforts.

Pricing / Volume Mix Pressure

Lower commodity prices for coal inputs have transmitted through long-term take-or-pay agreements resulting in lower pricing realized on certain blast furnace coke sales within Domestic Coke operations [S2]. Additionally, unfavorable coal-to-coke yields have constrained volume throughput impacting total sales quantities.

Acquisition Integration Costs

SunCoke incurred significant transaction-related expenses associated with acquiring Phoenix Global during this period adding upward pressure on SG&A lines [S2][S3][S26].

Regulation & Environmental Compliance Costs

Implementation of new EPA Maximum Achievable Control Technology (MACT) standards finalized in 2024 represents substantive capital investment demands along with increased operational constraints [S21][S22]. Regulatory compliance complexities are compounded by potential permit renewal difficulties which can impact production continuity.

Inflation & Cost Structure Effects

Rising inflation has increased labor costs (notably under unionized labor agreements), raw material costs including metallurgical coal sourcing expenses, and maintenance CAPEX burdens – limiting margin expansion possibilities [S4][S19].

Operational Limitations & Asset Utilization Constraints

Technological design prevents straightforward idling of cokemaking plants without risking asset integrity causing potential carry costs during periods of unsold coke inventory buildup [S16]. Furthermore, occasional equipment failures or natural disasters can significantly disrupt output.

Segment & Geographic Exposure Considerations

SunCoke’s Dual Segments:

- Domestic Coke: Core cokemaking operations predominantly supply integrated steel producers under trackable contracts but vulnerable to industry cyclical swings.

- Industrial Services: Logistics-oriented including slag handling/metals recovery which depends on securing additional coal volumes beyond current customers for growth [S17].

International operations introduce sovereign risk dimensions including political instability and currency volatility; compliance with laws such as anti-bribery regimes adds layers of complexity [S25][S20]. Regional risks such as Gulf Coast exposure heighten vulnerability to climatic disasters impacting CMT facilities [S17].

Liquidity & Capital Structure Dynamics

At period-end FY2025:[F1] SunCoke held around $88.7 million cash plus over $126 million borrowing availability under revolving credit lines enabling working capital flexibility. However:[F1] total consolidated debt maturities over next five years sum to approximately $693 million presenting notable refinancing risk amid potentially tighter credit markets.[S4][S11] Restrictions embedded within existing credit agreements limit incremental borrowing freedom complicating future capital raising or acquisitions[S5][S6]. Inflationary cost pressure elevates borrowing costs further[S4]. Operational free cash flow generated (approx. $42M after capex) provides some room for deleveraging but margins must improve markedly[S1][F1]. No share repurchases occurred recently while dividends have steadily increased suggesting commitment to shareholder returns albeit at risk if cash flow pressures deepen.[F1]

Regulatory Environment & Litigation Risks

SunCoke faces multi-faceted exposures:

- Environmental regulations impose extensive permitting requirements with potential for non-renewal or operational restrictions adversely impacting production capacity[S21][S22][S23].

- Compliance expenses related to air quality controls have escalated post EPA MACT standards introduction[S21].

- Litigation risks stem from environmental claims, personal injury suits linked to hazardous exposures at plant sites as well as ongoing commercial disputes including Algoma contract enforcement lawsuits[S9][S12].[S24]

- Cybersecurity threats continue evolving posing risks for data breaches incurring remediation costs; company maintains protocols yet uncertainty remains[S10][S14].

- Labor union negotiations remain critical; failure or delays could provoke work stoppages adversely affecting outputs[S19]. Overall these factors increase cost baselines while injecting earnings volatility.

Outlook & Growth Opportunities

Based strictly on disclosed facts:

- Potential growth drivers include expansion of industrial services volumes especially targeting dry bulk commodities[S17]; successful contract renegotiations or new customer wins would underpin volume growth.

- Continued geographic diversification may partially mitigate localized downturns though political/operational risks persist.

- Advances in operating efficiencies leveraging technology investments could reduce unit operating costs but require upfront capex which could be constrained given debt profile.

- Environmental compliance strategies could become either burdensome cost centers or positions for competitive differentiation depending upon execution. Absent explicit guidance published recently[N1], key metrics watchers should track:

- Contract resolution outcomes particularly Algoma litigation progress;

- Quarterly operating margin trends indicating stabilization or further erosion;

- Capital expenditure pacing relative to regulatory mandates;

- Refinancing outcomes addressing large upcoming debt maturities;

- Regulatory developments stemming from EPA MACT litigations;

- Labor negotiations updates impacting staffing stability. Overall growth appears conditioned on balancing headwinds against strategic operational adjustments.

Returns & Capital Allocation Analysis

SunCoke's returned capital profile reflects:[F1]

- Negative ROE estimated approx -7.4% for FY2025 owing primarily to net losses despite sizeable equity base ($597 million).

- Conservative capital expenditure approach evident amid tightening margins though capex remains material ($67 million).

- Operating cash flow generation remains positive supporting dividend payments which rose modestly suggesting management prioritizes consistent payout amidst profitability declines.[F1] No recent buyback programs reduced share count significantly post pandemic era[F1]; company appears focused on preserving liquidity given deleveraging concerns.[S7] Financial leverage remains elevated with refinancings necessary over coming years moderated by restrictive covenants limiting strategic flexibility.[S11]

Summary Perspective

SunCoke Energy confronts fundamental tradeoffs shaped by: contractual dependencies vulnerable to customer performance risk; intense regulatory scrutiny inflating costs; high fixed-cost cokemaking assets limiting operational agility; geopolitical complexity across international sites; inflationary pressures squeezing margins; and considerable near-term debt refinancing obligations constraining capital options. Yet its entrenched market position supported by long-dated contracts alongside diverse industrial service capabilities offers resilience enabling positive operating cash flows despite earnings volatility. Future success will likely hinge on effective contract enforcement/renewal outcomes—including resolution of Algoma-related disputes—coupled with proactive cost management addressing environmental compliance demands and sustained investment discipline balancing modernization needs against liquidity preservation. Industry conditions such as global steel demand dynamics will additionally influence growth prospects outside company control. Investors monitoring SunCoke must weigh these intertwined factors appreciating that while revenue stability benefits from structural contracts protecting topline variability somewhat, downside risks remain significant particularly on profitability metrics amidst evolving regulatory/market environments.

This analysis is provided solely for informational purposes based on publicly available company disclosures and does not constitute investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments