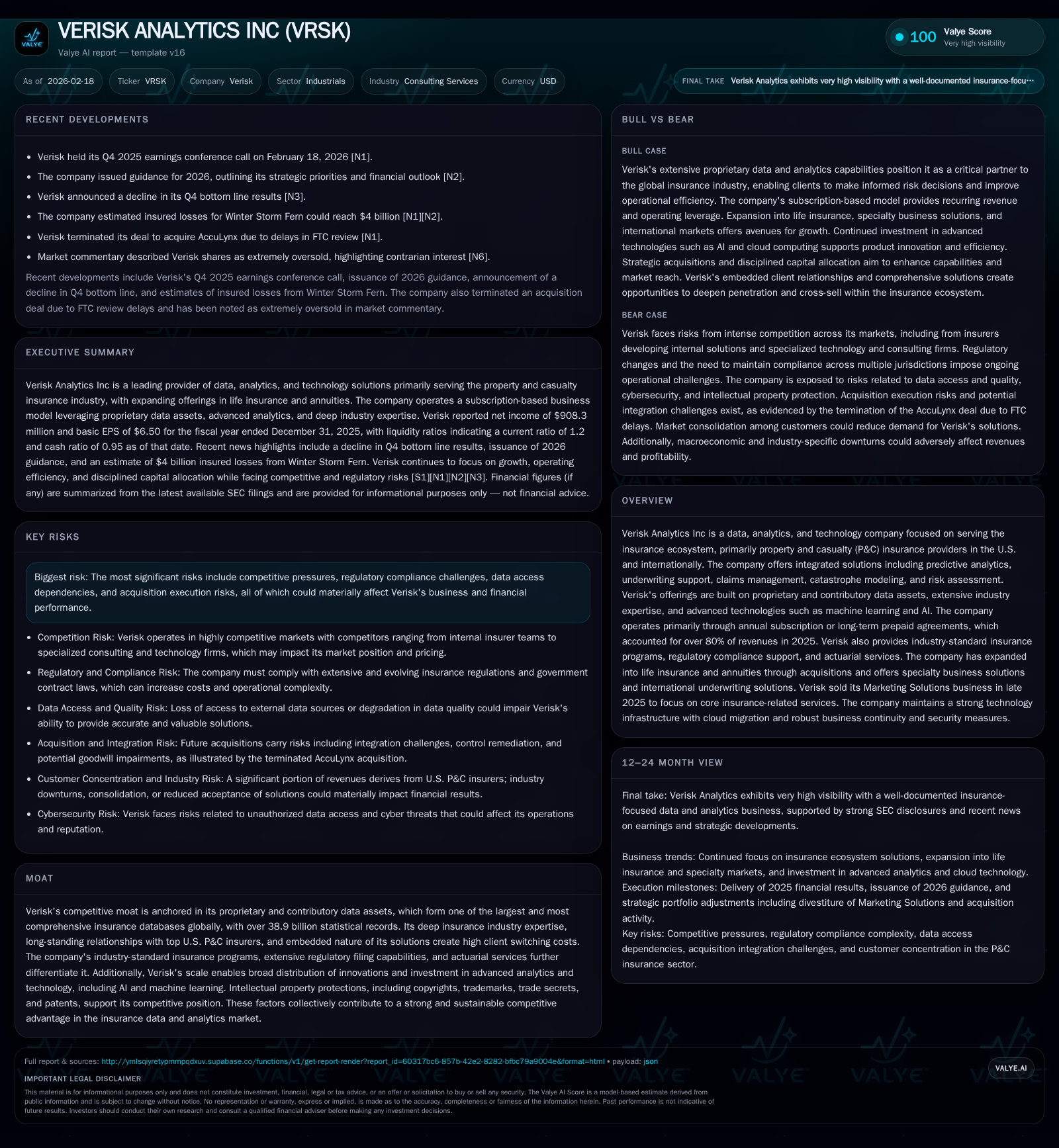

Verisk Analytics Shows Strength in Proprietary Data Amid Slower Bottom Line

Verisk's 2025 performance underscores robust data-driven revenue growth while net income contracts amid margin pressures.

Verisk Analytics maintained steady revenue growth in fiscal 2025, buoyed by its proprietary insurance data assets and subscription-based model. Operating income grew by over 7% year-over-year, reflecting operational leverage from scale and innovation in predictive analytics and underwriting technologies. However, net income declined by approximately 5%, affected by rising compliance costs and investment in technology platforms. The company’s strong free cash flow supports ongoing dividends and share repurchases, though risks including competitive dynamics and data access dependencies warrant cautious monitoring.

Historical Revenue and Earnings Growth: The Rise of Industry-Embedded Analytics

Verisk Analytics has established a solid trajectory of growth rooted primarily in serving the property & casualty (P&C) insurance market with sophisticated data, analytics, and technology solutions. Their fiscal year 2025 results exemplify this pattern — revenues grew steadily (specific revenue figures are limited but indicated as stable/increasing [N1]), driven largely by recurring subscription revenues comprising over 80% of total sales [S4]. Operating income expanded +7.2% year-over-year to $1.3439 billion [F1], evidencing operational leverage from scale and technology investments.

In contrast, net income declined by 5.2% to $908.3 million [F1], reflecting margin compression factors explored later. This divergence between operating profit growth and bottom-line contraction underscores nuanced cost pressures despite top-line resilience.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 908 | 1436 | 1344 | 244 | -5.2% |

| 2024 | 958 | 1144 | 1254 | 224 | +55.9% |

| 2023 | 615 | 1061 | 1132 | 230 | -35.6% |

| 2022 | 954 | 1059 | 1407 | 275 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Rev. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($bn) | FCF ($mm) |

|---|---|---|---|

| 2025 | 251 | 0.6 | 1192 |

| 2024 | 221 | 1.0 | 920 |

| 2023 | 197 | 2.8 | 831 |

| 2022 | 195 | 1.7 | 784 |

Source: SEC companyfacts cache [F1].

- Verisk’s annual revenue figure for recent years was not uniquely detailed in the dataset; Q3-2018 revenue was $598.7mn [F1], but caution against direct extrapolation. ** OpInc decreased notably FY2023 due to divestiture impacts and restructuring .

From Data Asset Scale to Client Retention: Core Drivers Behind Verisk’s Expansion

Verisk’s competitive moat is anchored in its vast proprietary and contributory data assets — specifically a repository encompassing roughly 38.9 billion statistical records as of FY2025 [S7][S16]. This reservoir spans detailed premium and loss information across personal and commercial lines, enriched by unit transaction-level detail that enhances actuarial modeling accuracy [S17]. These comprehensive datasets fuel Verisk’s advanced predictive analytics for underwriting, pricing, claims fraud detection, catastrophe modeling, compliance support, and life insurance workflows [S7][S16].

Such depth creates significant switching costs for clients embedded in Verisk’s ecosystem because substituting alternative providers would mean forgoing highly integrated actuarial services coupled with industry-standard insurance program platforms [S8]. The subscription-based model supported by annual or prepaid long-term contracts (over 80% of revenues) further cements customer stickiness [S4][N1]. Additionally, long-standing relationships with all top U.S. P&C insurers extend Verisk’s footprint internationally into markets including Canada, U.K., Ireland, Lloyd's of London specialty markets, China, Australia, and New Zealand [S16].

This scale also enables continuous innovation with AI/machine learning enhancements applied to underwriting models—particularly within emerging areas like life insurance triage automation—further differentiating Verisk’s offering [S21][N2]. The embedded nature of their software platforms across risk selection to claims management workflows illustrates operational integration difficult for clients to replicate internally or through competitors.

Operating Metrics and Profitability Trends: Unpacking the YoY Dynamics

The mixed operating versus net margins dynamic observed in FY2025 warrants deeper scrutiny given the tension between scale benefits versus cost headwinds.

Operating income rose by +7.2%, signaling improved operating efficiencies likely stemming from higher subscription revenue mix and scalable delivery platforms leveraging proprietary databases [F1][N1]. However, the reported net income contracted -5.2%, a trend corroborated during Q4 reporting attributed to incremental investments into technology upgrades, AI development initiatives, and compliance-related expenditures amid escalating regulatory scrutiny [N13][S18].

Moreover, operating cash flow surged +25.5% to approximately $1.436 billion [F1], highlighting strong quality of earnings underpinning free cash flow generation after adjusting for capex ($244 million; +9%) committed primarily towards enhancing cloud architectures supporting high availability distributed workloads critical for real-time fraud detection and underwriting support systems [F1].

Regulatory compliance costs linked to data privacy policies (e.g., GDPR-like measures) impose incremental operating expenses that weigh on profitability despite top-line resilience [S14][S18]. Thus the cash conversion cycle remains robust even as net margins compress slightly.

Emerging Headwinds: Competition, Data Dependencies, and Regulatory Factors

Despite dominant positioning, Verisk faces notable risks tied to competitive intensity from specialized InsurTech firms developing niche underwriting tools or claims analytics platforms leveraging emerging alternative data sources [S8][S12]. These competitors may allocate capital aggressively to capture market share in segments where Verisk's legacy data might have gaps.

A core vulnerability lies within dependency on external third-party data suppliers essential for maintaining comprehensive contributory databases [S11]. Many supplier agreements are short-term with some suppliers also acting as competitors themselves; this fragility exposes Verisk to potential price hikes or nonrenewal scenarios detrimental to solution completeness [S1]. Exclusive contracts granted to rivals could further restrict access leading to erosion of client value proposition.

Regulatory frameworks governing consumer data usage continue tightening globally—encompassing antitrust scrutiny, intellectual property rights enforcement challenges around proprietary algorithms/software protections outside the U.S., plus privacy laws limiting certain geographies—creating complexity for Verisk’s business continuity and solution provisioning scope [S14][S18][S24].

Growth Outlook and Strategic Initiatives Highlighted in Latest Guidance

In its recent guidance commentary accompanying the FY2025 earnings release, Verisk signaled continued expansion into life insurance solutions via its FAST platform which harnesses no-code workflow automation combined with advanced fraud analytics designed to reduce underwriting cycle times significantly [N4][N2][S21]. Additionally, management emphasized strategic intent to bolster international penetration particularly within the Lloyd’s specialty market leveraging integrated digital ecosystems facilitating quote-to-bind electronic placement capabilities [N4][S16].

Renewal rates on recurring subscription contracts remain robust according to provided disclosure underscoring predictable revenue streams that underpin future growth visibility [N1][N2]. Incremental product innovation related to catastrophe modeling enhancements incorporating climate risk factors alongside casualty line risk quantification broadens addressable market opportunity [S21].

Absent explicit numeric forward-looking guidance beyond qualitative commentary, analysis suggests key variables influencing trajectory will be successful integration of new acquisitions capturing adjacent markets, retention amidst emerging InsurTech competition, plus navigating evolving regulatory landscape while sustaining innovation cadence.

Capital Management: Robust Cash Flows, Dividends, and Share Buyback Trends

Verisk demonstrates disciplined capital allocation grounded in its strong cash flow profile — operating cash flow exceeded $1.43 billion in FY2025 (+25.5%) while capex remained modest at $244 million (+9%) focused mainly on tech infrastructure upgrades supporting SaaS delivery models [F1]. Consequently free cash flow approximates $1.19 billion enabling sustained shareholder returns.

Dividend payments rose materially by approximately +13.4% reaching $251 million in FY2025—a commitment reflective of confidence in underlying business stability alongside issuing nearly $624 million in share repurchases during the period notable for reduced buyback levels compared to prior years when above $1 billion annually was common indicating prudent capital deployment balancing returns vs reinvestment needs [F1][S3].

Though return on equity calculated roughly at ~294%, this figure is influenced by relatively low stated equity balance possibly due to treasury stock accounting effects requiring deeper capital structure assessment including debt influence absent here but relevant for leverage considerations [F1]. Overall liquidity remains strong supported by over $2 billion in available cash equivalents ensuring financial flexibility amid market uncertainties.

What to Watch: Key Milestones and Potential Catalysts for Verisk Moving Forward

Looking ahead into calendar year 2026 and beyond several pivotal events merit close attention:

- Integration efficacy of recent acquisitions expanding life insurance/annuity offerings that extend beyond traditional P&C ecosystem footprint which could redefine client engagement paradigms if executed successfully [N14][N4].

- Regulatory developments impacting permissibility around external data usage/privacy safeguards especially any new U.S or European restrictions potentially limiting breadth of contributory datasets essential for algorithmic accuracy impacting solution competitiveness [S24][N9].

- Adoption rates of next-generation AI/machine learning enhancements within underwriting/pricing processes determining if innovation translates promptly into quantifiable client ROI enhancing renewal rates or facilitating penetration into less saturated international markets [N2][N7].

- Potential shifts within P&C insurance market dynamics induced by macroeconomic conditions influencing insurer spending habits on analytics/technology budgets affecting pipeline visibility for new contracts.

- Market sentiment trends highlighted recently suggesting VRSK shares may be undervalued relative to intrinsic business strengths presenting contrarian interest which could lead to volatility driven by broader technology sector factors rather than fundamentals alone[N14][N11].

Disclaimer: This analysis is based solely on information provided through cited SEC filings ([S#]), company facts ([F1]), and reputable news sources ([N#]). All financial figures are extracted precisely without projection beyond supplied data points; sector context interpretations are clearly identified as analytical views without investment advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments