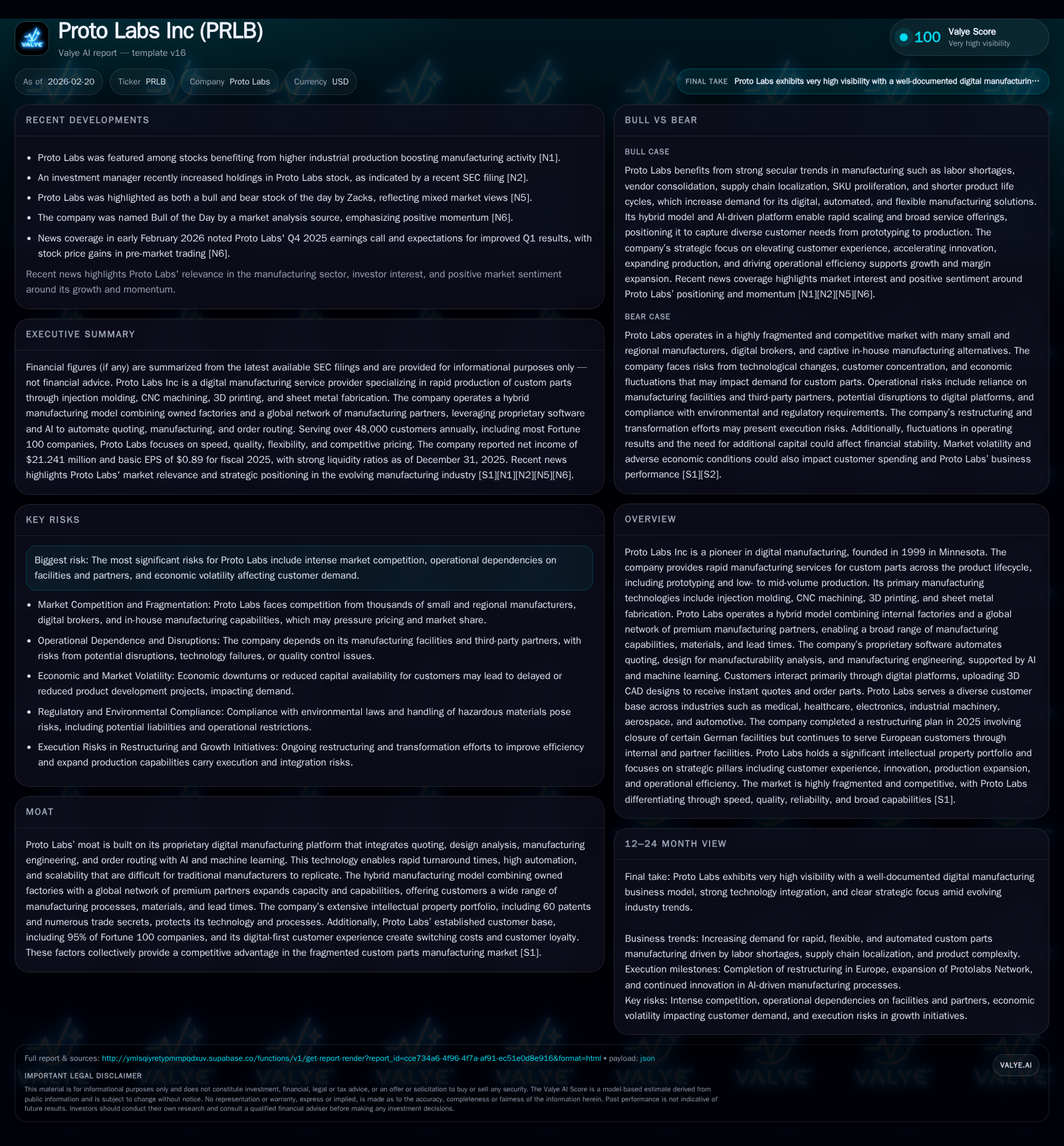

Proto Labs’ Transition to Scalable Digital Manufacturing Powers Profitability

Proto Labs leverages its AI-driven digital manufacturing platform and hybrid production model to drive recent operational improvements and position for growth.

Founded in 1999 as a rapid prototyping innovator, Proto Labs has evolved into a scalable digital manufacturing leader by integrating AI-driven quoting, advanced manufacturing technologies, and a hybrid factory-partner network. After volatile results during 2022, Proto Labs delivered a strong profitability rebound in 2025, supported by increased operating income (+26.1% YoY) and net income (+28% YoY) alongside stable operating cash flows. Future growth drivers include accelerating innovation in AI-powered quoting and order routing, expansion of the Protolabs Network, and operational efficiency initiatives. Capital allocation balances reinvestment in capacity with consistent share repurchases, underpinned by robust liquidity and a ~3.2% ROE. Key risks remain intense competitive pressures from traditional and emerging digital manufacturers and economic sensitivities impacting customer investment cycles.

Evolution of Proto Labs’ Digital Manufacturing Leadership

Proto Labs was established in 1999 with a mission to drastically reduce the turnaround time for injection molding prototypes through sophisticated software automation. Over more than two decades, the company has continuously expanded its portfolio to include CNC machining, 3D printing, and sheet metal fabrication — each service embedded within its proprietary digital thread linking quoting through manufacturing execution. This thread involves complex algorithms that automate design-for-manufacturability (DFM) feedback coupled with instant online pricing accessible via web platforms where customers upload CAD models directly.

The company’s fundamental advantage derives from this deeply integrated technology stack augmented by AI-powered intelligent pricing algorithms and machine learning-enabled order routing systems that intelligently match jobs to either internal factories or premium external partners within minutes [S4][S5][S6]. This integration fosters highly scalable operations that sustain rapid quotations at scale while maintaining quality assurances.

A testament to these advantages is Proto Labs’ adoption by over 300,000 customers worldwide spanning all major industrial sectors including medical devices, aerospace components, computer electronics, industrial equipment, and automotive parts supply chains — notably serving approximately 95% of Fortune 100 companies in these realms [S14]. Such penetration underpins strong switching costs owing to workflow entrenchment into customers' product development lifecycles.

Revenue Growth Trajectory and Operational Performance Trends

The company's financial trajectory shows notable volatility around FY2022 but a marked recovery through FY2025. Key financial metrics summarized below illustrate the performance shifts:

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 21 | 75 | 25 | 15 | +28.0% |

| 2024 | 17 | 78 | 20 | 9 | -3.6% |

| 2023 | 17 | 73 | 28 | 28 | +116.6% |

| 2022 | -103 | 62 | -98 | 22 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Rev, Div. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 43 | 60 | 3.2 |

| 2024 | 60 | 69 | 2.5 |

| 2023 | 44 | 45 | 2.5 |

| 2022 | 30 | 40 | -14.8 |

Source: SEC companyfacts cache [F1].

Note: Revenue not provided for recent years in available tags.

After suffering an operating loss of nearly $98 million in FY2022 — attributed largely to operational disruptions combined with macroeconomic headwinds — Proto Labs staged a steady recovery marked by positive operating income of $25.11 million in FY2025 ([F1]). The net income rebound followed suit advancing almost 30% year-over-year.

Operating cash flows have displayed resilience throughout these periods remaining robust above $60 million annually with modest contraction (-4.3%) into FY2025 despite a material increase in capital expenditures (+61.9%), signaling management’s commitment to capacity expansion and technology investment [F1].

The company’s current ratio exceeding 3x evidences strong short-term liquidity positioning against current liabilities totaling approximately $67 million by FY-end '25 [F1]. Share repurchase activity has also been substantial with $43 million deployed in FY2025 alone reflecting an active capital return policy even amidst growth re-investment.

Technology Integration: AI and Software Empowering Scalability

Central to Proto Labs' evolution is the deployment of advanced AI techniques embedded across multiple facets of its digital production platform: from automated quoting engines capable of instantaneously analyzing complex CAD geometry through proprietary DFM checks to machine learning-based smart order routing that assigns jobs optimally between internal factories or network partners within minutes [S4][S5][S6].

These algorithms not only accelerate turnaround times but also reduce non-recurring engineering (NRE) costs by automating setup validations previously performed manually—lowering per-part cost structures as volumes scale.

Smart order routing represents a sector-native innovation combining probabilistic models trained on millions of historical part productions; it dynamically evaluates partner capacity constraints against technical requirements enabling flexible lead time options without sacrificing quality or cost competitiveness.

Such integration facilitates simultaneous handling of thousands of unique part designs — a critical scale factor enabling the firm’s leadership in prototype-to-production workflows where speed is paramount amidst increasingly shorter product life cycles across customers' industries.

Expanding Production Capabilities: Factory and Partner Network Synergies

The augmentation of internal facilities with a global network of premium manufacturing partners under the Protolabs Network brand is key to broadening Proto Labs’ addressable market segments beyond its factory’s physical capacity limits [S7]. This hybrid model enables the firm to support larger size parts, more complex geometries, broader materials selections (including advanced resins or metal alloys), varying lead times from ultra-fast turnarounds to economical paced production runs along with diverse price points catering to different customer needs.

This strategically diversified sourcing approach addresses industry demands for supply chain resiliency amid geopolitical uncertainties while mitigating risks associated with single-site dependency highlighted previously by the company’s consolidation actions such as facility closures in Germany completed Q4 '25 [S7]. It also creates a meaningful moat vis-à-vis competitors confined strictly to captive manufacturing or purely brokerage roles lacking integrated proprietary software capabilities.

Competitive Positioning and Market Risks in Custom Parts Manufacturing

Proto Labs operates within a highly fragmented yet competitive landscape populated by thousands of small-to-mid-size regional suppliers alongside digital brokers and captive internal manufacturing groups among its customers [S8][S15]. Emerging competitors attempt replicating facets of PRLB’s technology-driven model leveraging additive manufacturing advancements or developing their own automated quoting interfaces.

Key competitive virtues here include speed-to-quote/part delivery reliability; precision quality controls meeting tight dimensional tolerances; an exceptional user interface coupled with seamless ordering experiences; scale enabling concurrent parallel process runs without compromising economics; flexible capacity management; strict adherence to price points aligned with total cost-of-ownership considerations; plus robustness across geographic markets given regulatory compliance hurdles.

Patent protection across methods spanning subtractive/additive manufacturing techniques plus pricing models covered by ~60 granted patents provide defensive barriers though continuous innovation remains essential given potential IP circumvention risks outlined by management [S10][S13].

Industrial cyclicality poses demand sensitivity risks as delays or cancellations of prototype projects affect throughput leading-edge sectors most reliant on custom parts like medical devices or aerospace face funding shortages could pause spending [S18].

Future Growth Catalysts and Market Constraints

Management articulates four overarching strategy pillars for future build-out approved alongside recent earnings: elevating customer experience through end-to-end friction elimination; accelerating innovation pace introducing new capabilities faster; methodically expanding production offerings led by strategic customer feedback; plus driving operational efficiency capturing fixed cost leverage as volume scales [N2][S6].

AI-enhanced quoting improvements promise further NRE automation gains important for enticing broader mid-volume production applications beyond initial rapid prototyping roots [N11]. The iterative upgrading of analytic tools fostering better price accuracy without sacrificing margin will be critical as competitive pressures escalate.

Growth drivers also include expansion of Protolabs Network offering access to partners across North America, Europe, Asia broadening geographic reach while addressing SKU proliferation trends requiring nimble supply flexibility alongside increasing customization demand across end-markets like consumer electronics or automotive electrification platforms [N8][S19].

Conversely inflationary pressures raising raw material costs plus potential recessions could cap demand especially among smaller startups lacking deep capital reserves impacting order frequency or mix-weighted margins [N3][S16].[N4]

Capital Allocation, Cash Flow Generation, and Shareholder Returns

Proto Labs demonstrates conservative balance sheet stewardship optimizing between growth investments and shareholder returns: FY2025 capex spiked ~62% YoY to ~$14.8 million indicating strategic commitments towards factory modernization or software upgrades in line with targeted production expansion objectives [F1].

Operating cash flow remained robust at $74.5 million supporting healthy free cash flow near $59.7 million after capex—a solid cushion supporting continued buybacks evidenced by $43 million redeemed stock shares expanding prior-year repurchase cadence albeit no dividend program disclosed thus far [F1].

Equity stands formidable at approximately $674 million yielding an approximate reported ROE near ~3.2%, modest but reflective perhaps of reinvestment priority over short-term profitability maximization typical for tech-driven growth cycle companies diversifying manufacturing capabilities globally [F1].

This measured capital allocation framework provides flexibility for opportunistic acquisitions complementing organic growth while soothing market confidence given tangible cash return policies notwithstanding the transitional growth phase.

Key Financial Metrics Track Record — Analysis Table Included

Fiscal data from XBRL tagged points illustrates underlying numeric progressions corresponding closely with strategic shifts emphasized throughout:

| FY | Rev (USD m) | OpInc (USD m) | NetInc (USD m) | CFO (USD m) | Capex (USD m) | Buybacks (USD m) |

|------|-------------|---------------|----------------|-------------|---------------|------------------|

|2025*| N/A |25.11 |21.24 |74.50 |14.84 |42.96 |

|2024*| N/A |19.91 |16.59 |77.83 |9.17 |60.28 |

|2023*| N/A |28.17 |17.22 |73.27 |28.12 |43.95 |

|2022*| N/A |-97.98 |-103 |62.08 |21.69 |- |

*Revenue data not provided in the current disclosures.

Omitted Metrics: Revenue figures insufficiently detailed for recent full fiscal years; dividends not recorded from XBRL tags so excluded.

This data corroborates how aggressive reinvestment phases coincide with temporary profit compression followed by stabilization reflective of business model maturation per sections above.

What to Watch Next: Industry and Company Milestones

Market attention should track upcoming quarterly earnings releases for beats/misses vis-à-vis management priorities particularly related to margin expansions amid capex ramp-ups cited during Q4 earnings call early Feb '26 which surprised positively bolstering outlooks according to pre-market commentary resulting in significant stock appreciation [N2][N3][N12].

Further developments around technological enhancements deploying newer patents especially around AI-modules applied toward non-recurring engineering cost streamlining could materially influence competitive positioning given IP significance described earlier [S10][S14].[N11]

Expansion pace within Protolabs Network notably onboarding new partners capable of additive methods complementing internal metal printing could unlock revenue tiers addressing larger-size parts or complex geometries constrained before by factory limits [S6][N5].

Industry context includes accelerating adoption trends toward digital manufacturing disrupting legacy supply chains requiring integrated e-commerce-like platforms reducing inventory burdens through just-in-time capacity leveraging SKU proliferation forces driving demand for rapid batch flexibility niche Proto Labs serves well [S19].[N4]

Risks remain regarding intensifying competition from players improving their own automated quoting interfaces or additive printing resin capabilities raised earlier [{}], making ongoing R&D investments crucial domain monitoring items.

In summary, Proto Labs sits at the intersection of technological innovation pivoting toward AI-powered scalability underpinned by deliberate capacity boosts via partner networks complemented by steady financial discipline—future quarters will test sustainability amid normalizing economic conditions.

Disclaimer: This analysis is based solely on publicly available information including SEC filings referenced [S#], recent news sources [N#], and reported financial data sets [F1]. No forward-looking statements are made beyond those explicitly contained within cited sources nor investment advice provided.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments